Highlights

- The U.S. dollar is coming off a difficult year, but concerns that global investors are fleeing it in droves are overblown.

- The depreciation over the past year still leaves the dollar close to 2024 levels on a trade-weighted basis and in line with its long-term average against many major currencies.

- Looking ahead to 2026, we see additional downside to the greenback of around 3%.

- There is little evidence that the diversification away from dollar-centric systems has accelerated, but it does continue gradually.

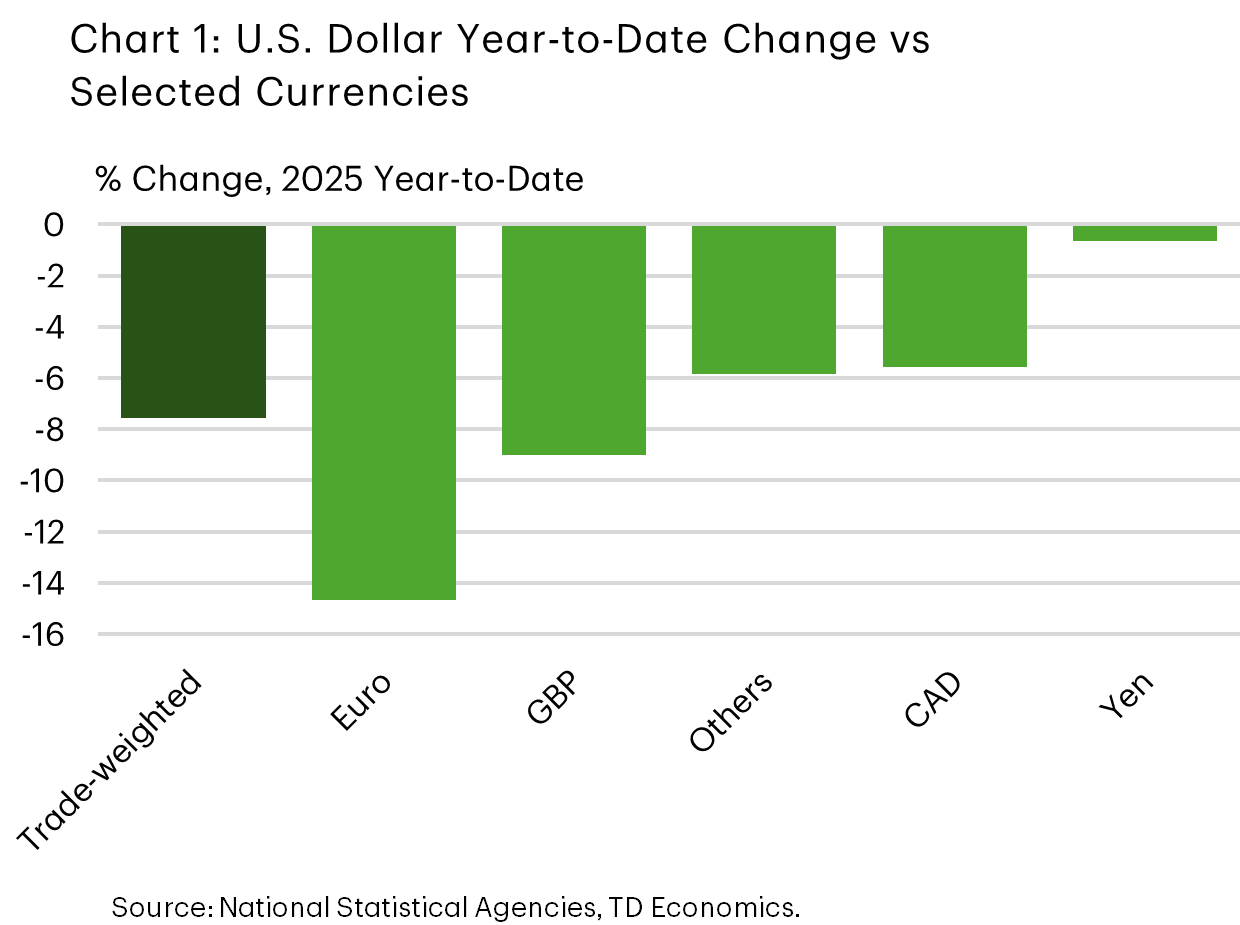

In broad trade‑weighted terms, the U.S. dollar fell roughly 8% in 2025, with a more notable ~10% decline against the majors (Chart 1). This marked an end to a fairly steady run of appreciation since the end of 2023.

