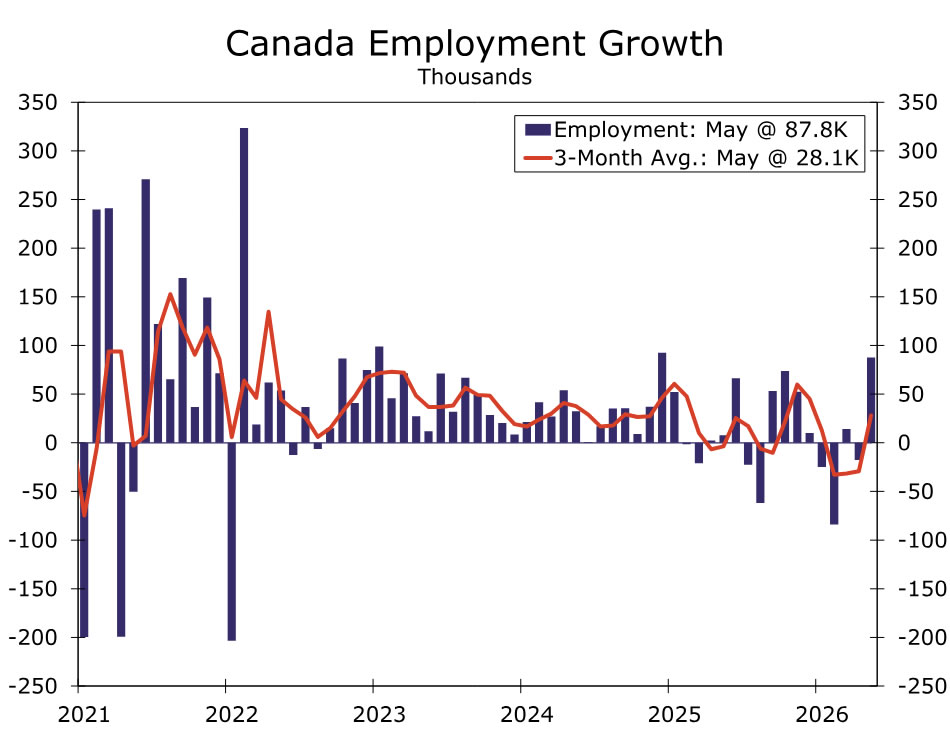

Next week’s release of the June FOMC meeting minutes should provide further insight into what could shift a divided Committee toward additional tightening, although we continue to expect the Fed to remain on hold as recent inflation strength appears largely driven by fading supply-side factors rather than overheating demand. Abroad, Japan’s labor cash earnings data will be closely watched for signs that wage growth remains consistent with the Bank of Japan’s policy normalization path. In Canada, we expect labor market conditions to remain broadly stable despite some moderation in hiring after May’s strong employment gain, supporting a patient approach from the Bank of Canada. In emerging markets, Mexico’s June CPI report should show further progress on disinflation, but persistent services inflation is likely to keep Banxico on hold.

United States:

- FOMC Meeting Minutes (Wednesday)

G10 Economies:

- Japan Labor Cash Earnings (Tuesday), Canada Labor Force Survey (Friday)

Emerging Markets:

- Mexico CPI (Thursday)

U.S. Week Ahead

FOMC Meeting Minutes — Wednesday

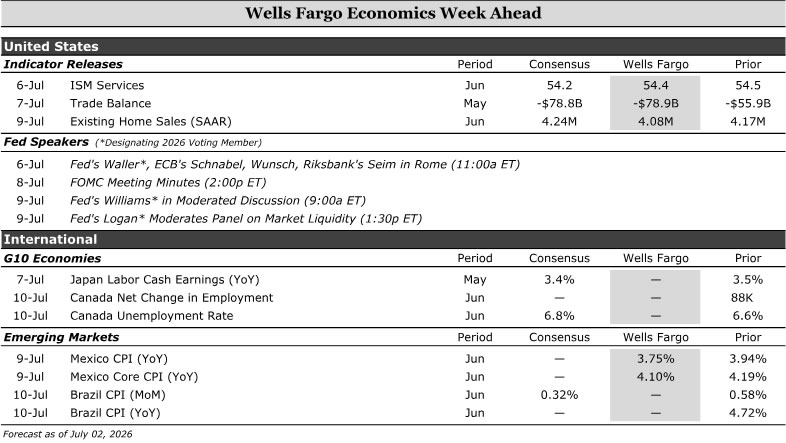

We will look to next week’s FOMC minutes for any signs of what could shift a divided Committee from a hold toward rate hikes. The dot plot from the last meeting made clear that policymakers are split on whether rate hikes are warranted, but with forward guidance getting tamped down under Chair Warsh, the Fed’s reaction function remains uncertain in terms of what exactly would build broader support for more restrictive policy.

We will be looking to whether a majority of participants view the recent pickup in inflation as persistent enough to warrant additional tightening or as primarily a temporary supply-shock. We will also be interested to see the extent to which Committee members view the labor market/the demand side of the economy as an inflationary problem.

