The Swiss National Bank delivered one of the least surprising decisions of the week, leaving its policy rate unchanged at 0% and signaling little urgency to alter its policy stance anytime soon. Despite inflation rising to 0.6% in May from 0.1% in February, the SNB made clear that it views the increase as largely an energy story rather than the start of a broader inflation problem. Policymakers emphasized that “medium-term inflationary pressure… is virtually unchanged” and described current policy settings as appropriate for maintaining price stability.

A key focus of the statement was the Swiss franc. The SNB reiterated that it has an “increased willingness to intervene in the foreign exchange market” and explicitly stated that it would act against a “rapid and excessive appreciation of the Swiss franc.” That language underscores the bank’s long-standing concern that an overly strong currency could push inflation too low and weigh on economic activity. In effect, the SNB continues to view franc strength as a greater policy challenge than inflation itself.

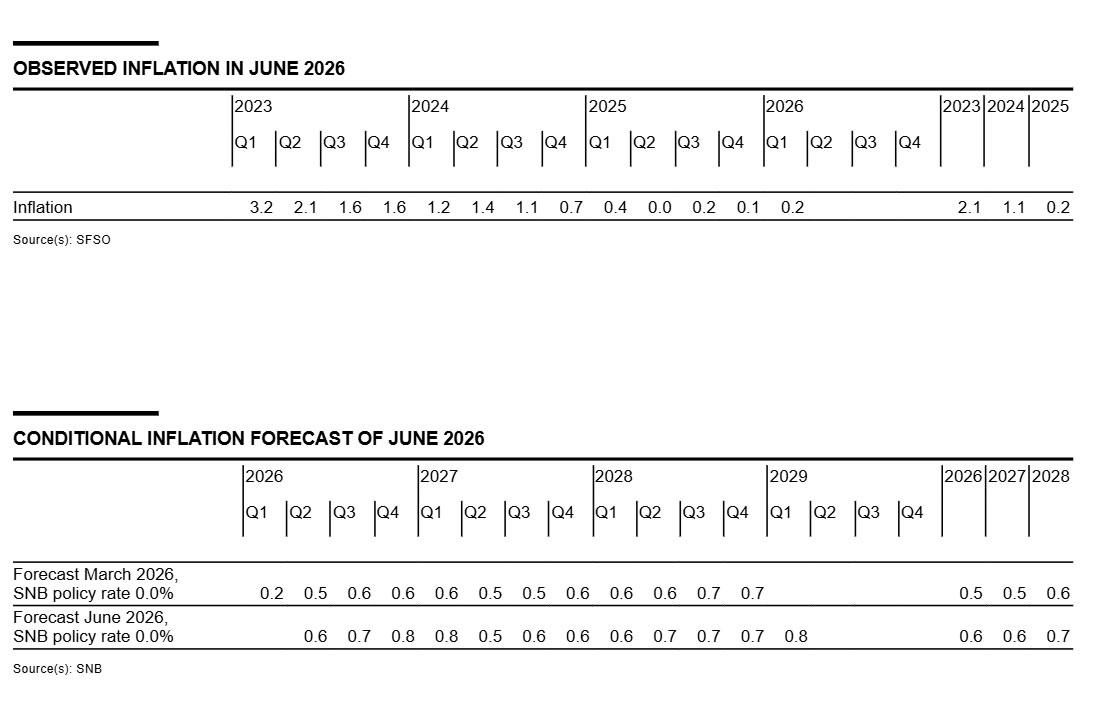

The central bank expects inflation to rise slightly in the near term before easing again as the effects of higher energy prices gradually fade. According to its latest projections, inflation will average 0.6% in both 2026 and 2027 before edging up to 0.7% in 2028. Importantly, the bank stressed that inflation remains within its definition of price stability across the entire forecast horizon, reinforcing expectations that rates can stay at 0% for an extended period.

The statement also highlighted significant uncertainty surrounding the global outlook, particularly developments in the Middle East and commodity markets. Nevertheless, the SNB described the Swiss economy as resilient, even though unemployment has risen somewhat in recent months. For markets, the takeaway is straightforward: unlike some major central banks that are increasingly worried about inflation becoming entrenched, the SNB still sees the current inflation pickup as temporary and remains prepared to use foreign exchange intervention if franc appreciation becomes excessive.

{kind=link}