Our summary of recent economic events and what to expect in the weeks ahead.

Canadian Highlights

- Canadian inflation accelerated in May, driven primarily by higher gasoline prices, while the Bank’s preferred core measures remained close to 2%.

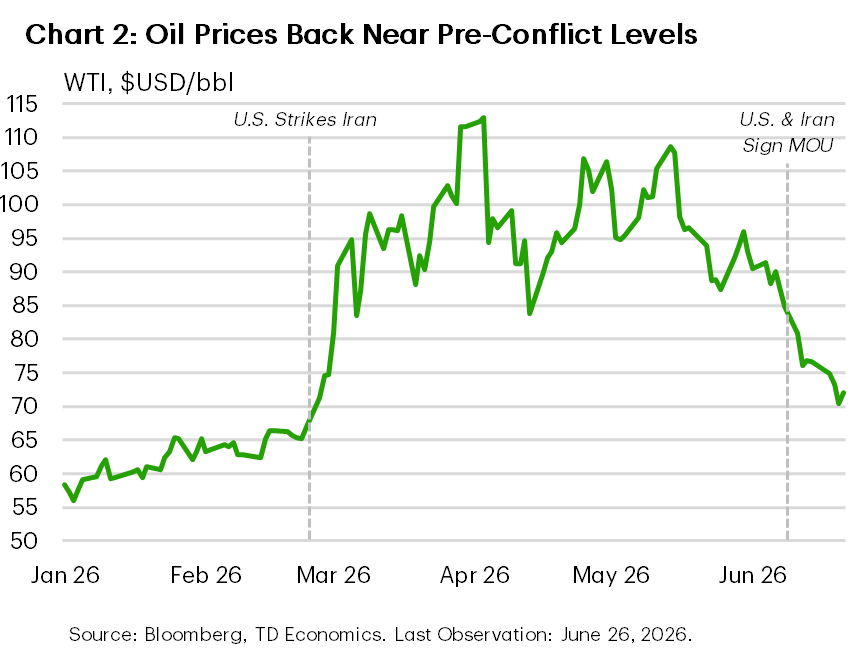

- WTI crude has largely unwound its recent geopolitical premium, retreating to around $70 per barrel. If sustained, this will pull headline inflation lower over the coming months.

- Attention now turns to next week’s industry GDP release. We expect a rebound in April, which would be in line with GDP growth to resume at 1.9% annualized pace in the second quarter.

U.S. Highlights

- Oil prices fell below $70/barrel, flirting with pre-conflict levels as the U.S. and Iran continue to negotiate towards a permanent resolution.

- The Federal Reserve’s preferred inflation metric, core PCE, rose 3.4% year-over-year in May.

- Personal income and spending both rebounded in price-adjusted terms in May, though households have increasingly relied on savings to support spending.

Canada – Peak Inflation

This week’s inflation data reinforced a familiar message: the recent inflation gain remains largely energy-driven, while underlying price pressures have remained contained and continue to ease. May’s CPI print showed headline inflation re-accelerating to 3.2% year-on-year (y/y) from 2.8% in April, driven primarily by higher gasoline prices. Prices at the pump rose for a third consecutive month, accelerating to 33.2% y/y and reaching their highest levels since June 2022. Air transportation prices also increased as airlines faced higher operating costs, particularly for jet fuel. Another notable outlier was tomato prices, which surged 45.2% y/y, reflecting reduced Mexican supply due to poor weather conditions and a reduction in planted acreage following the implementation of U.S. tariffs.