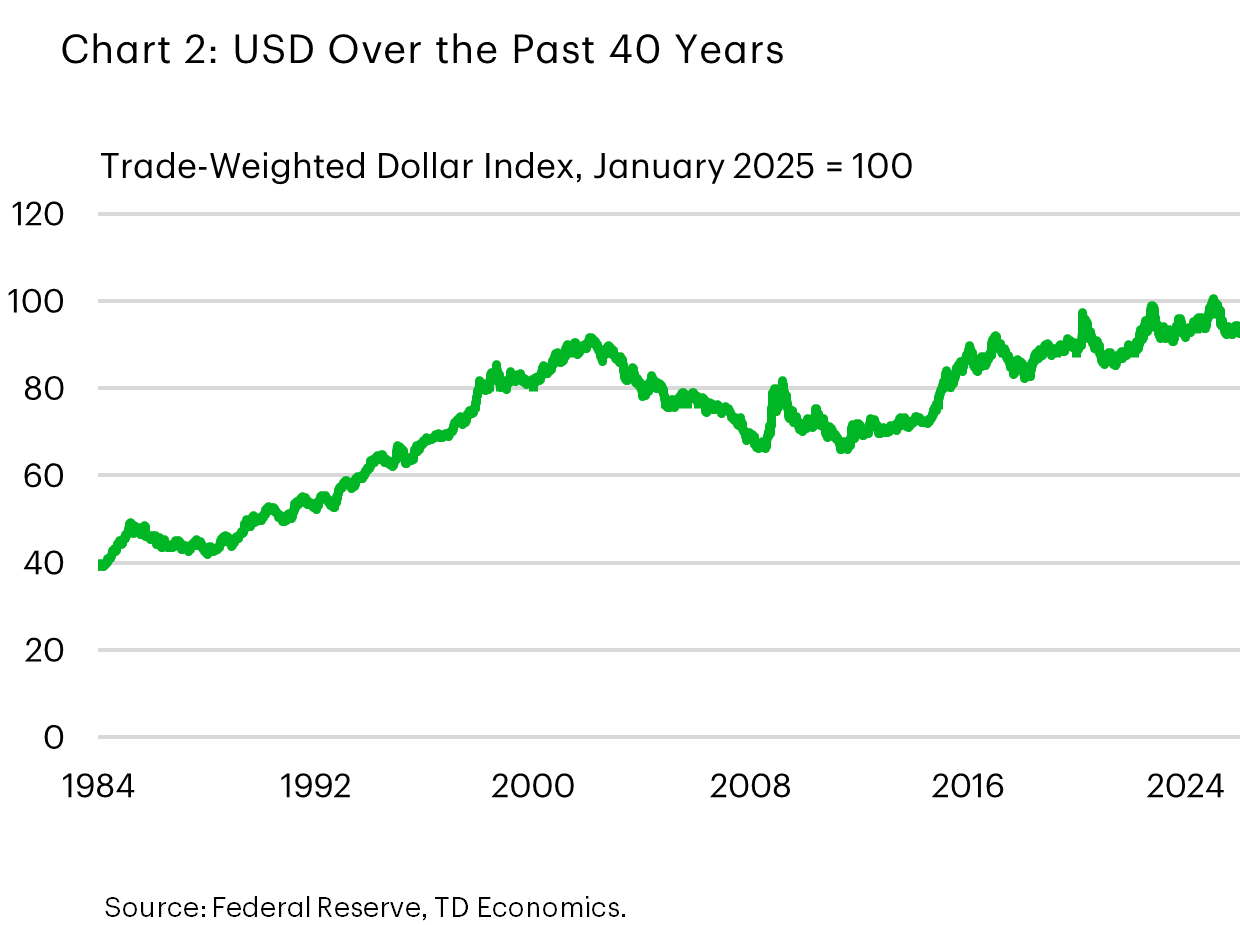

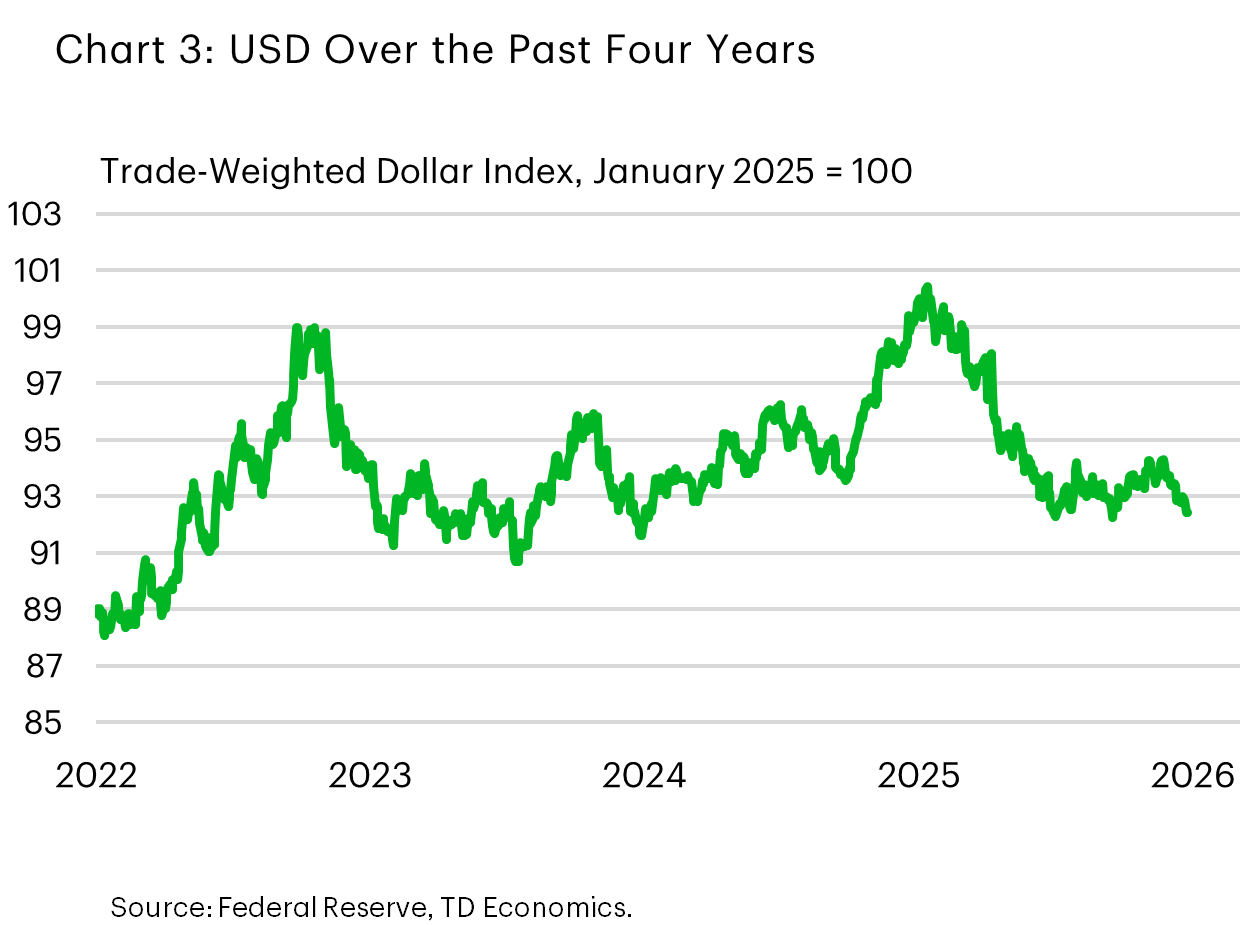

Still, for all the recent chatter around the greenback’s woes the currency is hardly plumbing the depths. Last year’s pull-back only took the USD back to its level prevailing in 2024 and close to its average level over the past decade. Taking an even longer perspective, the trade-weighted dollar continued to hold near its 3-decade high (Chart 2 & 3).

