Our summary of recent economic events and what to expect in the weeks ahead.

Canadian Highlights

- The July 1st CUSMA extension deadline came and went, but this outcome was well telegraphed and the status quo, in terms of U.S. tariffs on Canada, remains.

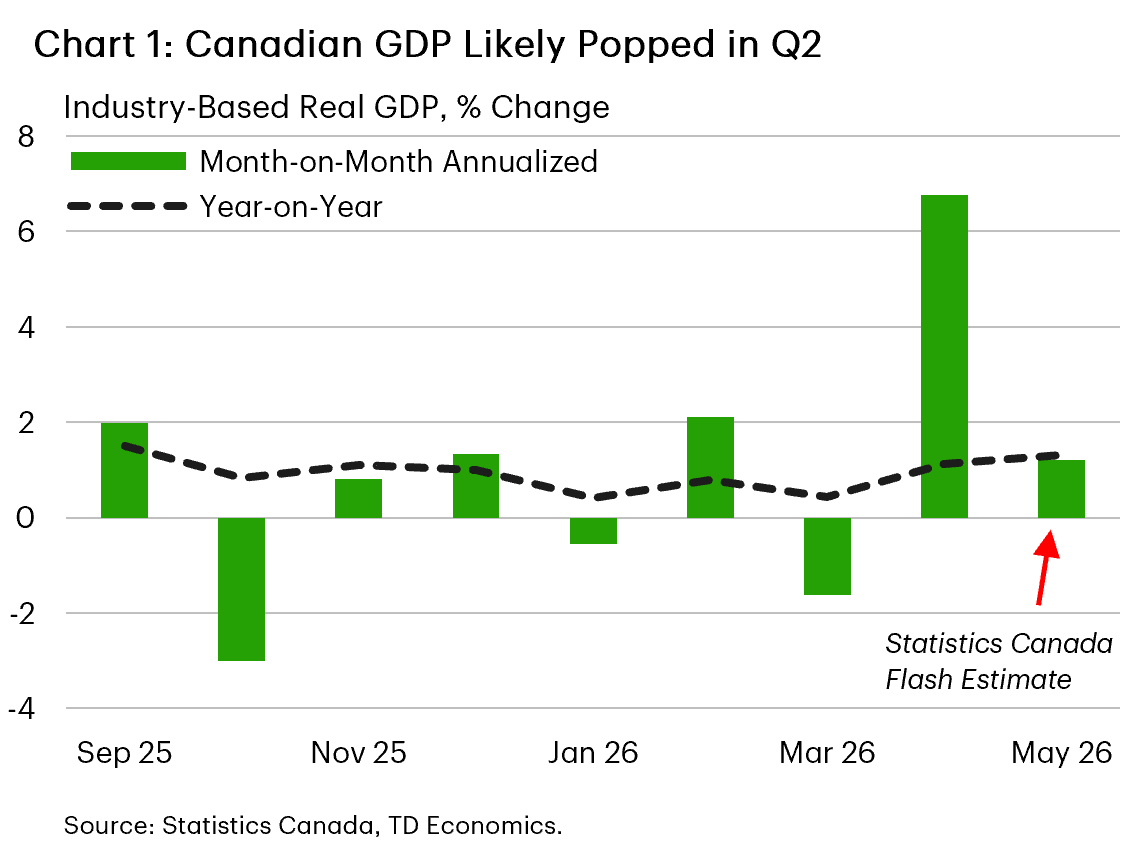

- Canada’s economy popped in April and likely grew again in May. This puts Q2 growth on track to print above 2% annualized, easing recession concerns.