While the minutes may lean hawkish, we continue to view recent inflation strength as being driven largely by supply side factors, including tariffs and energy, that should fade over time. Since the June meeting, oil prices have fallen further, which should help ease concerns that energy-related inflation will broaden further. And the June employment report showed no signs that the labor market is overheating or contributing to broader inflationary pressures. We thus continue to expect the FOMC to keep the funds rate on hold for the foreseeable future.

G10 Week Ahead

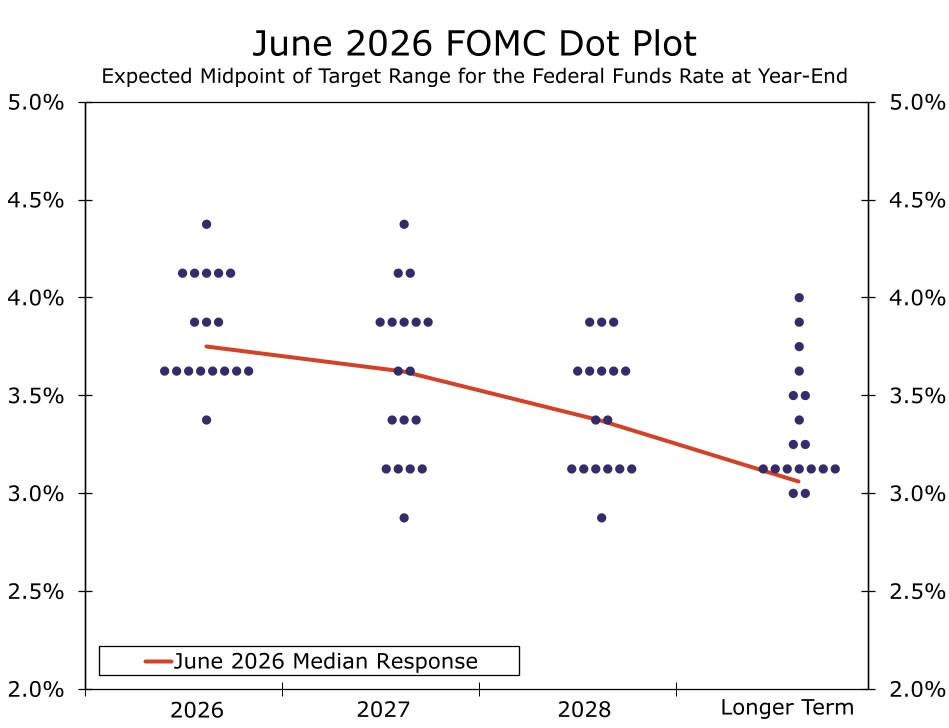

Japan Labor Cash Earnings — Tuesday

With Japan’s labor cash earnings for May due next week, the release will offer a fresh read on whether the wage-price cycle remains intact. The Bank of Japan (BoJ) continues to signal conviction in its path toward policy normalization, as April labor cash earnings and ordinary time earnings (the BoJ’s preferred gauge of underlying wage momentum) rose 3.6% and 3.3% year over year, respectively. This year’s Shunto negotiations delivered another round of strong pay gains, with labor unions securing average wage increases of more than 5% for a third consecutive year, effective from April. Given the limited coverage of union workers and the lagged pass-through from negotiated settlements to realized earnings, wage growth should remain supported in the months ahead. Lower oil prices could also help ease margin pressure for smaller firms, supporting a broader pass-through of negotiated wage increases.

While inflation has been soft, the fading of government subsidies and impact of a weaker yen on import prices should contribute to a gradual pickup in inflation. Combined with resilient GDP growth and a solid Q2 Tankan report, a strong wage print would support the case for further tightening. As such, we continue to expect the BoJ to deliver a 25 bps rate hike in Q3 (most likely September), bringing the policy rate to a terminal level of 1.25% by year-end.