Factors conspiring against the dollar

Part of the perception is fueled by the delta between actual USD performance and the lofty expectations at the start of last year. Many forecasters had anticipated another step up in the dollar in 2025, under the assumption that U.S. import tariffs would be imposed, which in theory should be currency supportive. Moreover, many expected that U.S. growth exceptionalism since the pandemic would carry over into the first half of last year.

It didn’t take long for that thesis to unravel as 2025 got underway. Market attention quickly shifted to the potential negative impact tariffs would have on the U.S. expansion and hopes for Fed rate cuts. Although the rate relief was ultimately delayed until the autumn due to stubborn core inflation, investors never lost hope that U.S. central bank rate cuts would eventually materialize. And, indeed, as the Fed resumed monetary easing in the closing months of 2025, the extra yield offered by dollar-denominated assets relative to global assets narrowed.

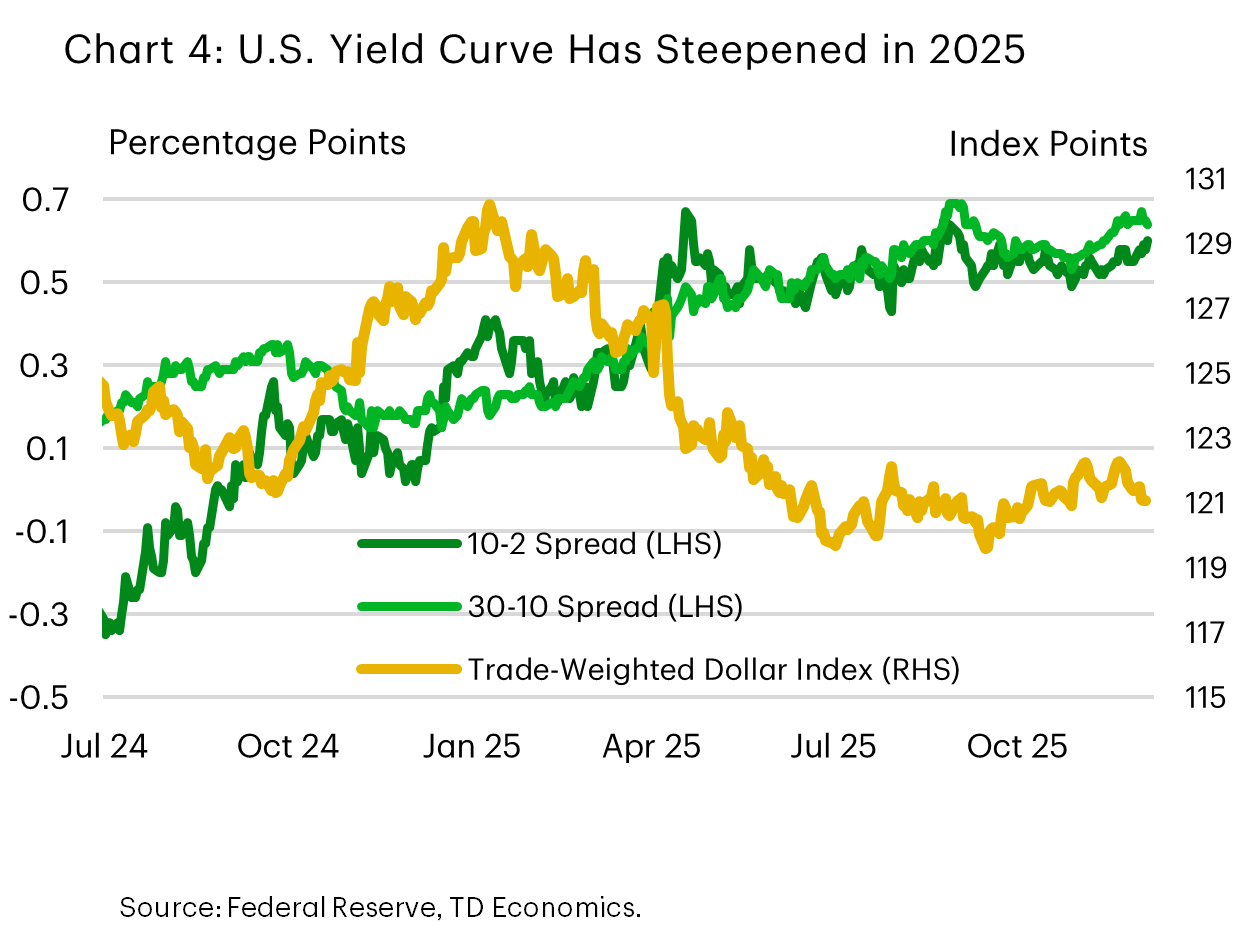

Technical factors also contributed to the bout of dollar weakness. Research from the Bank for International Settlements indicates that a decline in hedging costs between January and May spurred increased foreign currency hedging activity. This effect was particularly pronounced during Asian trading hours, placing incremental downward pressure on the dollar1. We suspect, as well, that the steepening yield curve through May 2025, as the United States Congress debated the One Big Beautiful Bill and its impact on the national debt – alongside discussion around Fed independence – contributed to a souring in sentiment towards the dollar. The depreciation coincided with the increased spreads witnessed on long-term U.S. Treasuries relative to short-term Treasuries (Chart 4).

