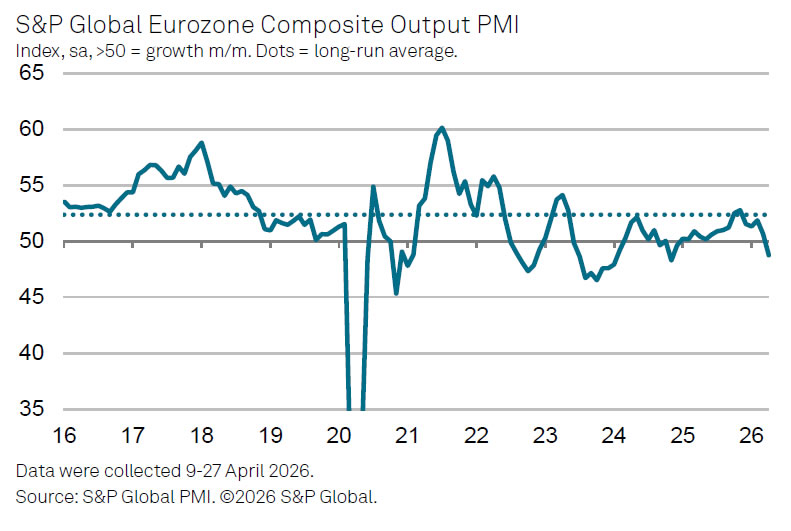

Eurozone private sector activity slipped back into contraction in April, with the Services PMI finalized at 47.6, down sharply from 50.2 in March and marking a 62-month low. Composite PMI fell from 50.7 to 48.8, its weakest reading in 17 months and the first contractionary print in nearly a year and a half. The data suggest the recovery momentum that had been building earlier this year has been derailed by escalating tensions in the Middle East.

The downturn was concentrated in services, particularly consumer-facing sectors, as surging energy costs and disruptions to travel weighed heavily on demand. According to S&P Global’s Chris Williamson, the ongoing conflict is delivering a “double whammy” to the sector through higher fuel prices and weaker mobility. Meanwhile, manufacturing has remained relatively resilient, though much of the support appears to be driven by precautionary stock building amid fears of future supply shortages and further price increases. At the same time, inflation pressures intensified significantly, with prices charged rising at the fastest pace in three years.

The weakness was broad-based across the region’s largest economies. Germany and France both recorded their sharpest declines in private sector activity in more than a year, while Spain saw its steepest downturn since August 2023. Only Italy and Ireland remained in expansion territory.

Williamson warned that the current slowdown could deepen further if the geopolitical crisis persists. He noted that rising ECB interest rate expectations are already weighing on real estate and financial services activity, while higher borrowing costs risk amplifying the broader decline in business confidence.

| Indicator | Previous | Final | Notes |

|---|---|---|---|

| PMI Services | 50.2 | 47.6 | 62-month low |

| PMI Composite | 50.7 | 48.8 | 17-month low |

{kind=link}