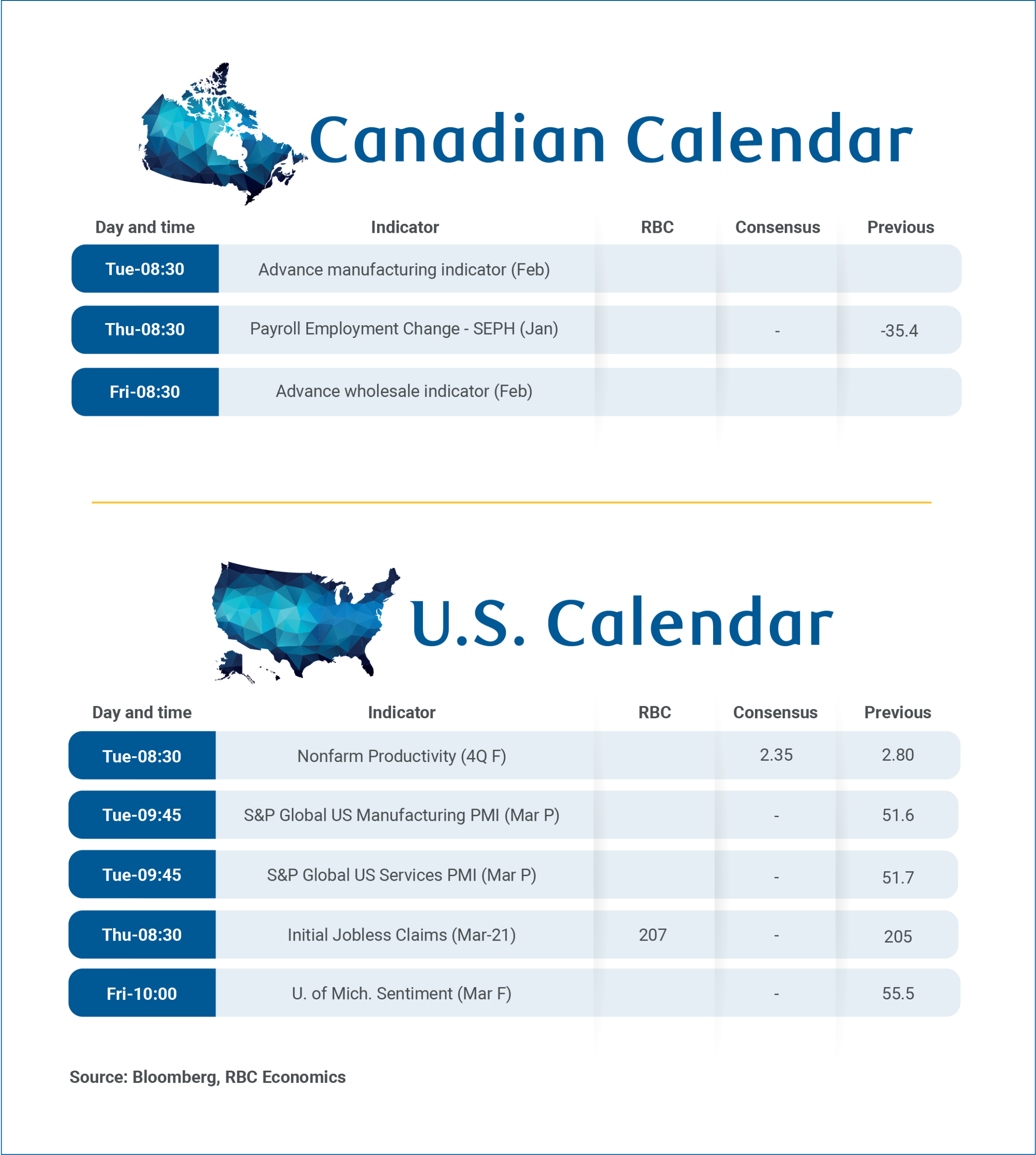

Economic data releases in Canada are quiet in the week ahead with the most notable being January’s Survey of Employment, Payrolls and Hours (SEPH) on Thursday, when we expect further stabilization in job vacancies following improvements in timelier job openings data from Indeed Hiring Lab.

February’s labour market report was weak with the unemployment rate rising to 6.7%. However, layoffs remained low and the unemployment rate was still below 7% in Q3, and 6.8% in Q4 2025.

Solid domestic demand beneath weak headline gross domestic product in Q4 2025 should continue to support a rebound in hiring early this year. We still look for the unemployment rate to gradually decline to 6.3% by the end of 2026.

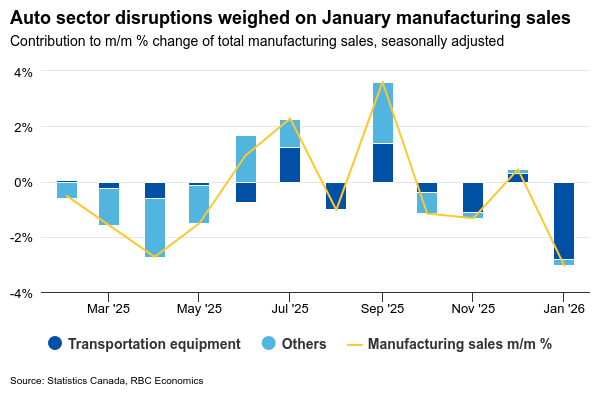

We will also receive advance February industry data that should show a partial rebound after disruptions in the auto industry drove large declines in January.

Manufacturing sales dropped 3.9% due to a significant decline in transport equipment sales from atypical production disruptions at several Ontario plants. Wholesale sales also fell 1.5% in January. Some moderation in production disruptions should support a partial rebound in February sales with manufacturing on Tuesday and wholesales on Friday.

BoC and Fed stand pat on rates

Overall, as the Bank of Canada noted in its meeting on Wednesday, the economy started Q1 on a softer footing than expected. However, with weakness in production mostly driven by disruptions in the auto sector, we expect some recovery later in the quarter.

We have left our outlook for modest growth and improved per-capita economic conditions this year broadly unchanged, and for now expects relatively neutral economic impact from recent oil price increases in both Canada and the U.S. –with the BoC and U.S. Federal Reserve remaining on hold through 2026.

At their meetings this week, both central banks held rates steady and refrained from commenting too much on the economic impact from the ongoing Middle East conflict.

In Canada, persistently weak inflation pressure prior to the oil price shock should leave the BoC with room to wait for additional clarity, compared to the U.S., where inflation pressures have been more stubborn, and tariff-related pressures are starting to show up.

on Thursday, when we expect further stabilization in job vacancies following improvements in timelier job openings data from Indeed Hiring Lab.){kind=link}