Euro and pound record the strongest gains

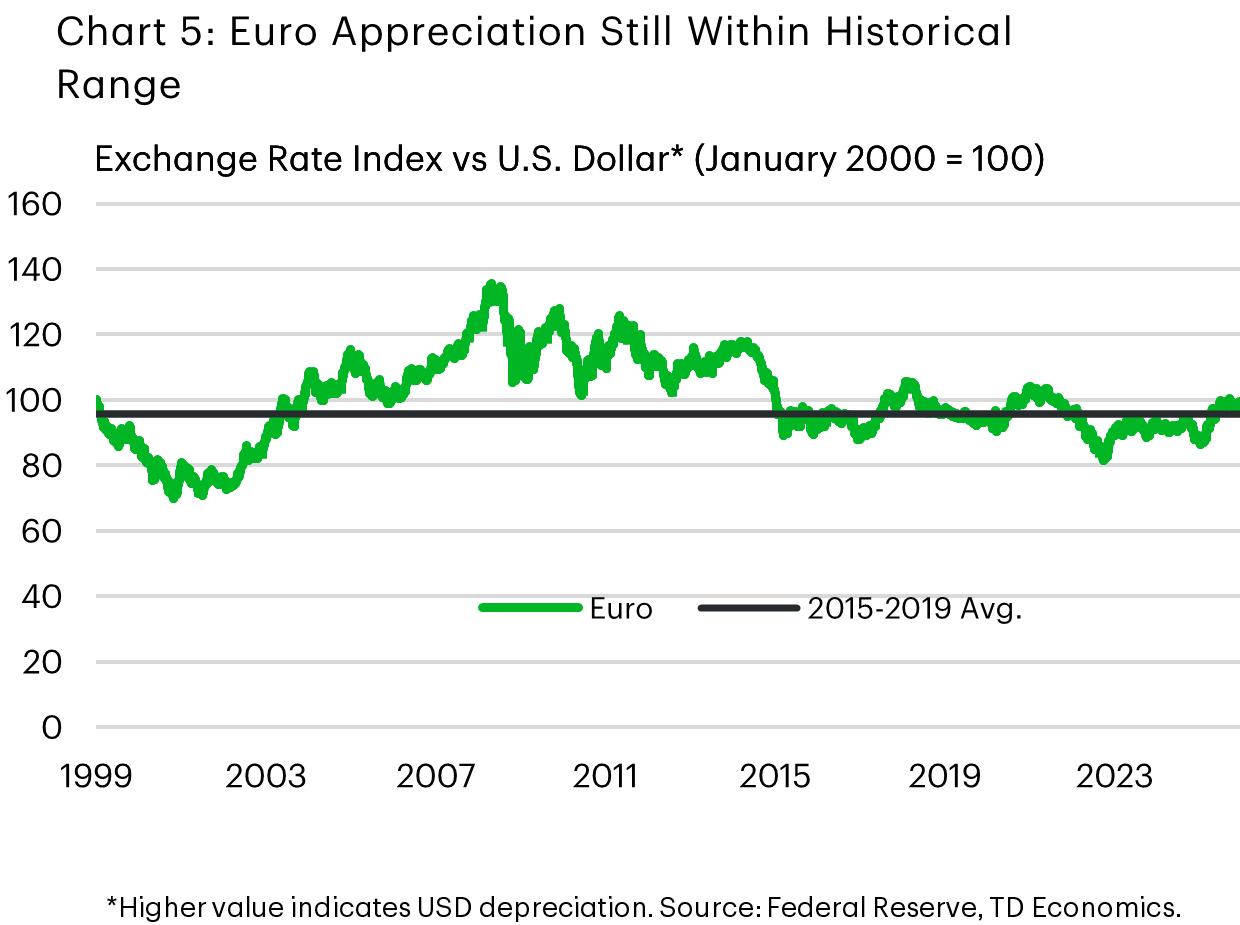

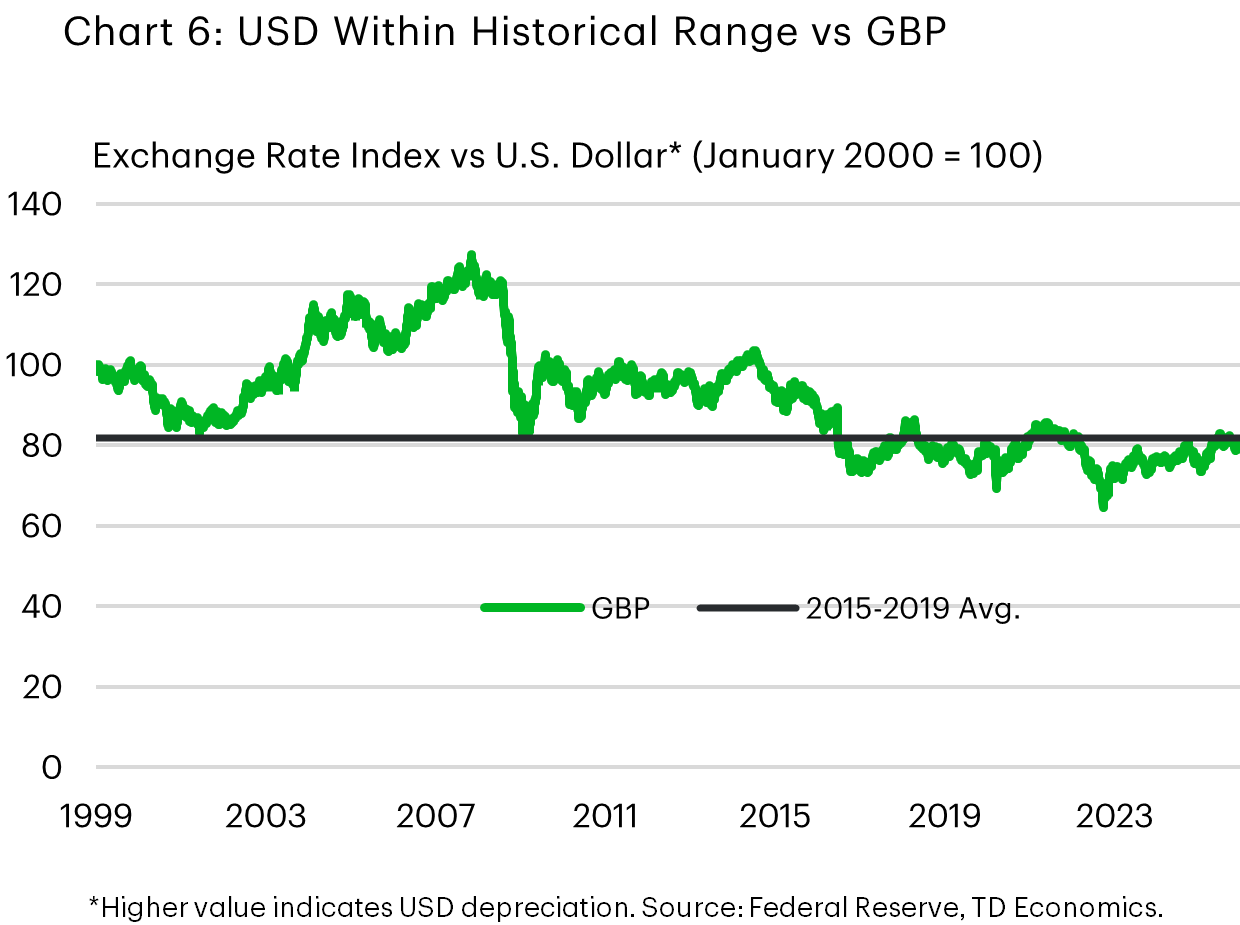

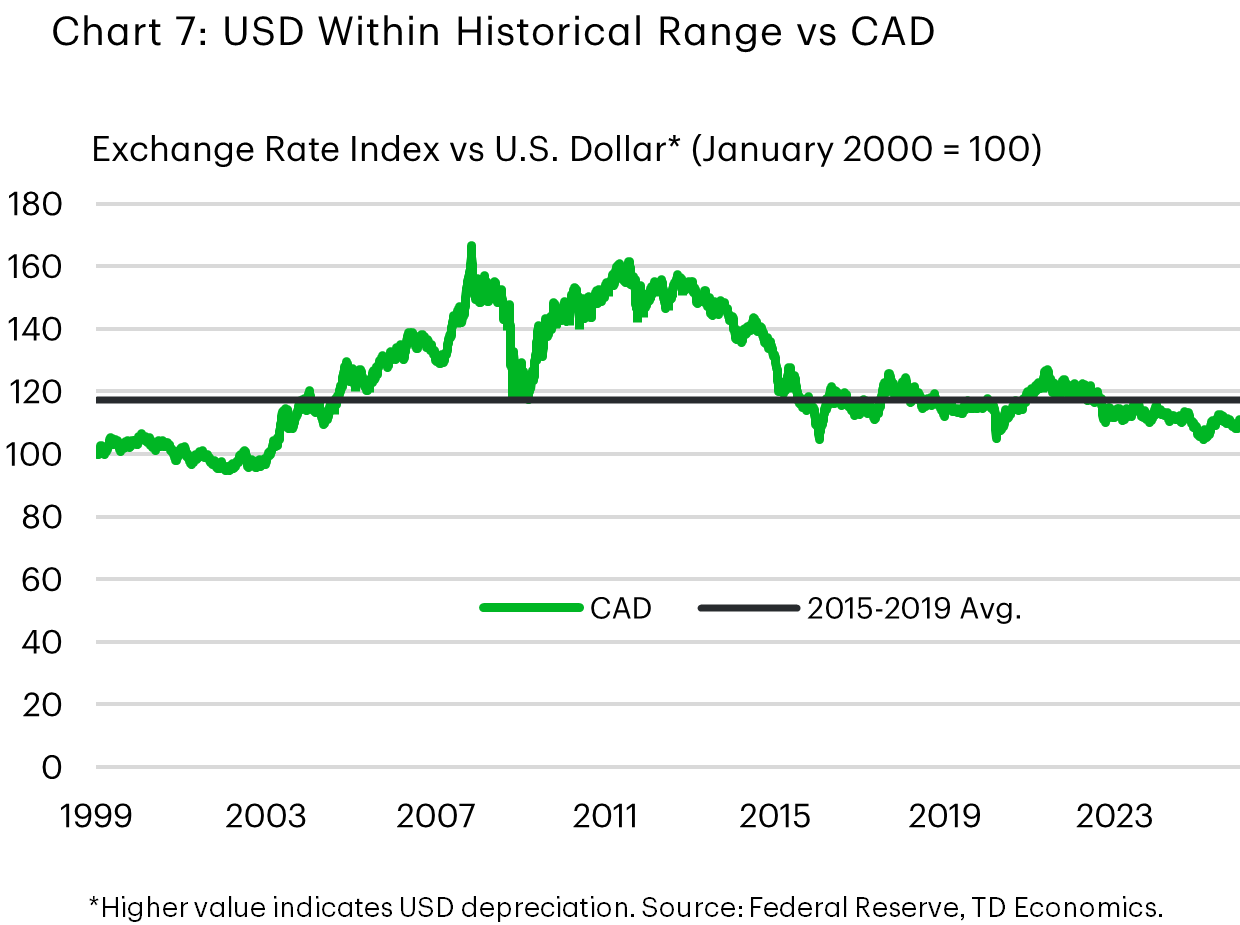

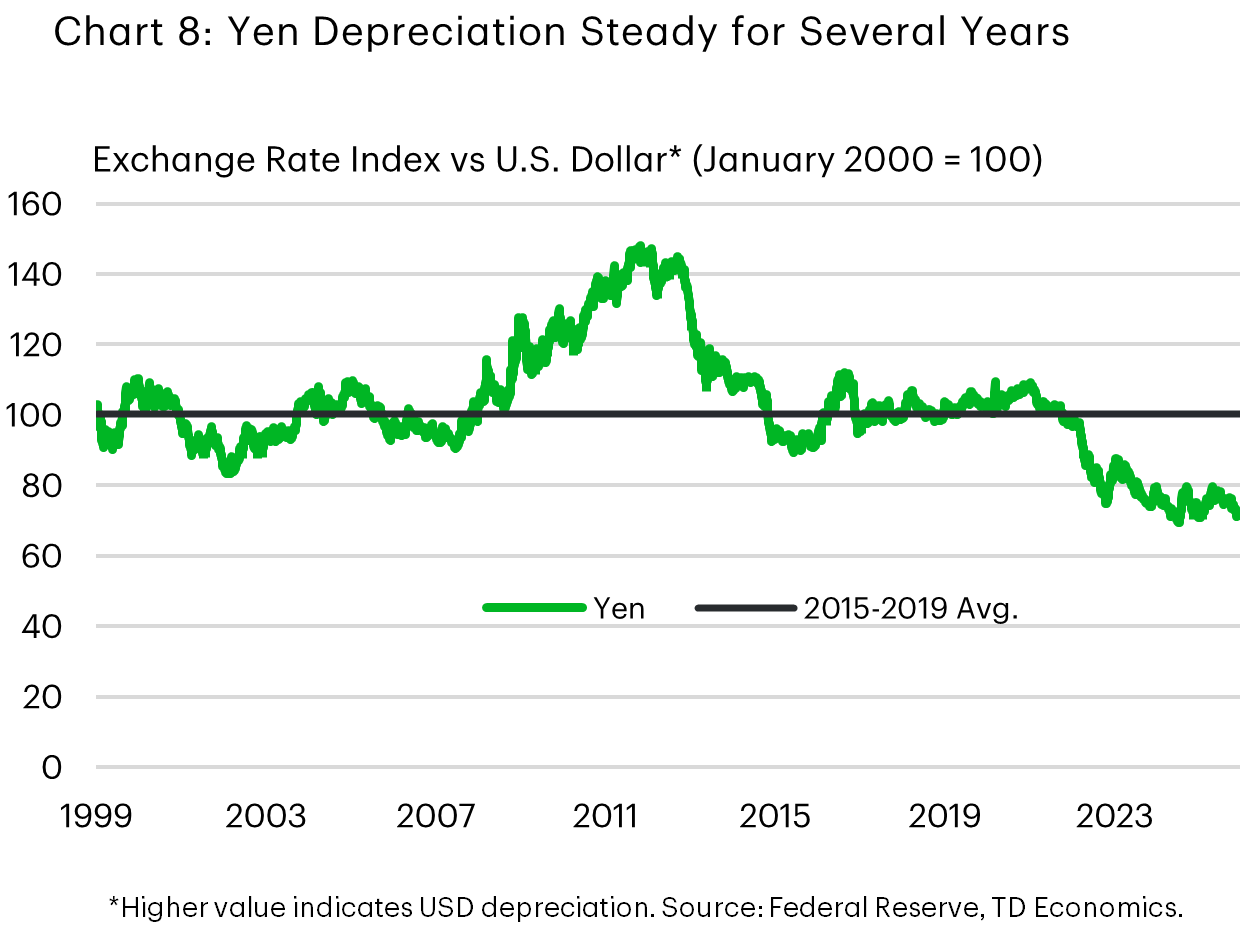

Taking a look under the hood, the U.S. dollar lost ground across board last year, led by a nearly 15% depreciation against the euro and a 9% depreciation against the pound sterling. Smaller 6-8% drops were recorded vis-à-vis the Canadian dollar and the Australian dollar, while the USD was roughly flat against the Japanese yen. The USD was not alone in depreciating against the euro, which reached an all-time high in trade-weighted terms in September, benefiting from perceptions that Europe’s fiscal and strategic shift would raise growth in the coming years.

Charts 5-8 show 2025-ending levels for the dollar against their major counterparts. Against the euro, the pound, and the Canadian dollar, the dollar now trades close to its 2015–2019 averages. Bucking the trend is the yen, which sits