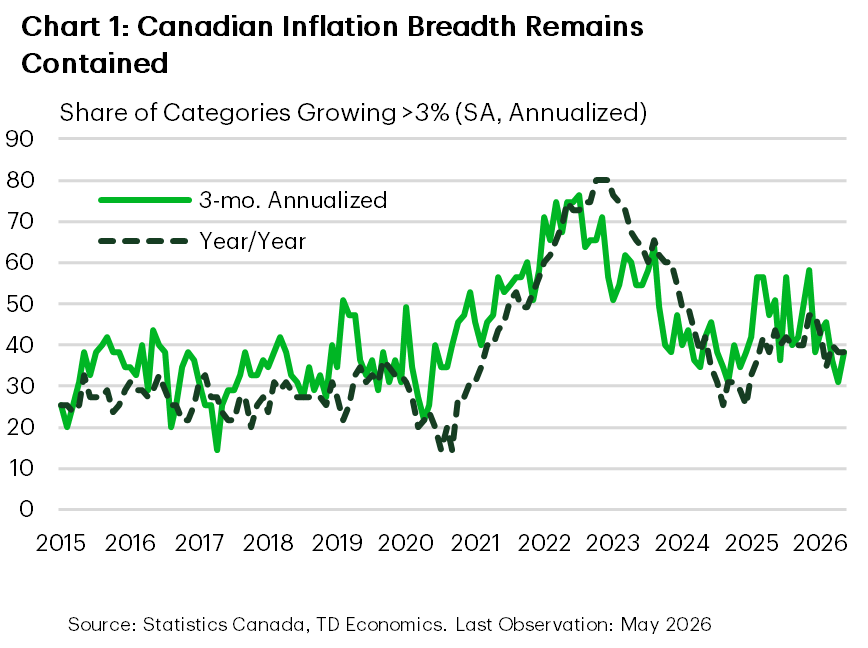

In contrast, the Bank of Canada’s preferred core measures remained close to 2%. While they edged slightly higher on a three-month basis, the increase was modest and not enough to raise alarm bells. The contained pace of core inflation underscores that the recent energy price spike has remained concentrated in a few categories. Inflation breadth – a measure of how broadly price increases are spread across the economy – remained contained. Outside of energy price pressures, prices are broadly consistent with an economy operating below potential.

Meanwhile, oil prices have begun to retreat, suggesting that this energy-driven inflation flare-up has peaked. WTI crude has largely unwound its recent geopolitical premium, retreating to around $70 per barrel – close to its pre-conflict level. The decline reflects expectations that oil flows through the Strait of Hormuz will normalize relatively quickly, easing concerns over oil supply disruptions. If those expectations prove correct, lower energy prices will pull headline inflation lower.

Core inflation, however, is likely to remain somewhat elevated for another two to three months, reflecting the typical lag for energy costs to feed through to the broader economy. What’s important is that the trend in core inflation is broadly consistent with what the Bank of Canada would like to see. Governor Macklem reiterated this point following his speech in Paris, noting that inflation remains concentrated rather than broad-based, while the Bank’s preferred core measures have shown little movement.

Attention now turns to next week’s April industry GDP release. Recall that first-quarter expenditure-based real GDP contracted by 0.1% annualized, weighed down by volatile trade flows and weak domestic demand. The underlying picture, however, was more constructive. Industry-based GDP grew by 0.5% annualized over the quarter, suggesting that the headline contraction might have overstated the degree of underlying weakness. Statistics Canada’s flash estimate points to a solid 0.4% month-on-month gain in April, positioning the economy for a stronger start to the second quarter.

This aligns with our broader assessment that the economy is going through a soft patch rather than sliding into recession. We expect growth to resume at 1.9% quarter-on-quarter (annualized) in Q2 2026.

Maria Solovieva, CFA, Economist

U.S. – Oil Prices Retreat as AI Volatility Picks Up

The first week of summer was relatively quiet on the economic data front, with financial markets consumed by developments in the Middle East and evolving trends in AI. The latter proved to be a source of volatility in equity markets this week, as news of personnel changes at Alphabet led to a sell-off that spread to the broader AI ecosystem. This was partially reversed later in the week, but still highlights the inherent sensitivity of markets under the combined influence of elevated valuations and market concentration. The S&P 500 was down 1.8% while U.S. Treasury yields moved modestly lower on the week as of the time of writing.

