Summary

The 4.7 point jump in the ISM manufacturing index is consistent with our call for a modest broadening in capital expenditures and manufacturing activity, though some year-end replenishing amid trade uncertainty could be exaggerating momentum. Prices at 59.0 is not terribly encouraging for the efforts to get inflation in check.

“A new year, with new challenges”

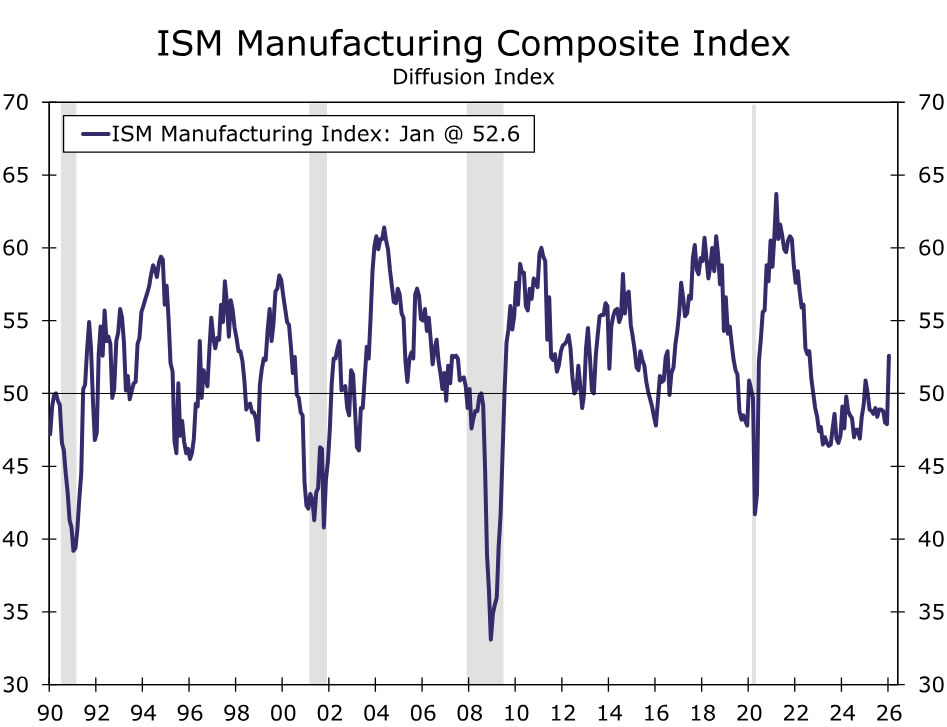

The ISM manufacturing index crossed back over into expansion territory after 10 straight months in the purgatory of contraction last year. Today’s 52.6 reading for January signals a welcome bit of relief for manufacturing even if some year-end quirks are giving only a temporary boost to the numbers in today’s report (chart).