well below its pre-pandemic levels, hit by concerns around the direction of Japanese fiscal policy, and more recently, the pro-stimulus, expansionary policy bent of the new Prime Minister.

Further downside in store for 2026

We are not expecting a repeat of 2025 but do see scope for a further USD modest depreciation on the order of 3% in the year ahead. U.S. growth is likely to be a relatively neutral factor on the dollar, as the U.S. continues to outperform most other developed market currencies. However, the rate-differential story will likely translate into some downdraft in the greenback against the euro, CAD, and GBP. The other major central banks have largely concluded their easing cycles, but we see room for the Federal Reserve to lower interest rates this summer. While additional monetary easing is already priced into the market, we still see further selling pressure as the specter of the cuts draws nearer.

We see this modest appreciation shared across most of the majors. In Canada, a continued gradual easing in trade uncertainty is likely to support a 2-3% bounce in the Loonie to around the 0.74 CAD per USD level. A similar gain is expected in the euro (to around 1.20) predicated on promised fiscal expansions and defense spending commitments materializing. On the flip side, the yen appears oversold, and should start to the turn the corner, though a snap election set in Japan in the coming weeks and a period of heightened uncertainty about the direction of policy could keep it below 150 to a dollar for longer.

Based on our estimate, the trade-weighted USD is currently at a level not far off its fundamental value and consistent with our baseline macro outlook. Thus, a large move from the prevailing level would likely take the realization of major downside or upside surprise, such as a major geopolitical event, a more durable erosion of central bank independence than we have seen to date, or a significant change to the economic growth outlook.

What about “De-dollarization”?

