- The Bank of England on hold, as widely expected.

- A scenario framework was presented and suggests rate hikes would be the appropriate response, but the governor was very careful not to pre-commit to anything.

- We think that the most likely outcome going forward is no changes, but recognise risk is tilted towards one or two hikes.

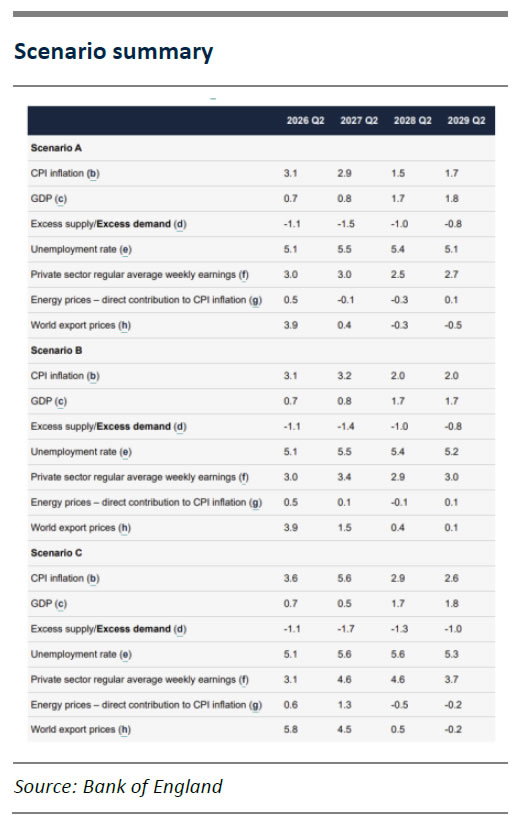

The Bank of England (BoE) kept the Bank Rate unchanged at 3.75% as expected. The decision was taken with an 8-1 vote, with Chief Economist Pill voting for a hike. The BoE presented three scenarios in their monetary policy report, of which scenario A looks outdated, because energy prices are conditioned on mid-April futures curves.

Scenario A assumes the energy shock is short lived, while scenario B and C means more persistent costs and higher inflation in particularly scenario C, see BoE: Monetary Policy Report for details. Noticeably, none of the scenarios pencil in an outright recession. Different BoE models largely put appropriate policy responses of one/two/several hikes in the three different scenarios. Governor Bailey is putting most weight on scenario B along a small majority in the MPC which could quickly find itself split in the middle again. In the press conference, Baily was very careful not to attach any probabilities or specific policy responses to the scenarios, though. He noticed, however, that he does not think market pricing is off, so no push back on that front.

He emphasized that the decision was an “active hold” and not a “wait-and-see” decision. The BoE will not wait for second round effects to react, because by then, it is too late. Over the coming weeks, they will be particularly zoomed in on food prices, which have a large energy component. Pay settlement is set in the spring and is thus not likely to compensate consumers for lost purchasing power anytime soon.

BoE call. The meeting today and the balance of the MPC-members’ individual statements did not convince us, that the BoE is on the brink of hiking rates. We think they are satisfied with the tighter financial conditions and are most likely to keep the Bank Rate at the current level, but we recognise the risk is tilted towards one or two hikes. Much hinges on the situation in the Gulf and the balance between UK activity and signs energy costs are spreading to core inflation.

Market reaction. The market responded to the decision by trading Gilt yields lower and backtracking a bit on the hawkish repricing. The June meeting is now priced close to 50-50 for a rate hike.

kept the Bank Rate unchanged at 3.75% as expected. The decision was taken with an 8-1 vote, with Chief Economist Pill voting for a hike. The BoE presented three scenarios in their monetary policy report, of which scenario A looks outdated, because energy prices are conditioned on mid-April futures curves.){kind=link}