- The ECB decided to leave its key policy rates unchanged with the deposit facility rate at 2.00%, as expected by markets and consensus.

- Lagarde struck a calm and balanced assessment of the implications of higher energy prices, which suggests that the ECB is not in a hurry to hike interest rates.

- We keep our call that the ECB remains unchanged at 2.00% in 2026 and 2027, with risks clearly skewed to the upside. Uncertainty is higher than usual.

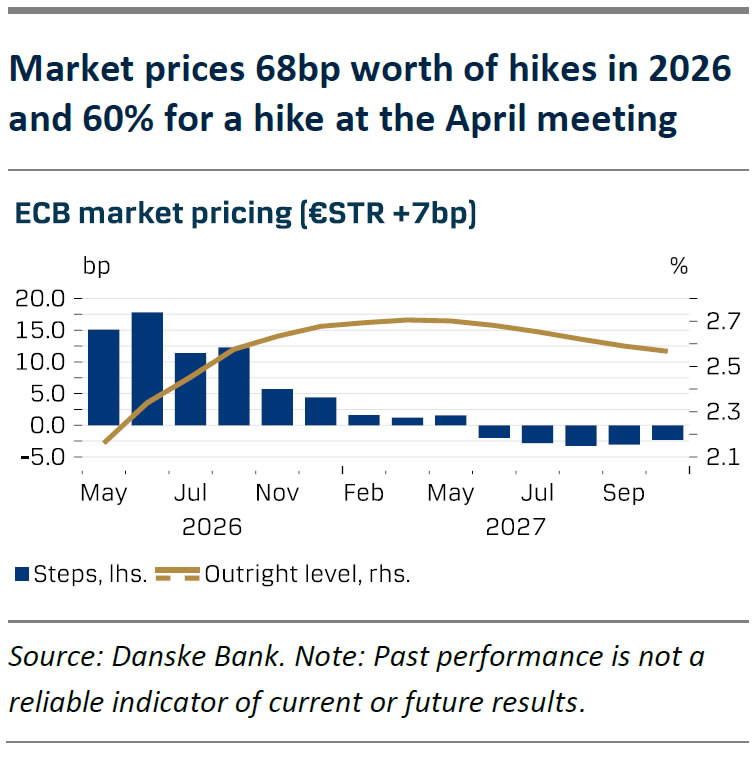

- New trade: We recommend receiving the April26 meeting at 15.5bp, as we see a high bar for the ECB delivering a hike already in April and therefore think riskreward favours a received position.

The ECB left the deposit rate unchanged at 2.00%, as expected by both markets and analysts. Lagarde struck a calm and balanced assessment of the implications of higher energy prices, which suggests that the ECB is not in a hurry to hike interest rates. She explicitly mentioned that the mood in the Governing Council was “calm”, and several times mentioned that longer-term inflation expectations remain anchored. Lagarde did not significantly emphasise the risk of second-round effects on inflation, stating only that they would remain attentive. A key argument for further ECB rate hikes – that the 2022 inflation shock has lowered the threshold for companies to pass on price increases to consumers faster – was raised in the Q&A, but she did not endorse it, saying the ECB now has a better grasp of pass-through and remains dependent on incoming data. She noted the labour market is not as hot as in 2022, while cautioning that consumers and businesses may have a fresher memory, which could increase the pass-through of higher input costs to consumer prices. Overall, we judge her tone as dovish relative to market expectations for ECB hikes heading into the meeting, as she clearly avoided a hawkish stance, which we heard from several members last week.

