Summary

We know from our many client discussions that there appears to be at least some degree of comfort with a Warsh led Fed vs. the other choices. But, we all should be mindful that there is also some degree of uncertainty associated with this pick if for no other reason than his public remarks on the economic outlook and the appropriate path for the federal funds rate have been fewer and farther between than the other finalists.

We generally expect Chair Warsh to support a more dovish stance on monetary policy driven in part by his optimism over productivity growth as well as his view of the need for lower rates to support “Main Street.” And of course, a dovish slant is what President Trump wanted. That said, Warsh has historically been among the most hawkish of the four finalists on President Trump’s shortlist. Warsh’s reputation as a hawk stems from his time as a Fed Governor and during his post-Fed career.

Although Warsh’s comments on the fed funds rate have been infrequent in recent months, he has maintained a belief that the Fed’s balance sheet is too large—a belief he has long held and another factor that has contributed to his hawkish reputation.

We think it is highly unlikely that the Fed will shrink its balance sheet materially under Chair Warsh given how entrenched the “ample reserve” operating framework is in the financial system. Stated differently, there are no reasonably plausible scenarios where the financial system would comfortably absorb a sharp change to this stance, no matter what the leaning of the new Fed chair may be. There is a high hurdle to altering this framework.

Where we think Chair Warsh could affect more change is by de-emphasizing short-term data dependence in favor of “trend dependence”, which we believe would lead to fewer, but more seismic, inflection points in U.S. monetary policy. We can also see him making a case for diminishing or even completely doing away with the Summary of Economic Projections and the Dots. We would not be surprised if he makes a case for less “Fed-speak”.

When it comes to Fed independence, Warsh has been outspoken about the need for the Fed to revisit some of its current governance policies and processes, but he has publicly maintained a belief in the importance of central bank monetary policy independence.

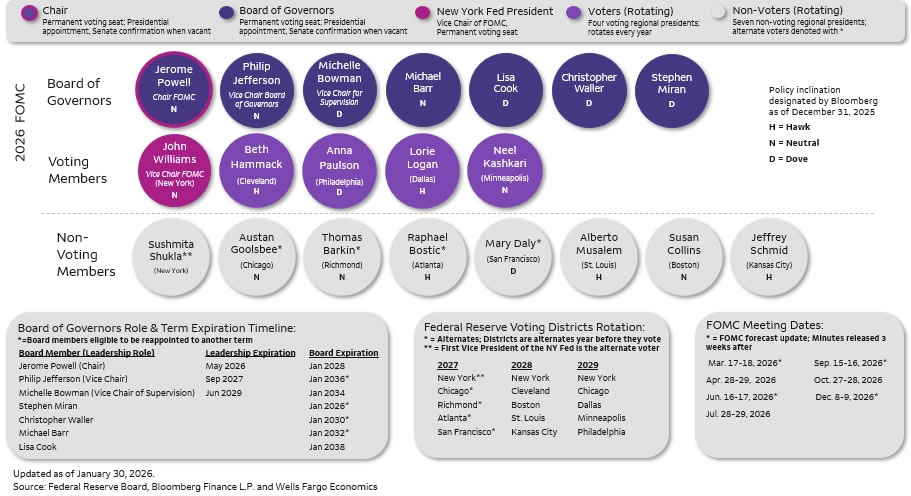

It is also important to remember that monetary policy decisions are a Committee decision. Seven governors vote at each meeting in addition to five of the 12 regional Fed presidents. This ensures some continuity in the makeup of the FOMC as it transitions. Accordingly, we do not anticipate making any changes to our fed funds forecast, although as we have stressed elsewhere, we continue to see risks to our call.

We would give you just two more things to consider. Warsh has some challenges that start almost right away. First, does he act as a shadow Fed chair? If he is going to second guess Powell at every turn or forcibly disagree with him, he may appease his new boss, but he runs the risk of alienating himself to the rest of the Committee. We think Warsh knows this and will tread carefully around that, but it’s a risk. And second, what kind of consensus builder will he be? Criticize Powell as much as you like (and yes, we have been critical of him at times), but he is one heck of a consensus builder, carefully crafting and selling his message to members ahead of meetings. This will be critical for Warsh. The expectation is he wants to cut, perhaps even more aggressively than market pricing. If that is indeed the case, he has his work cut out for him in building a consensus toward that when the expectation of the Committee at large is just for one more cut per the dots (where we think the hurdle is growing higher even for that).

For those that want to read on, below you’ll find more detail about his background and our analysis of his direct quotes over the years…

Warsh’s Windy Path Back to the FOMC

Like current Fed Chair Jerome Powell, Kevin Warsh does not hold a PhD in economics but has prior experience in the financial industry and public policy. After obtaining a law degree from Harvard in the mid-1990s, Warsh went on to work on Wall Street before holding several positions in the George W. Bush administration, including executive secretary to the National Economic Council. From 2006 to 2011, he served on the Federal Reserve Board of Governors. Although Ben Bernanke, Janet Yellen and Jerome Powell also served on the Board prior to their appointments as Fed Chair, Warsh’s tenure is not as recent as his predecessors’ was when they assumed the Chair (Figure 1). Warsh has not served in government since his time at the Fed, although he has remained active in public policy circles. He currently serves as a distinguished visiting fellow at the Hoover Institution.