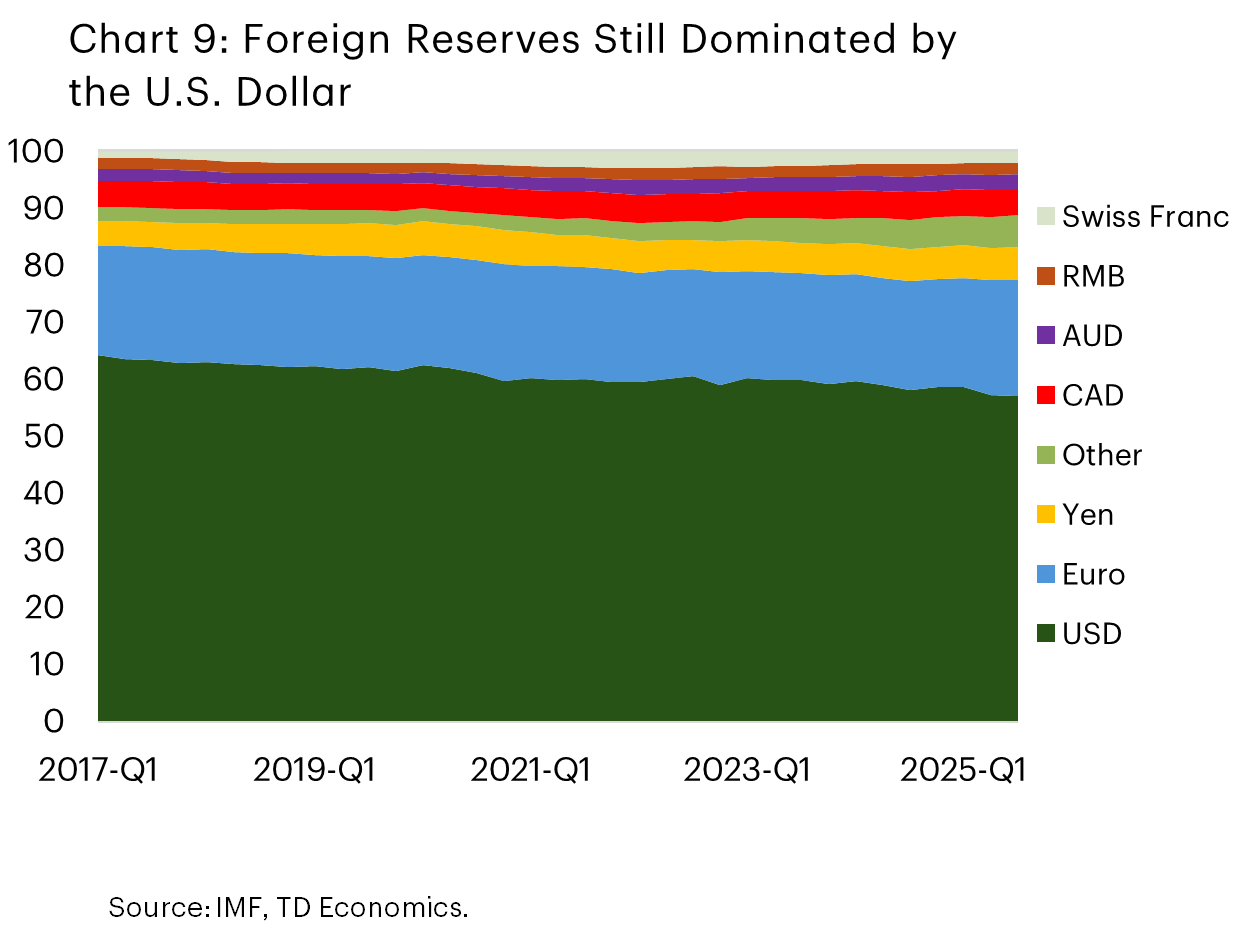

Turning back to the “de-dollarization” theme that has made lots of hay over the past year, the truth of the matter is that a gradual move away from the greenback has been ongoing for many years. For example, official foreign exchange reserves have been slowly, but steadily, trending away from the greenback (Chart 9). The small move down we see over 2025 in the USD share of official reserves is almost entirely attributable to the depreciation and not official sales of USD reserves2, which is to say that 2025 largely looks like another year on the same trend, rather than an abrupt shift in the status and perception of the dollar.

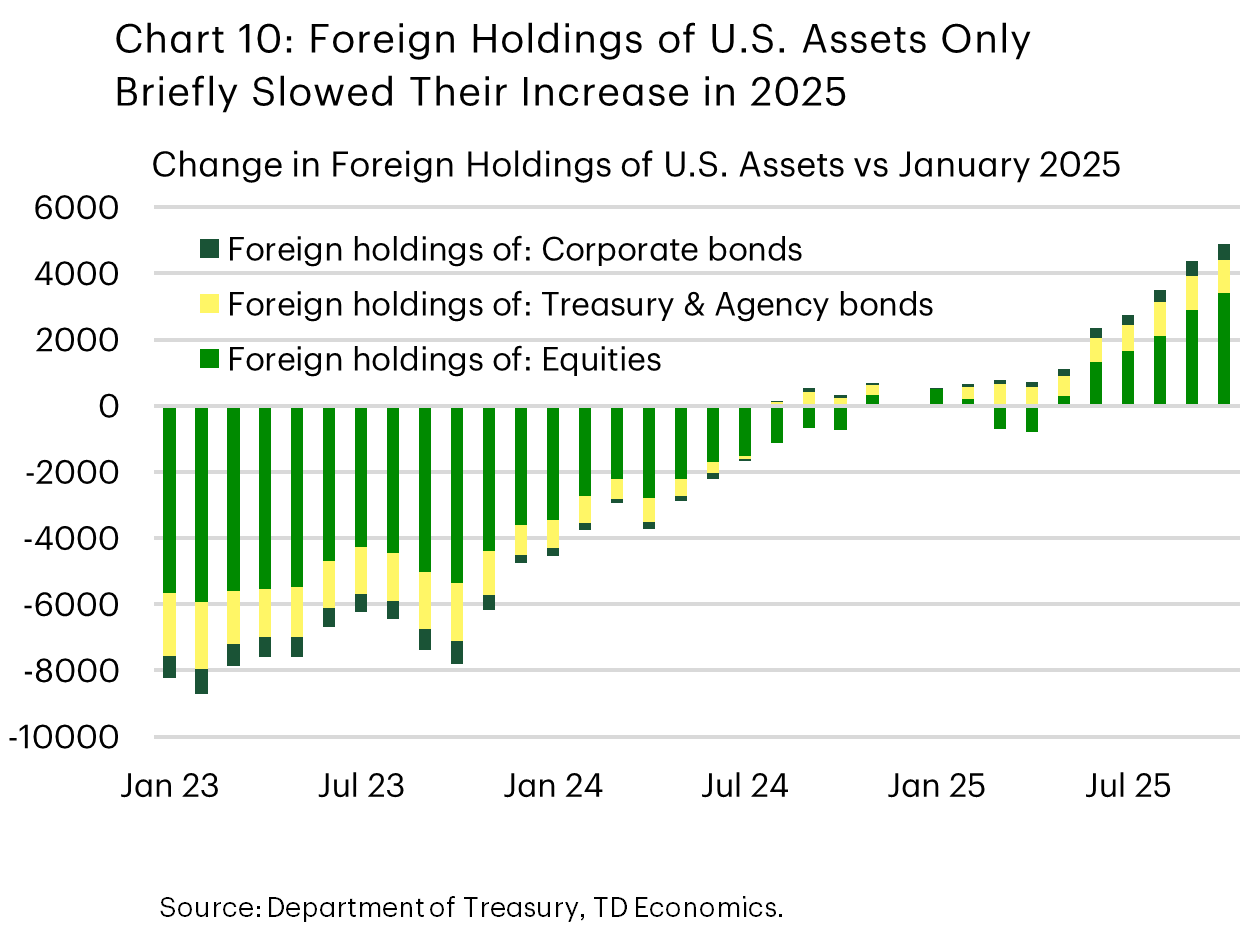

We also do not see a prolonged decrease in investor appetite for U.S.-dollar assets; in fact, foreign investors had a healthy appetite for US dollars in the second half of 2025. There was a brief pause in foreign investors’ accumulation of U.S. assets in early-2025 and outflows in April and May, and accumulation resumed thereafter (Chart 10). Undoubtedly, some of the factors we previously touched on were on the minds of investors – the expanding deficit, the uncertain impact of tariffs, and the change in the Federal Reserve’s stance all seemed to come together to briefly sour sentiment on the dollar in those months, but this was clearly temporary. The $US 4 trillion inflow into USD assets show in Chart 8 likely dwarfs the flows into alternative assets such as crypto and gold over 2025 – and stablecoin demand is actually positive for the USD in its current form, since most are backed by the USD. Gold had a banner year in 2025, but available data show that flows into gold-related funds were a small fraction of broader flows into USD assets, around $US 100 billion in 20253.