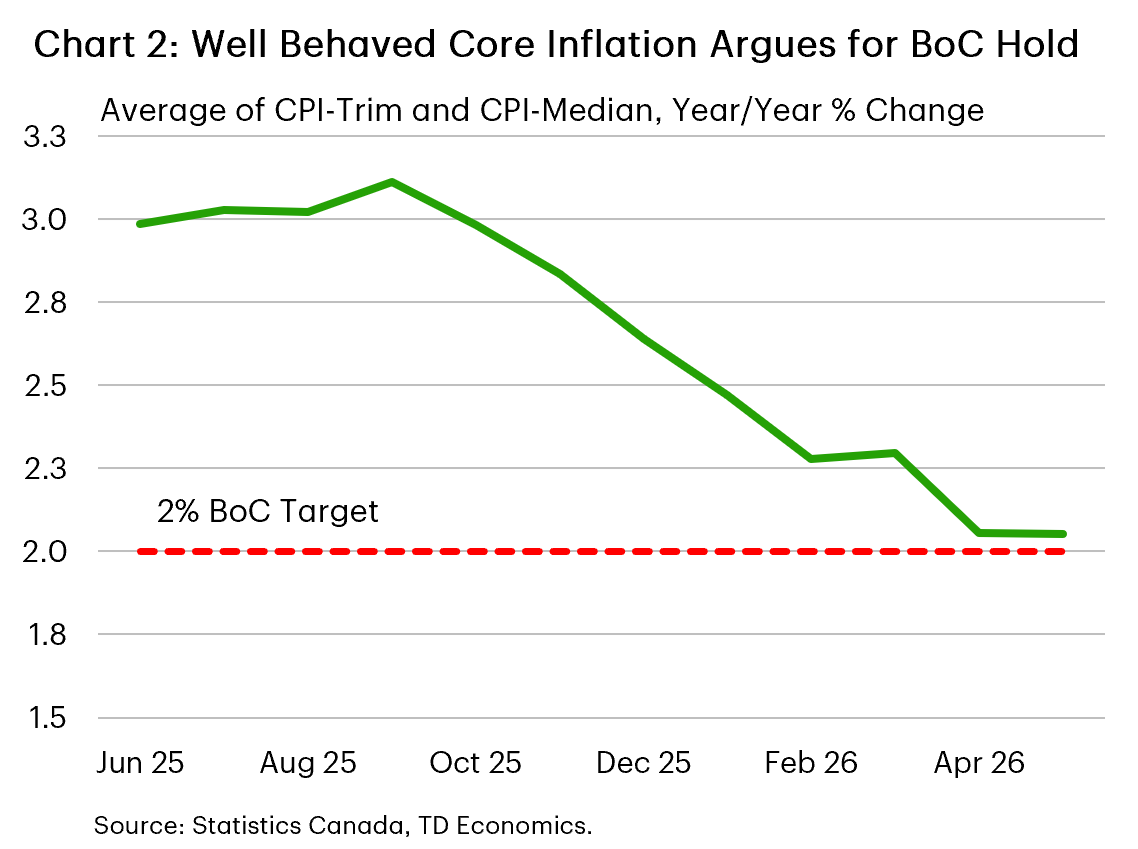

- Lower oil prices should help near-term inflation, while underlying slack and contained core inflation pressures strengthen the case for a Bank of Canada hold stance.

U.S. Highlights

- U.S. equities had a stellar first half performance this year, with the S&P 500 and NASDAQ rising 9.5% and 13%, respectively.

