The U.S. administration’s response to the Supreme Court’s ruling against IEEPA tariffs could overshadow economic data releases in the week ahead. We have noted before that the government has multiple options to reimpose those measures using other legislation.

And, in Canada’s case, an exemption for CUSMA compliant trade means most exports were already exempt from IEEPA tariffs with product specific section 232 tariffs (not impacted by the ruling) the main source of tariffs on Canada (Issue in Focus for more).

We continue to view maintaining CUSMA-related exemptions more important for Canada than the IEEPA ruling itself.

Canadian GDP growth appears to have stalled in Q4

International trade uncertainty and volatility has been a persistent feature in the growth backdrop over the last year, but we expect a flat Q4 gross domestic product reading for Canada next Friday was in part due to temporary disruptions in the economy with signs of stronger activity late in the quarter.

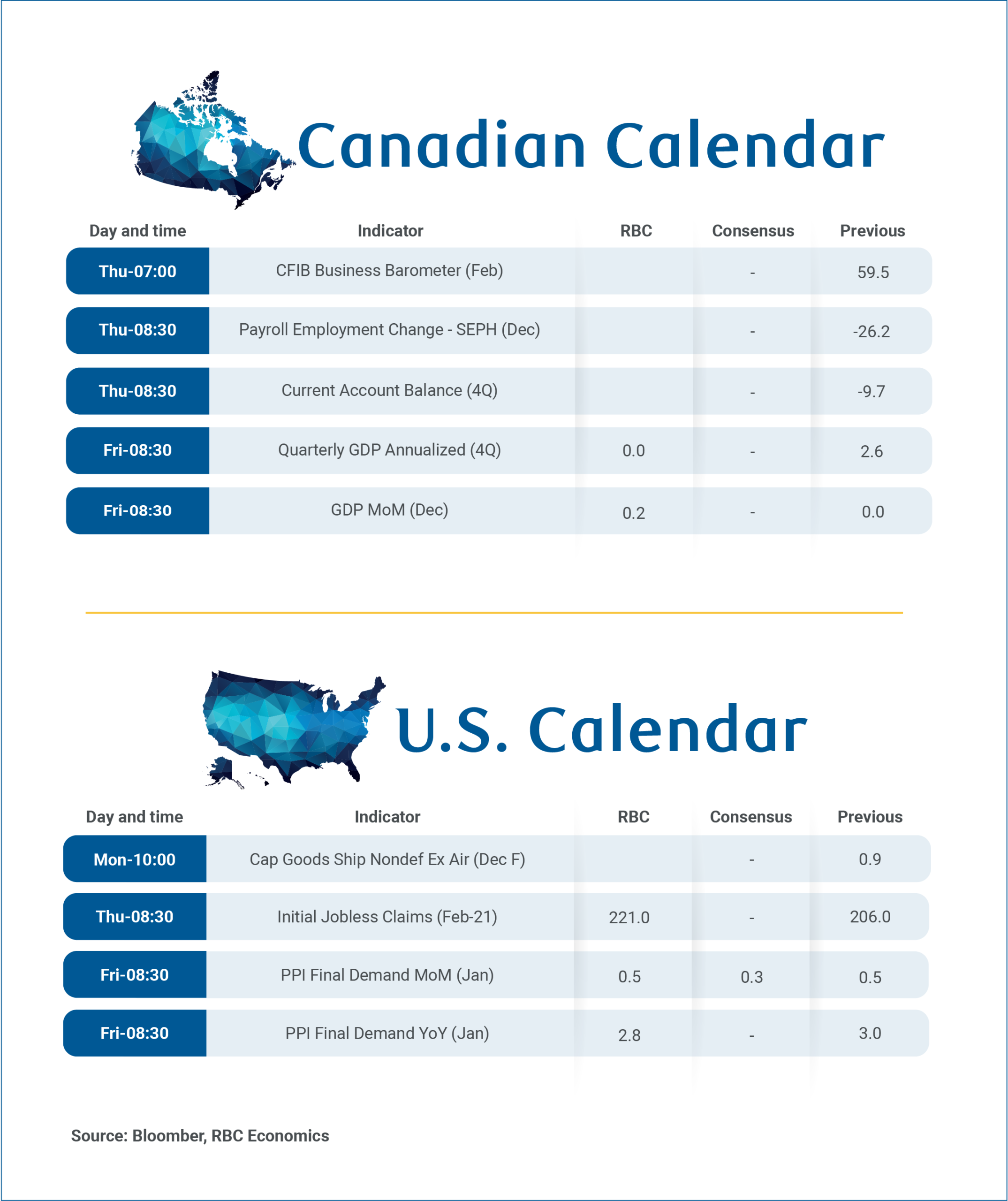

Following two soft growth prints in October and November, we expect a 0.2% increase in December that would be slightly above Statistics Canada’s 0.1% advance estimate. That would leave Q4 tracking close to our (and the Bank of Canada’s) forecast for no growth after a 2.6% annualized increase in Q3.

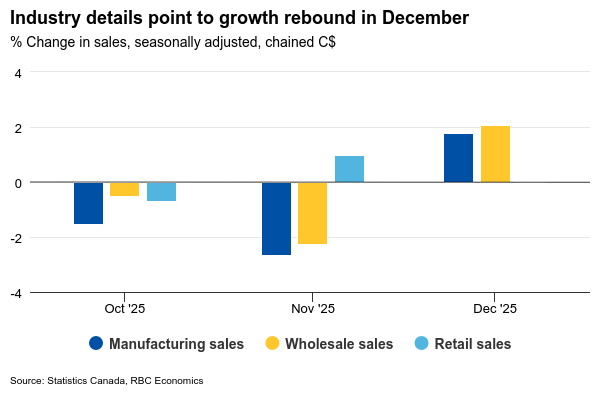

The silver lining to a soft looking quarter is that most of the weakness was concentrated in October and November with industry reports for December mostly positive.

Manufacturing and wholesale sales surged 2.1% and 1.8%, respectively, as auto production bounced back from disruptions related to a semi-conductor shortage in November. Education services in December likely recouped more of the weakness from Alberta’s teachers’ strike in October after a partial bounce back in November.

Those disruptions—along with impact from a postal strike in October—combined to subtract almost three-quarters of 1% from annualized Q4 GDP growth, according to our estimates.

Still, soft spots remain. The manufacturing sector continues to struggle from U.S. tariffs. Home resales pulled back in December (and again in January), and retail sales were unchanged from November.

Rise in business investment but residential likely fell

We expect to see a pick-up in business investment in Q4 as key indicators like electrical equipment and parts’ imports rose.

Moderating trade uncertainty likely helped with stabilizing sentiment and investment intentions. Most companies surveyed in the BoC Q4 Business Outlook Survey didn’t expect further deterioration in the tariff and trade backdrop going forward.

Residential investment likely contracted after bigger increases in Q2 and Q3, given declines in home resales, construction and housing starts in Q4. Elsewhere, household consumption and net trade likely grew modestly although our tracking of RBC card spending data pointed to a drop-off in consumers’ buying momentum (especially among discretionary items) in January.

The BoC already assumed flat Q4 GDP in their January forecasts, and much of the weakness appears to have been due to one-off factors. In the meantime, labour markets continue to show signs of improving with the unemployment rate broadly edging lower.

With interest rates already bordering stimulative levels, we don’t think it’s likely or necessary for the central bank to cut again.

{kind=link}