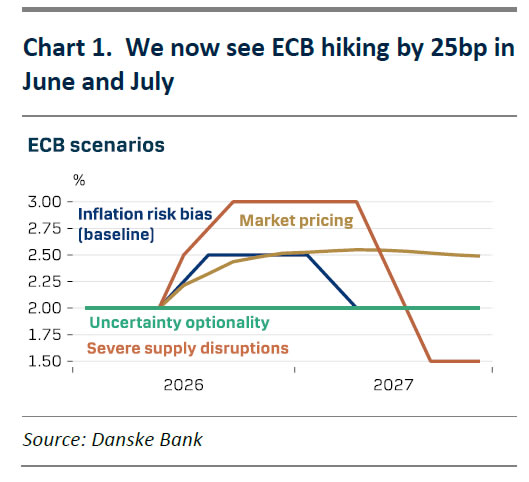

We tweak our ECB call and now expect the ECB to remain on hold at the April meeting before increasing policy rates by 25bp in each of June and July, bringing the deposit rate to 2.50% in July. Our previous call included two 25bp rate hikes in April and June. There are two main reasons for the change: 1) the ECB’s communication has shifted to a less hawkish stance; and 2) the two-week ceasefire has caused commodity prices to decline significantly over the past week.

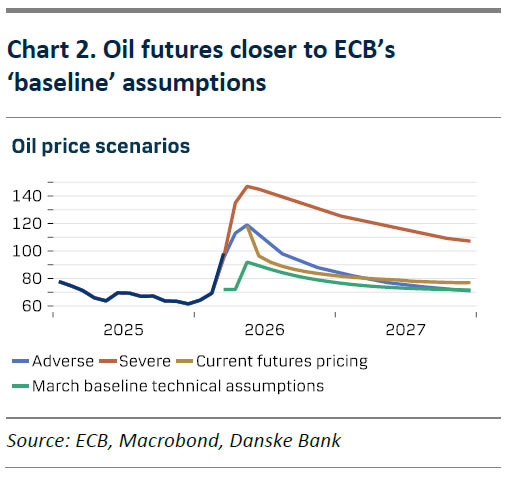

Regarding the ECB’s communication, a sources story released overnight revealed that the GC is leaning towards keeping policy rates unchanged in April as it is too early to give a verdict on the consequences of the war in Iran. The highly influential GC member Schnabel at the same time stated that ECB can afford to take time to analyse the shock and that they do not want to impose unnecessary costs on the economy. The minutes from the March ECB meeting were on the dovish side and resembled Lagarde’s calm ‘wait and see’ stance at the press conference in March. Hence, we expect the ECB is likely to use the uncertainty optionality of the situation to hold rates unchanged at the April meeting. Regarding commodity prices, the two-week ceasefire in Iran and reports of continued talks between the US and Iran have caused a drop in the spot brent oil price to around 97 USD/bbl from 110 USD/bbl last week. The futures curves remain in steep backwardation and are now closer to the ECB’s baseline staff projections’ technical assumptions (see Chart 2), while the April and May contracts were above.

We expect two 25bp hikes, in June and July, bringing the deposit rate to 2.50%

We continue to expect the ECB to hike policy rates by a total of 50bp this year due to the still relatively hawkish sentiment in the GC, but we now see the first hike in June and not April. Lagarde has stated that the ECB runs a communication risk of not hiking to higher prices, so they remain “agile”. Furthermore, we anticipate rate increases to ensure inflation expectations remain anchored. Several GC members have emphasised that inflation expectations may be more responsive to energy price rises, given that the 2022 episode remains fresh in memory. Whilst we believe the 2022 episode cannot be compared with the current situation, the GC appears to have a lower threshold for rate increases. Additionally, European governments have already begun stimulating demand, with 20 out of 27 EU member states having introduced tax cuts or price subsidies on oil products. Although the total fiscal allocation to these measures remains modest relative to the size of the eurozone economy, they demonstrate a clear bias towards non-targeted measures, which makes ECB rate hikes more probable. Given that monetary policy affects the economy with significant lags, we expect the ECB to deliver rate increases relatively quickly, in June and July, rather than later in the year.