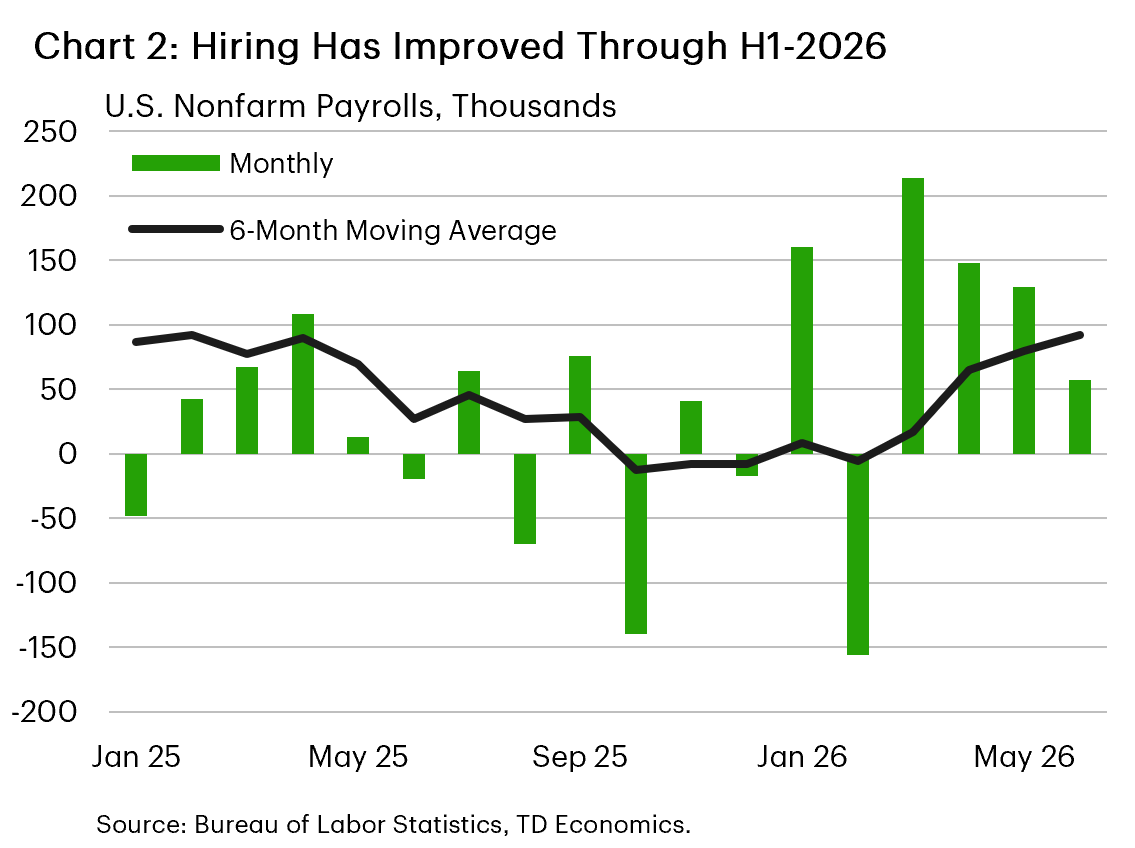

- Nonfarm employment moderated in June, but underlying hiring trends remain reasonably solid. The unemployment rate dipped to a twelve-month low of 4.2%.

- The ISM Manufacturing Index remained in expansionary territory for the sixth month in June, while vehicle sales hit a nine-month high of 16.5 million.

Canada – GDP Fireworks Ahead of Canada Day

In this holiday shortened week, there were still some notable moves in financial markets. Oil slid lower and, more broadly, has plunged since early June on hopes of a U.S.-Iran peace deal and improved traffic through the Strait of Hormuz. Canadian bond yields climbed during the week but eased back a bit today, driven by dynamics in the U.S. For its part, the Canadian dollar was unchanged at about 70 cents U.S. but has been tumbling since early May, pressured by hawkish U.S. central bank messaging.

The recent slide in oil prices is certainly a welcome development from an inflation perspective and will be reflected in June’s CPI print. However, there could still be some upside to oil prices after this initial downswing. Global inventory buffers were steadily drawn down during the conflict and the summer driving season is set to ramp up.

Nonetheless, our forecast assumes that oil prices are past their peak. The Bank of Canada will breathe a sigh of relief if that turns out to be true, although policymakers were treated to some fireworks ahead of the Canada Day holiday, courtesy of a well-timed surge in monthly GDP. Indeed, Canadian GDP shook off some winter blues, popping by 0.5% month-on-month in April. This should help quell recession chatter, with April’s gain marking the largest such increase since July 2025.

On the less-positive side, the July 1st deadline to extend the CUSMA agreement for another 16 years came and went this week. However, this outcome was telegraphed well ahead of time by Canada, U.S. and Mexico. For now, the status quo remains, with most of Canada’s exports to the U.S. tariff-free, but with punishing levies on sectors such as steel, aluminum and autos still in place. The process now moves to annual reviews (which will keep the cloud of uncertainty hanging), although parties can strike a deal at any time. We have tentative evidence that the worst of the trade conflict may be in the rearview. For instance, manufacturing GDP has risen in two of the last three months through April, and may have increased again in May given a pickup in hiring.

Incorporating StatCan’s GDP guidance for May, Canada’s economy is now on track to grow at a pace above 2% annualized in the second quarter. This is stronger than what the Bank of Canada expected in its April projection. Even still, it doesn’t materially change our view on rates. Remember that the bounce back in GDP comes on the heels of several quarters of soft activity, meaning that the economy is still likely in excess supply. Core inflation remains well behaved, with economic slack likely to apply downward pressure. Next week brings a slew of important data, including the Bank of Canada’s Business Outlook Survey (BOS) and the June read on the job market. The prior BOS offered evidence that businesses are adjusting to the trade war, while Canadian hiring surged in May (raising the risk of some giveback in next week’s report). We’ll be monitoring these closely, but it would take some surprises to shake us from the view the Bank will remain on hold this year.

Rishi Sondhi, Economist

U.S. – Celebrating America’s Exceptionalism

This weekend will mark America’s 250th anniversary, but for financial markets, this holiday shortened week also brought a brief halftime for calendar 2026. It’s been an eventful first six months of the year, marked by a flurry of trade deals, further shifts in tariff policies, a new chapter for the Federal Reserve and plenty of geopolitical tensions. Through it all, financial markets have remained remarkably calm. The S&P 500 rose 9.5% through the first half of the year while the NASDAQ was up nearly 13% – or more than double last year’s mid-year performance. It remains to be seen whether the run is something to cheer or fear, but one thing is for certain, the AI buildup and the expected productivity enhancements that it could eventually deliver have been pivotal catalysts underpinning the bull rally.