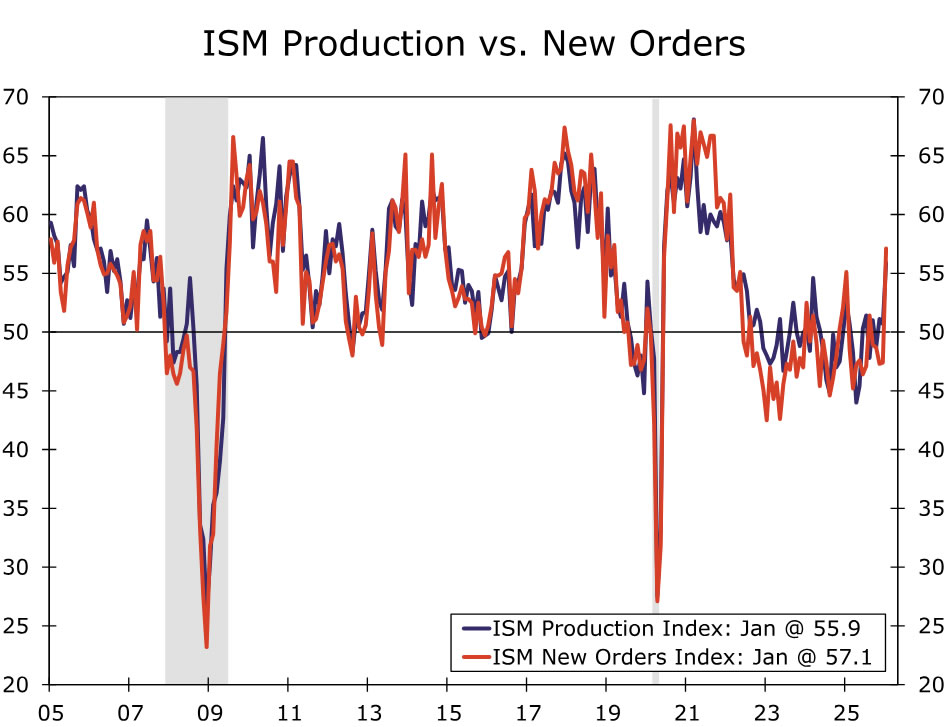

Three out of five of the subcomponents that feed into the headline for the ISM manufacturing index are now in expansion territory. The biggest overall move was in new orders which jumped 9.7 points to 57.1 (chart). That’s the biggest one-month pop outside the pandemic since 2001 and signals the fastest pace of expansion for this forward-looking measure in nearly four years. While we’ve highlighted the broadening out in durable goods orders as a signal traditional manufacturing and cap-ex might be gaining traction, this likely overstates the extent of order expansion as the release noted “post-holiday replenishment and customers’ desire to get ahead of additional tariff-driven price increases as possible reasons for the increase [in orders]”.

Supplier deliveries came in at 54.4 in January and that too lifted the headline, although we should be wary of long wait-times amid evolving trade tensions. Production also jumped 5.2 points to hit 55.9 suggesting a somewhat brighter assessment of production despite lackluster industrial production data.

The select respondent comments continue to strike a tone of caution around activity due to tariffs. Nearly all respondents made direct mentions of tariffs last month, while three industries (Computer & Electronic Products, Chemical Products and Apparel & Leather) specifically mentioned moving manufacturing out of China. Others noted supply chain volatility, the inability to plan long-term and profit misses because of tariff costs.

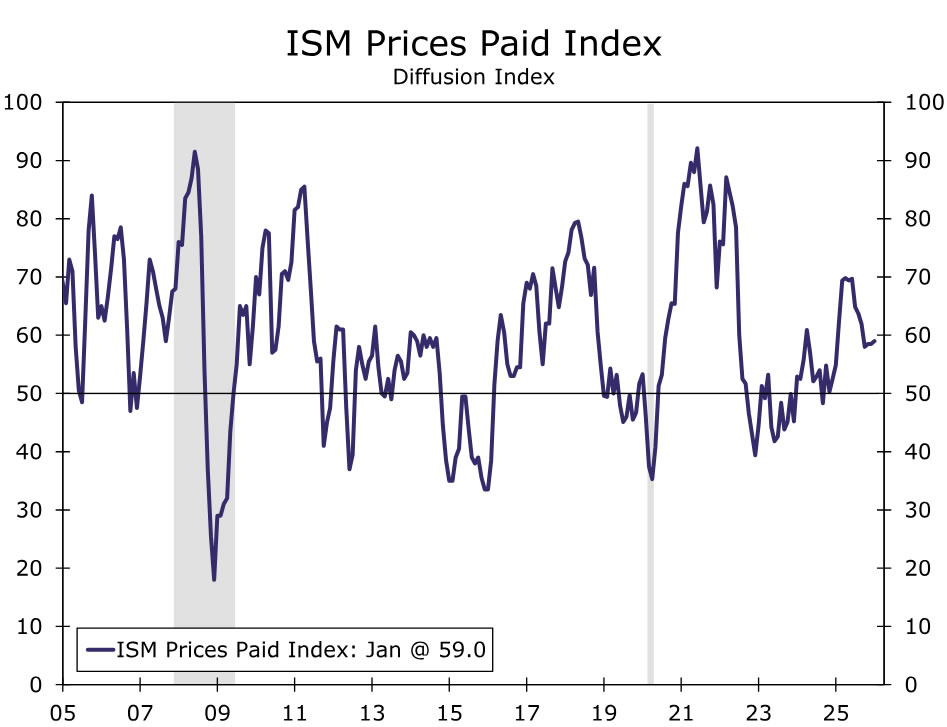

The prices paid index inched higher to 59.0, indicating some stubbornness in prices with 11 industries reporting paying higher prices for raw materials last month (chart). Just under 30% of respondents reported paying higher prices, which is the highest in at least four months, but remains well below the 49.2% that reported so back in April 2025.

The employment index registered its highest reading in a year, although at 48.1 it remains consistent with a contraction in hiring in the sector. The release also noted that “for every comment on hiring, there were two on reducing head counts.”

We continue to anticipate a modest broadening in capital expenditures this year, and even if the latest data overstate the current run rate of growth, the January ISM ultimately suggests some sign of stabilization in underlying manufacturing activity.

{kind=link}