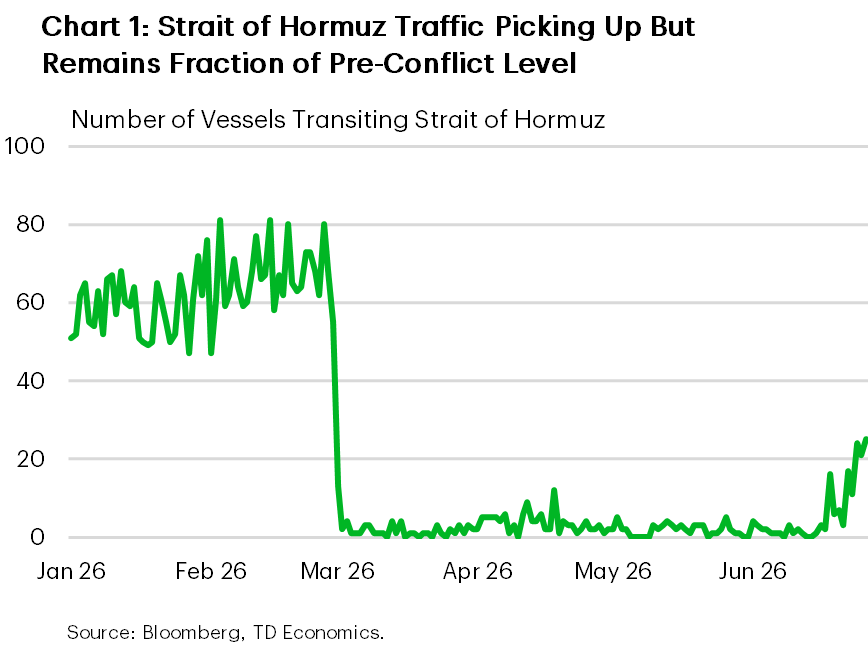

On the geopolitical front, negotiations between the U.S. and Iran continued after the two sides signed a 60-day memorandum of understanding (MOU) last week. The cessation of hostilities and reopening of the Strait of Hormuz have been enthusiastically welcomed by financial markets, with oil prices now back at their pre-conflict level. However, it bears repeating that the resumption of oil trade through the vital passageway is likely to be a gradual process as evidenced by the current level of maritime traffic through the strait. Combined with the possibility for roadblocks to be encountered during negotiations, risks related to oil prices remain skewed to the upside.

The feedthrough of higher energy prices to the economy was evident in the PCE inflation reading for May. Prices were 4.1% higher year-on-year (y/y) during the month, primarily driven by a 24% increase in energy prices. However, broader inflation pressures were also present, with core PCE inflation, which excludes food and energy products, rising 3.4% y/y. With energy prices having sharply reversed, some downward pressure on overall inflation is already in-tow. However, uncertainty around the magnitude and duration of energy-related second-order effects has given policymakers reason to adopt a more hawkish stance.

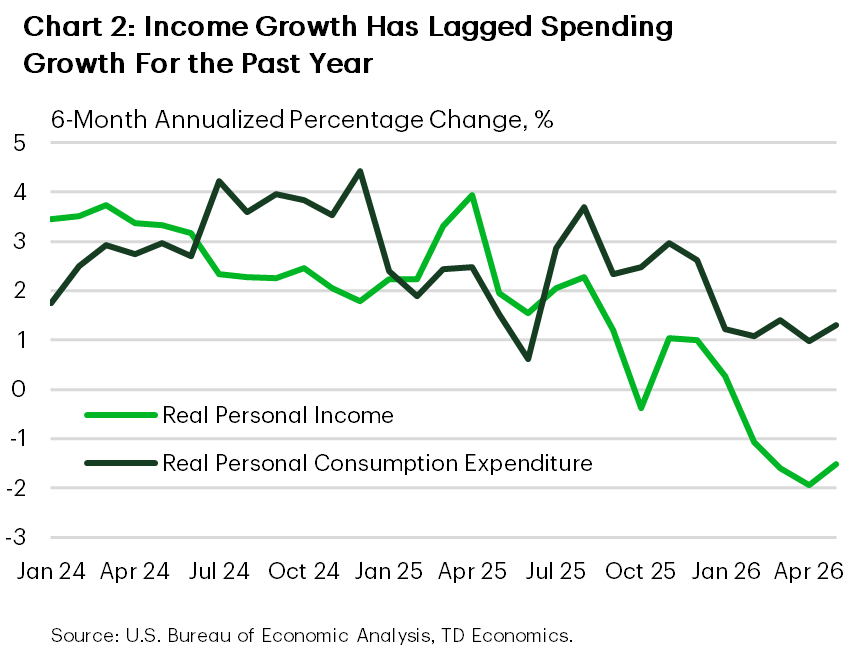

Personal income and spending both rebounded in real (price-adjusted) terms in May after softer readings in April, reflecting the sustained resilience of the American consumer. Still, much of the spending in recent months has been driven by a drawdown in savings, with the savings rate remaining at 3% in May – far below its historical average of 5-6%. While robust financial returns over the past few years may be offsetting the extent to which consumers need to save to meet their financial goals, the downward trend in the savings rate also began in mid-2025, coinciding with the introduction of broad tariffs and likely reflective of the multitude of cost pressures that have weighed on consumers over the past year.

Looking ahead to next week, the June employment data release on Thursday will be the highlight. Markets currently expect 118k new jobs to have been created during the month, marking a moderate deceleration relative to the strong reading in May. Fed Chair Warsh will also participate in a panel discussion next Wednesday, which will be watched closely for any signals on monetary policy decisions over the second half of the year.

{kind=link}