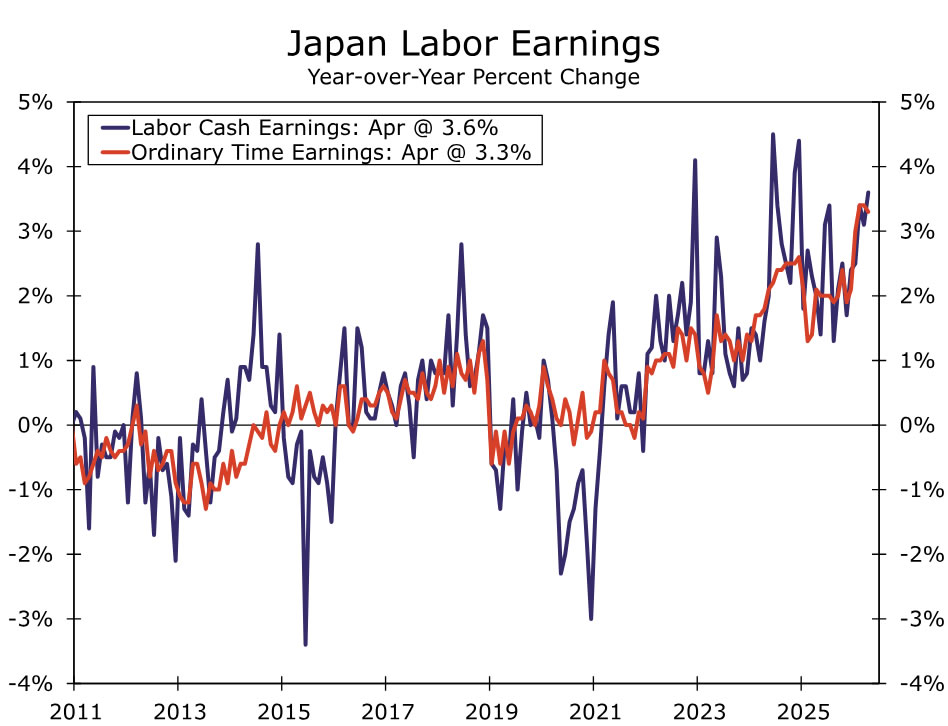

Canada Labor Force Survey — Friday

Canada’s labor market remains soft, though weakness earlier in the year was met with a sharp rebound in May. Even so, employment is up less than 1% from a year ago, underscoring the sluggish pace of hiring beneath the month-to-month volatility. While demand has softened, recent gains having been concentrated in full-time positions, rather than part-time work, is a sign of stability.

Labor supply constraints are also easing only gradually. An aging workforce and slower immigration flows should continue to limit labor force growth, helping keep a lid on any significant increase in unemployment. As a result, we expect the jobless rate to remain broadly within the 6.5–7.1% range that has prevailed over the past 12–18 months.

Following the strongest monthly employment gain since late 2024, some payback in June would not be surprising. Still, our broader assessment is that labor market conditions are stabilizing rather than deteriorating. Wage growth remains positive but is no longer accelerating materially, consistent with labor demand that has softened enough to reduce inflation pressures but not enough to raise meaningful recession concerns. Taken together, the labor market argues for continued patience from the Bank of Canada, keeping policy on hold for the foreseeable future.

EM Week Ahead

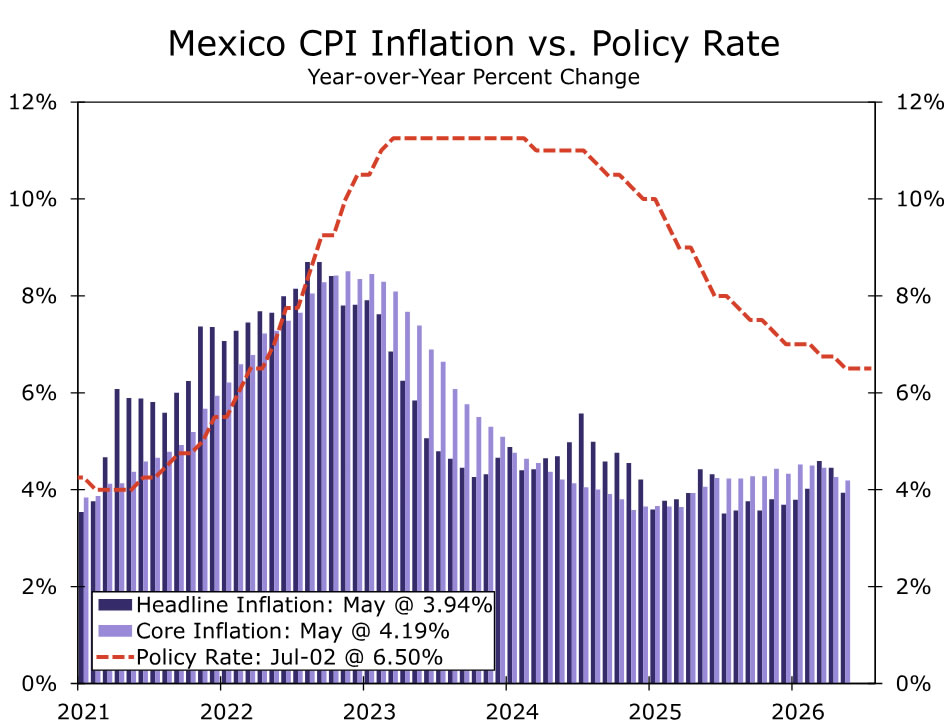

Mexico CPI — Thursday

Mexico’s June CPI release next week should provide more clarity on whether disinflation is broadening enough to reopen the door to rate cuts. Based on the mid-month data, we expect headline and core inflation to slow to 3.75% year over year and 4.10%, respectively, from 3.94% and 4.19% in May. Still, core services inflation remains sticky, which should keep Banxico cautious.

At its June meeting, Banxico’s Governing Board unanimously held the Overnight Rate at 6.50% and suggested that the current policy setting remains appropriate for an extended period. Policymakers also revised their Q2-2026 headline inflation forecast slightly lower, while the core forecast moved slightly higher.

Our base case remains for Banxico to stay on hold through year-end and into 2027. That said, risks are tilted toward a cut rather than a hike. Banxico expects growth to rebound in Q2 after contracting in Q1, then expand at a steady pace. If activity instead continues to struggle and disinflation broadens further, a rate cut could come by year-end.

{kind=link}