A Hawk Dressed in Dove’s Clothing?

Public comments by Warsh last summer revealed he was in favor of reducing rates prior to the Committee cutting the fed funds rate at its three final meetings of 2025, noting simply in an interview on July 8, that “interest rates should be lower.” Driving his rationale for a lower fed funds rate at the time was the sluggish state of the housing market but, more predominantly, optimism that the economy was on the verge of a productivity boom. Such a resurgence, traced to AI and other “pro-growth policies” adopted by the Trump administration, would act as a disinflationary force, in his view.

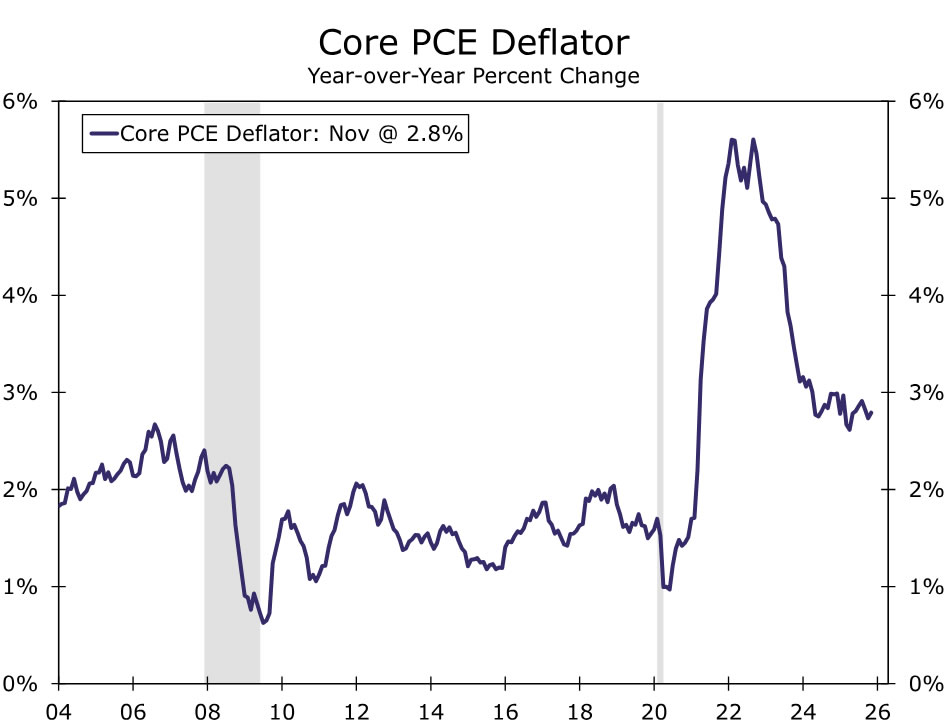

We have significantly less conviction about how far Warsh would aim to reduce the fed funds rate compared to other candidates that were on President Trump’s short list. Warsh’s lack of recent remarks on the policy rate as well as his historic reputation as a hawk inject more uncertainty into the monetary policy outlook than a Chair Hassett or Chair Waller would have generated, in our view. Warsh’s hawkish reputation was earned due to his focus on upside risks to inflation during his time as a Fed governor from 2006-2011, including in the spring of 2008 when inflation was a little over 2% but the economy, as we now know in hindsight, was already in recession (Figure 2). He was also an outspoken critic of the Fed engaging in multiple rounds of large-scale asset purchases (i.e., quantitative easing) in the early 2010s when the fed funds rate was constrained by the zero-lower bound. In short, there are more questions than answers about a Chair Warsh, in our view, and we expect the market to be sensitive to his public remarks in the coming months as everyone assesses his outlook on monetary policy.

While less concerned about inflation today, Warsh has remained critical of the size of the Fed’s balance sheet. In a November Wall Street Journal op-ed, he said that “the Fed’s bloated balance sheet…can be reduced significantly.” With the Fed owning 14% of Treasury securities and 25% of agency MBS, reducing the balance sheet significantly would, all else equal, put upward pressure on longer-term borrowing costs. Warsh believes that these upward effects could be offset by cutting the fed funds rate further. He views the size of the Fed’s balance sheet as having disproportionately benefited large companies and “Wall Street” in lieu of “Main Street” and the broader economy.