This underscores that there is no clear alternative to the U.S. dollar, even while there may be appetite for one. Competitors such as China have sought alternatives that would free it and the countries it has close economic ties with from reliance on the U.S. dollar and the associated constellation of financial architecture. It created the Cross-Border Interbank Payment System to build a cross-border payments network that settles transactions in yuan to further this end. While the growth in this system has been substantial, having seen participation by over 18 countries and exceeding US$50 billion in daily transactions, the RMB still only accounts for a low-single-digit share of global cross-border payments. Related initiatives underway elsewhere the world. The European Union, for example, is moving to adopt a digital euro, which would allow electronic retail payments to occur without the involvement of payment processors (primarily U.S. businesses), but this is not yet fully approved and remains years from being operational.

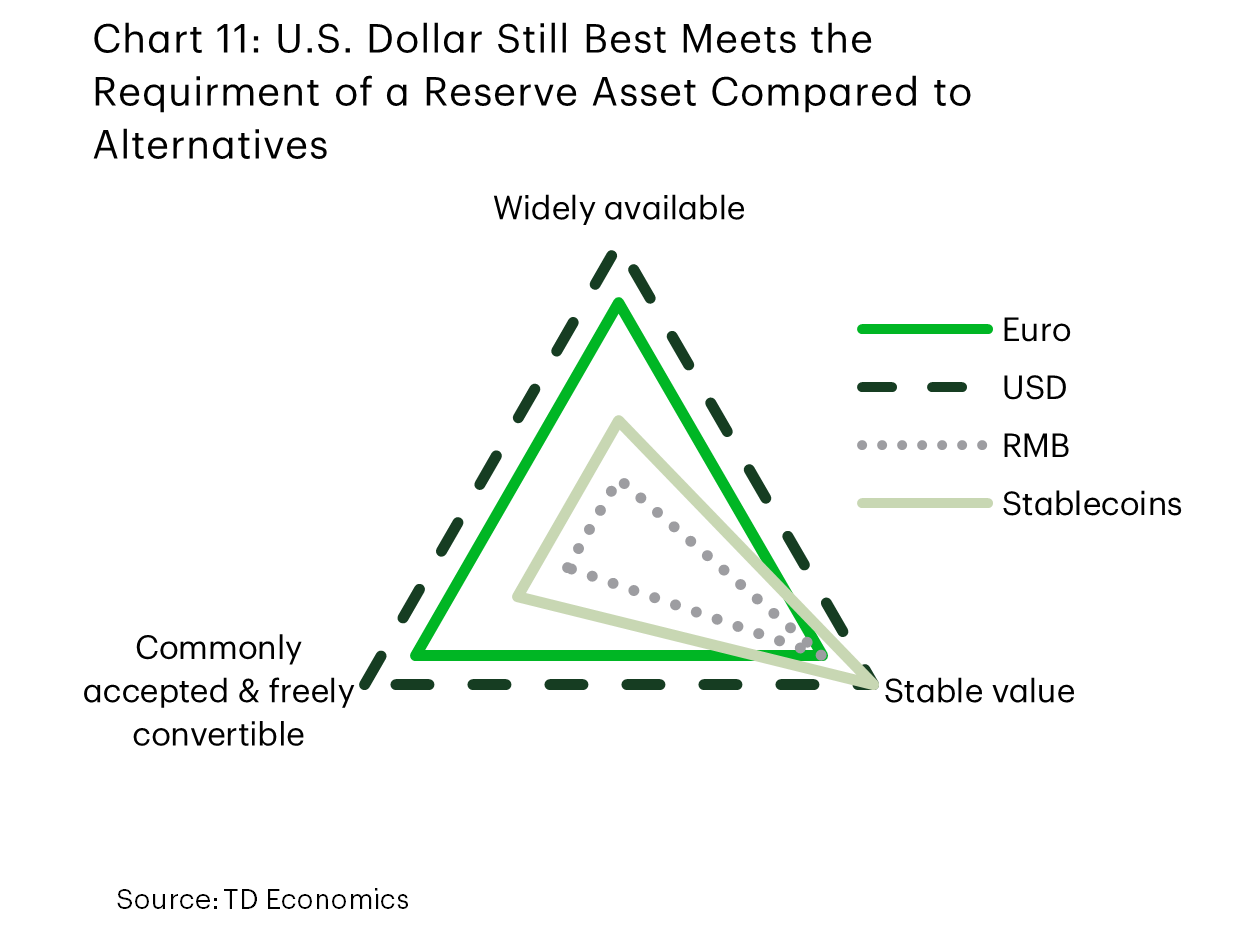

It is all but certain that many economies’ quests to reduce their reliance on the U.S. dollar will continue apace in the coming years, but completely displacing the USD as the global reserve currency and the central currency in international trade and finance is not realistically in the cards. Chart 11 shows how the closest competitors, in our view, lack the characteristics necessary to take on the role of a reserve asset. The U.S. dollar and U.S.-dollar denominated assets exist in far greater supply and have shown to provide more liquidity than the closest substitutes that exist today.

As it stands, there is little evidence that de-dollarization has accelerated. Flows into dollar-based assets have returned to trend, dollar use has been relatively stable, official reserves are mostly unchanged, and the world still lacks a convincing alternative. The U.S. dollar remains, by far, the most widely available, freely traded, and commonly accepted currency, in part because it has been issued by the world’s largest economy for nearly eighty years now. This is a privileged position that it cannot be dislodged from quickly.

Going forward, we expect that the international financial system will continue to become more multi-polar and less dominated by the dollar, as innovations in payments technologies continue, rivals further development of competing architecture to the existing dollar-based systems, and alternatives expand in size. But this gradual diversification away from the U.S. dollar globally still leaves the greenback in a leading position for some time to come.

. This marked an end to a fairly steady run of appreciation since the end of 2023.){kind=link}