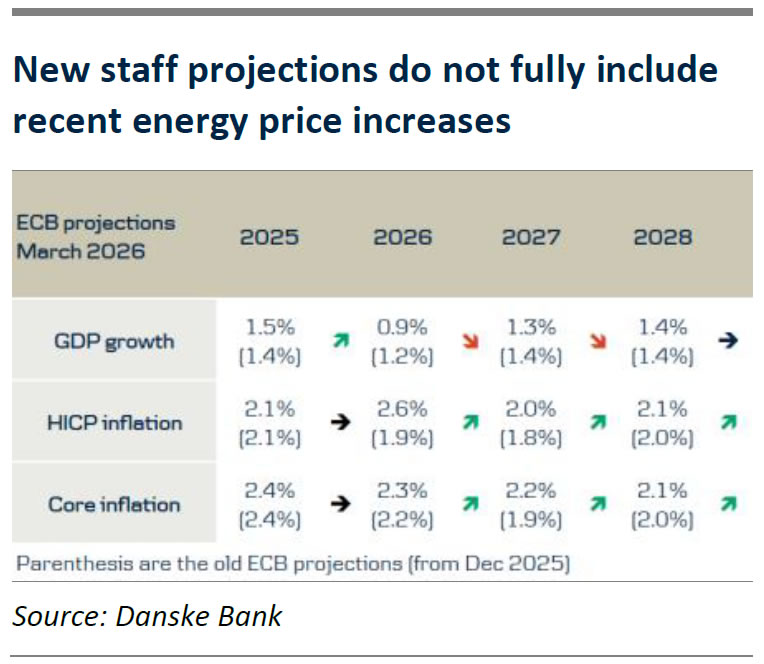

The new staff projections only partially reflect higher oil prices, as the commodity price cut-off was 11 March, implying USD83/barrel in 2026. The scenario analysis is therefore more relevant, especially the ‘adverse scenario’ that aligns most closely with current commodity futures. It assumes oil at USD119/barrel in Q2 26 and USD70 in Q3 27, and gas at EUR87/MWh in Q2 26 and EUR35 in Q3 27. In this case, HICP inflation rises to 3.5% y/y in 2026, then falls swiftly to 2.1% y/y in 2027 and 1.6% y/y in 2028, consistent with a temporary shock. If the ‘adverse scenario’ materialises, which is our base line, this should give the ECB confidence to hold rates steady, since inflation is only temporarily above target and does not affect the medium-term outlook. However, if the ‘severe scenario’ materialises, which includes a prolonged period of higher oil and gas prices with clear second-round effects on core inflation, we expect the ECB to hike policy rates several times. We stress that the uncertainty surrounding the ECB outlook is thus much higher than usual.

New trade: Receive April 2026 meeting at 15.5bp

Following today’s communication from the ECB, we recommend receiving the April26 meeting at 15.5bp (indicative mid, effective start of May) implying a roughly 60/40 probability between the ECB delivering a 25bp hike and keeping rates unchanged. While uncertainty remains high, we think the emphasis on negative growth risks, well-anchored long-term inflation expectations and little emphasis on second-round effects should keep the ECB on hold in the near term with little time until the April meeting. Historically, the ECB has been slow at reacting to shocks, with policy shifts requiring more thorough analysis and factual inflation evidence. With today’s communication, we see a high probability that this will also be the case this time around. In sum, we see a high bar for the ECB delivering a hike already in April and therefore think risk-reward favours a received position.

Our baseline is unchanged ECB rates, with a clear upside risk and higher uncertainty

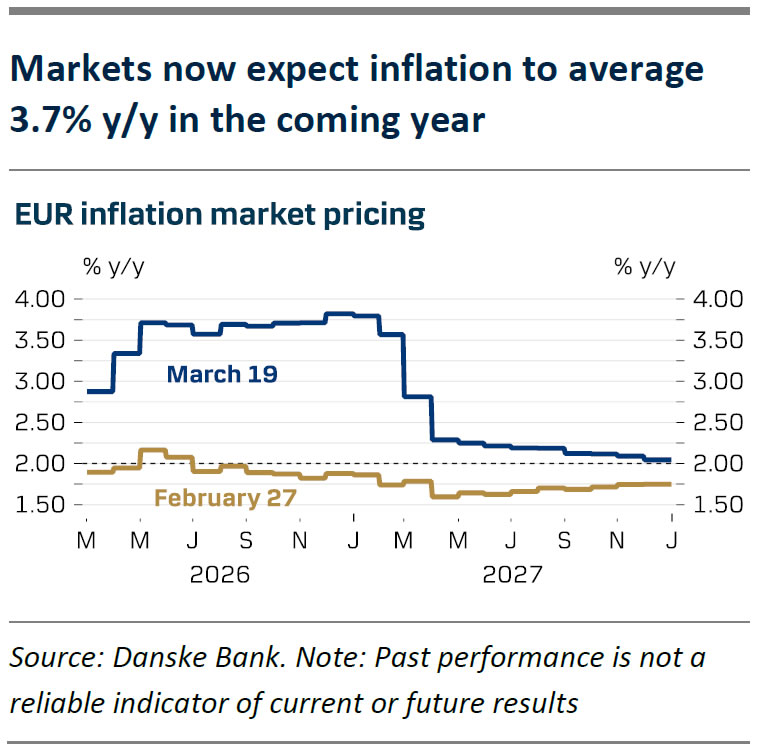

In our base case, we expect rising energy prices to have a temporary effect on the price level, but we expect only small changes to medium-term inflation due to limited pass-through to core. This is also the view of market-based inflation expectations, with the 1y1y inflation swap at 2.10% and 2y2y at 2.09%. We therefore expect the ECB to “look through” the Iran shock as growth is also negatively affected, and subsequently we do not expect the ECB to raise policy rates in 2026 nor 2027. A further rise in energy prices and risks, a significant fiscal response, and more significant second-round effects, constitute clear upside risk to our ECB call.

{kind=link}