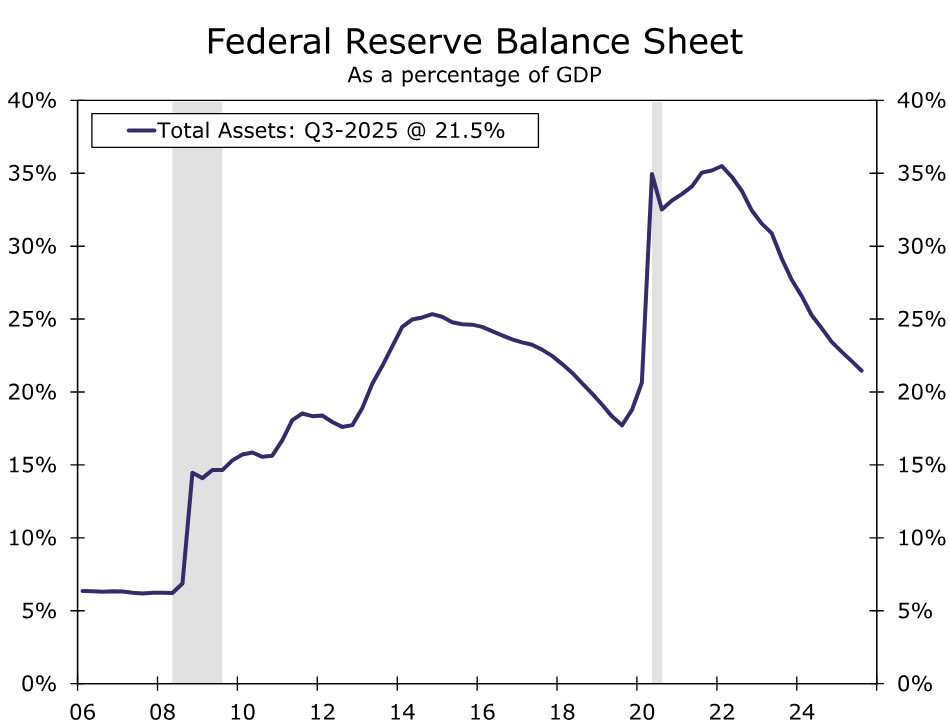

We would not expect Warsh to meaningfully shrink the balance sheet in his tenure as Fed Chair. The Fed’s shift to an “ample reserve” operating framework makes reducing the balance sheet to pre-2008 levels as a share of GDP very unlikely (Figure 3). As recently as the FOMC’s meeting in December, the Committee voted to initiate purchases of shorter-term Treasury securities to maintain an ample supply of reserves and ensure effective short-term interest rate control. Furthermore, a smaller balance sheet could be at odds with President Trump’s preference for lower longer-term borrowing rates generally and lower mortgage rates specifically, leading us to question how ardently Warsh would push for a smaller balance sheet as Fed Chair.

One other view from Warsh that struck us as important in his history of public remarks is his disdain for near-term forecasting, forward guidance and data dependence. These themes have come up repeatedly in his public remarks, such as in his G30 speech at the IMF Spring Meetings last April.1 The following remarks from a 2017 op-ed in the WSJ capture the sentiment well: “The Fed should adjust monetary policy only when deviations from its employment and inflation objectives are readily observable and significant. The Fed should stop indulging in a policy of trying to fine-tune the economy. When the central bank acts in response to a monthly payroll report, it confuses the immediate with the important.” Under Chair Warsh, individual data points and Fed speak may move markets less than they did under Chair Powell if Warsh adopts a more medium-term and less near-term perspective on monetary policy. The “insurance cuts” taken out at various times under Chair Powell might become less common, for example. That said, under this framework, inflection points may become less frequent but more seismic at times when the Chair attempts to change course.

Would Monetary Policy Independence Be Maintained Under a Warsh Fed?

We are of the view that Kevin Warsh as Fed Chair would not be a major threat to U.S. monetary policy independence. Warsh has argued for a “strategic reset” at the Federal Reserve after “institutional drift” and, in his view, a loss of credibility. But when it comes to monetary policy, Warsh believes Fed independence is “essential”, provided that when “monetary policy outcomes are poor, the Fed should be subjected to serious questioning, strong oversight, and when they err, opprobrium”.

While Warsh would likely be apt to revisit current governance and processes at the Fed, we do not think his chairmanship would greatly alter the near-term path of monetary policy. It is important to remember that monetary policy decisions are a Committee decision. There are seven governors voting at each meeting in addition to five of the 12 regional Fed presidents (Figure 4). This ensures some continuity in the makeup of the Committee as it transitions from one led by Jerome Powell to one led by Kevin Warsh. It is our view that if an incoming Chair were to propose monetary policy that is significantly out of line with what economic conditions warrant, then there would be major push back by most of the FOMC.

Of more importance to Fed independence, in our view, are the multiple legal challenges the Trump administration has brought to current Board members. The case regarding the dismissal of Fed Governor Lisa Cook is currently pending with the Supreme Court. If the court rules in favor of the administration, it could grant presidents sweeping authority to dismiss Fed governors for cause. This would set a precedent for future administrations to take advantage of and allow the executive branch to adjust the composition of the FOMC in a more material way. The Department of Justice investigation of Chair Powell’s Congressional testimony similarly holds higher stakes than the appointment of a new Chair in our view. If criminal charges can be brought against FOMC members, they are more likely to bend to the president’s will. Our base case is that the Supreme Court will establish a relatively high bar for dismissing a Fed governor for cause and the DOJ will not pursue charges against Powell. But if we are wrong on either front, we view such legal developments as a significantly bigger threat to Fed independence in 2026 than the appointment of Kevin Warsh as Fed Chair.

{kind=link}