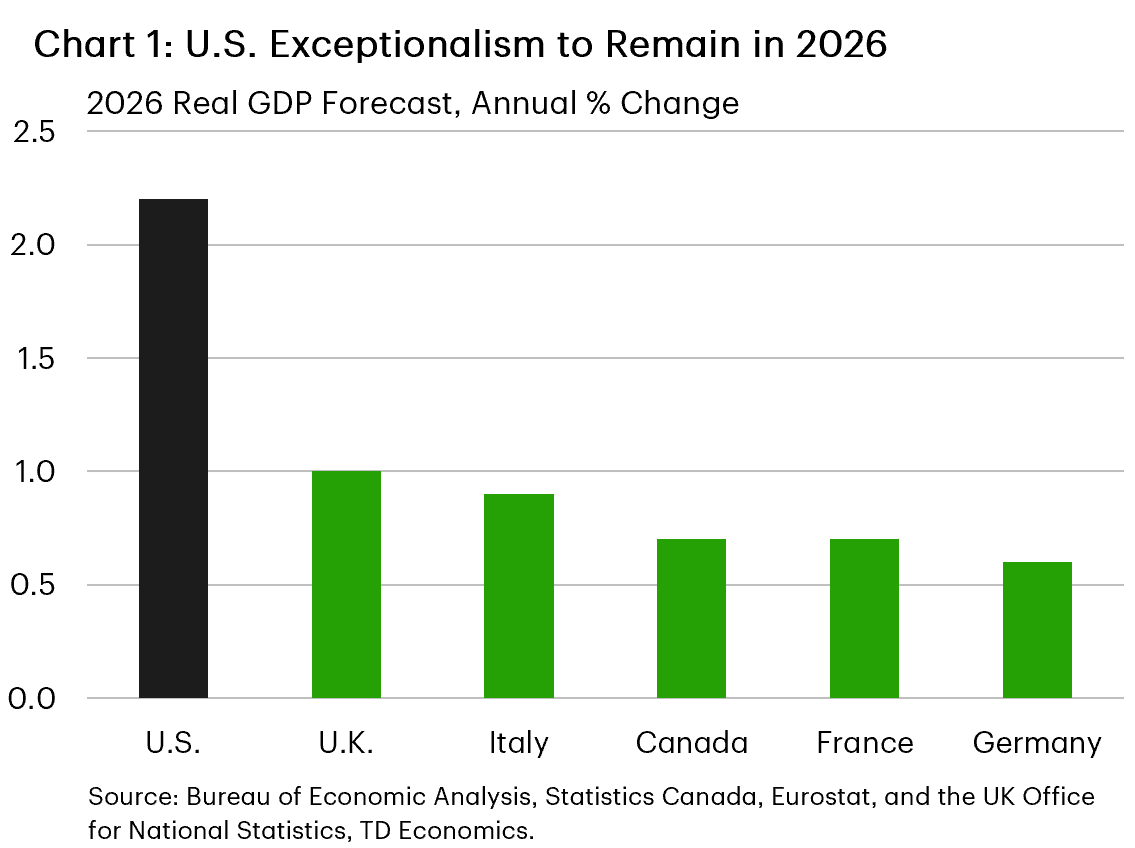

Beyond the AI push, a return to the American exceptionalism trade has also offered a tailwind for equities. U.S. growth is tracking north of 2% for 2026, or a multiple of any of the other G7 nations. And perhaps more encouragingly, the balance of risks for the U.S. outlook feels tilted to the upside. The U.S.-Iran peace deal has quickly returned energy prices to pre-conflict levels, dragging gas prices lower. This is good news for the consumer. At the same time, the labor market has clearly turned a corner after grinding through a soft patch last year. Nonfarm payrolls rose by 57k in June, a moderation from prior months, but a decent print nonetheless. Smoothing through the volatility, hiring has averaged 111k and 92k over the last three and six months, respectively. This is well above the breakeven rate, which helped to push the unemployment rate to a twelve-month low of 4.2%. But it wasn’t all good news, a sharp drop in the labor force was entirely driven by a decline of over 800k prime working age individuals (i.e., 25 to 54 years old). It’s too early to know what drove the decline or whether it’s simply related to volatility. But the magnitude is noteworthy and something worth monitoring in the months ahead.

Other data out this week also reinforced America’s economic resilience. June vehicle sales rose to a nine-month high of 16.5M, while the ISM Manufacturing Index remained in expansionary territory for the sixth consecutive month. Importantly, both production and new orders continue to expand at decent clips. And while input prices remain elevated, the sub-index fell to a four-month low, suggesting the worst of the cost pressures stemming from the energy shock are now in the rearview mirror.

This is good news for Fed officials, who are hunting for any signs of slowing price pressures amid continued concerns of elevated inflation. In his first public appearance since the June press conference, Chair Warsh underscored the Fed’s commitment to return price stability, but stopped short of giving any forward guidance. While this leaves the impression that every meeting is “live” we would argue that the data released since the last FOMC meeting alongside the sharp pullback in energy prices reduces the odds of the Fed hiking rates this summer.

{kind=link}