- The Bank of England kept the Bank Rate at 4.00%.

- The vote split was 5-4 in favour of hold, more dovish than expected.

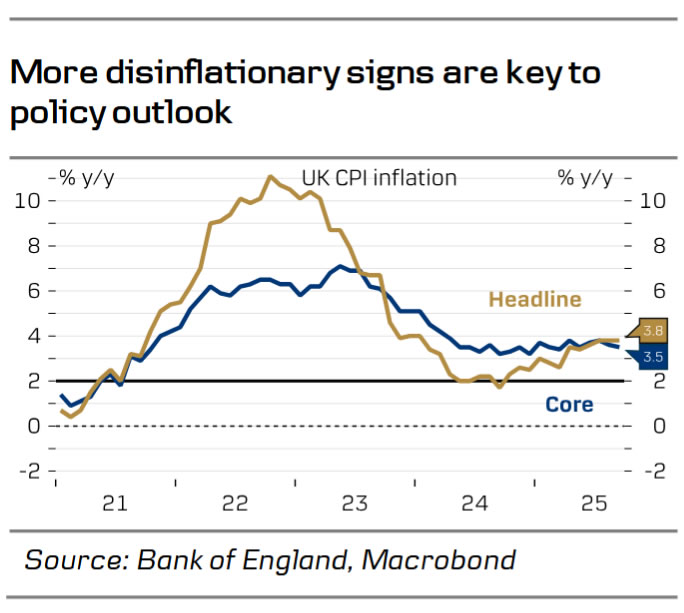

- The potential of further easing hinges a lot on the continuance of the recent promising disinflation.

- The market reacted by trading Gilt yields a bit lower and EUR/GBP higher, although the latter move faded a bit.

The Bank of England (BoE) kept the Bank rate at 4.00% against our expectation but in line with market pricing. The vote split was 5-4 (keep vs. cut), which was more dovish than expected, though. Deputy governors Ramsden and Breeden joined Taylor and Dhingra in the camp voting for cut while Governor Bailey casted his deciding vote for keep with the view: “Rather than cutting Bank Rate now, I would prefer to wait and see if the durability in disinflation is confirmed in upcoming economic developments this year”.

Thus, Bailey looks just one encouraging inflation print away from voting for another cut. Listening in on the press conference, second round effects on inflation were mentioned several times, though, and we do not think Bailey sounds like someone ready to cut at two meetings back-to-back as monetary restrictiveness is reduced further. New projections from the BoE have unemployment slightly higher at 5.0% in 2025/2026 and inflation slightly lower, which does open for more easing. The wording of the BoE’s guidance to investors was shortened significantly but the message is unchanged. “The extent of further reductions will therefore depend on the evolution of the outlook for inflation”.

BoE call. We now expect the BoE to deliver the next cut in the Bank Rate in December, where we also think fresh government spending cuts will call for further easing. We think a majority in the MPC will be ready to cut unless inflation spikes again. We kick the final rate cut further down the road. As monetary restrictiveness falls, we think the bar will increase for the following rate cut. Thus, we expect the April meeting to conclude the easing cycle with the Bank Rate at 3.50%. The Autumn Statement is a big joker in the BoE outlook, though, see also Research UK – Autumn Statement will be key for UK markets.

Market reaction. Gilt yields traded a couple of basis points lower and EUR/GBP higher on the announcement, with the market putting emphasis on the close vote split indicating more easing likely around the corner. We expect EUR/GBP to trend higher the coming year, targeting the cross at 0.89 in 6-12 months.

kept the Bank rate at 4.00% against our expectation but in line with market pricing. The vote split was 5-4 (keep vs. cut), which was more dovish than expected, though. Deputy governors Ramsden and Breeden joined Taylor and Dhingra in the camp voting for cut while Governor Bailey casted his deciding vote for keep with the view: "Rather than cutting Bank Rate now, I would prefer to wait and see if the durability in disinflation is confirmed in upcoming economic developments this year".){kind=link}