We view the risks to our new call as tilted to the downside. We believe that the longer the ECB delays rate hikes, the more the probability of future hikes declines, as negative growth effects become more apparent and the ECB treats the shock as a “one-off”. The likelihood of the ECB looking through the energy shock entirely has therefore increased. The past month has demonstrated how quickly sentiment can shift within the GC, from being calm at the March meeting (as minutes reveal), extremely hawkish in the days after the March meeting (e.g. Nagel saying on 20 March the ECB would need an April hike if the price outlook soured), and now less hawkish again (as the sources story overnight showed). This relative shift could occur again before June, leading to no rate increases at that time, in contrast to our baseline of two hikes.

However, much of the outlook also depends on the war in the Middle East. There remains a clear risk that the ceasefire turns out to be only temporary and that energy prices will rise again as the two sides disagree on key matters, see Geopolitical Radar: Pause, Not Peace, 10 April. Furthermore, the risk of supply shortages on key refined oil products such as jet fuel is also increasing, as shipments through the Strait of Hormuz remain low. The IEA has stated that Europe has ‘maybe’ six weeks of jet fuel remaining, which could raise airfares and thus core services inflation. With the ECB staff projections’ ‘adverse’ and ‘baseline’ scenarios including approximately 35bp worth of hikes, we believe they provide the ECB with comfort in raising policy rates in June and July. Given that economic activity in the eurozone is negatively affected by the supply shock and expected rate hikes, we still anticipate the ECB lowering policy rates by 25bp in each of March and April 2027, bringing the DFR back to 2.00%.

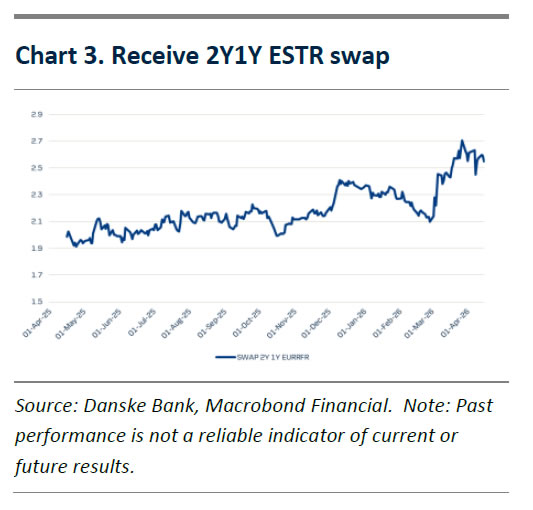

Rates Strategy: New trade – receive 2Y1Y ESTR swap

In last week’s Reading the Markets EUR (RtM EUR, 9 April), we highlighted that if the two-week ceasefire was the first step towards a lasting resolution and we saw a further drop in oil price, we would position for a move lower in short-term interest rates and would fade the April meeting pricing. Since then, it has become increasingly evident that both the US and Iranians are looking for an off-ramp in the Middle East, and that the ECB is taking a more cautious stance. As highlighted above, we have therefore pushed our call for hikes to June and July (previously April and June).

Given recent developments, we see value in receiving the 2Y1Y ESTR swap. On one hand, given the ECB’s more cautious stance, we see a possibility that the wait-and-see approach would gain traction within the GC as time passes and would increasingly favour that the ECB could see through the pick-up in headline inflation and remain on hold. Conversely, a war in the Middle East constituting a negative supply shock with elevated energy prices puts downward pressure on growth prospects. We think the narrative of worsening growth prospects due to high energy prices, which would only be further exacerbated by the outlook for monetary tightening, will gain traction in the coming months, and favour receiving the front-end of the curve. The 2Y1Y point offers a 6M roll-down of around 5bp.

Risks to the trade are more pronounced fiscal easing triggering a more forceful response from the ECB, and developments in the Middle East.

New trade: We recommend receiving the 2Y1Y ESTR swap @ 2.55% with a soft target of 2.35% and a stop-loss at 2.75%.

the ECB’s communication has shifted to a less hawkish stance; and 2) the two-week ceasefire has caused commodity prices to decline significantly over the past week.){kind=link}