- We expect the Bank of England to keep the Bank Rate at 3.75%. Through the past couple of weeks, this has also been priced in by markets and become consensus.

- The war in the Middle East implies huge uncertainty on the outlook from here, but for now our base case remains a cut in April and another one in November.

- We will look closely at MPC members’ views on what the right policy response is, if energy prices remain elevated.

- We see risk of the significant repricing of the BoE to revert, opening up for a move higher in EUR/GBP.

At the February meeting, the BoE took a dovish turn as new analysis showed wagesetting is not the threat to inflationary pressures, the BoE previously thought it was and only a slim majority voted to keep rates unchanged.

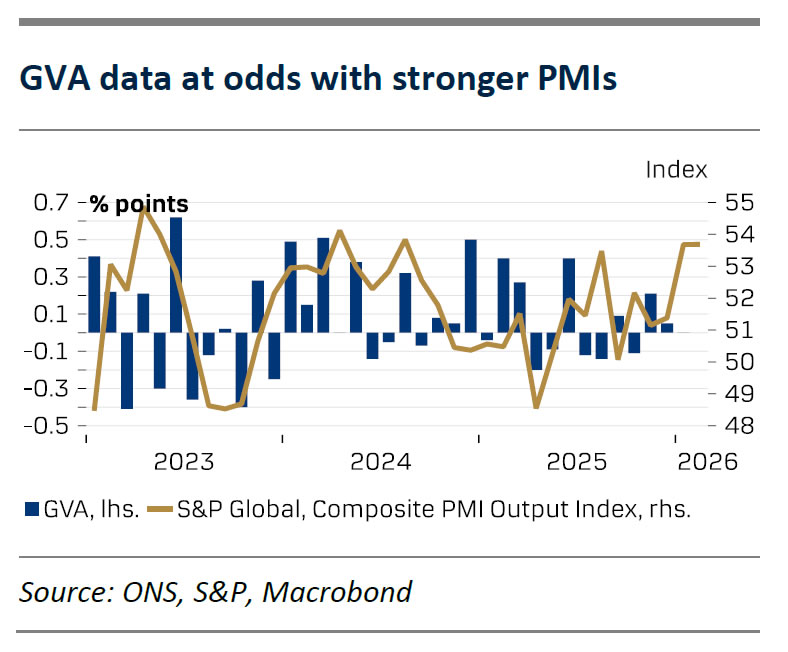

Data released since February have been mixed with some key dovish details. PMI data have suggested the economy has picked up speed in Q1. However, January GDP data disappointed as m/m growth hit 0. January inflation was close to expectations, but wage growth is declining and unemployment has edged higher. However, the war in the Middle East has turned market pricing upside down. Ahead of the war, two rate cuts were priced in by investors this year. At the time of writing, markets are leaning towards one hike.

Given the very uncertain situation in energy markets, the most likely outcome is probably that the more centrist leaning doves, Breeden and Ramsden, flip their votes to hold for now. It will be interesting to see the different MPC members’ views on what the right policy response is, if energy prices remain elevated. Worth noticing, 5/9 MPC members are new compared to the start of the previous hiking cycle in early 2022, when the BoE was clearly behind the curve. A majority of the MPC is then likely not to make the mistake of “fighting the previous war” and hiking rates too early. Thursday, ahead of the rate decision, a fresh jobs report will be published. While it is not likely to question the decision on Thursday, it will be interesting to see if the recent trends in the labour market continue.

BoE call. We stick to our expectation of an April rate cut followed by a final one in November, leaving the Bank Rate at 3.25%. We also appreciate that the risk is, the final path of the cutting cycle will drag out.

Market reaction. EUR/GBP has gradually edged lower following the escalations in the Middle East. While the UK is still a net-energy importer akin to the euro area, the energy mix in the UK slightly favours a relatively stronger GBP vs EUR. This poses a risk to our call of a weaker GBP the coming year combined with GBP performing in a USD positive environment. However, we highlight that the UK economy remains fragile and that we see scope for the significant repricing of the BoE to revert in a larger extent than for the ECB, opening up for a move higher in EUR/GBP.

{kind=link}