Two important messages delivered at the ECB meetings are: 1) the end of the front-loading of PEPP asset purchases and 2) acknowledgement of a more persistent inflation pressure. The policy rates were all kept unchanged with the main refi rate, the marginal lending rate and the deposit rate staying at 0%, 0.25% and -0.5% respectively. The central bank also upgraded the economic growth and inflation projections at today’s meeting.

Rather than committing to purchase assets under the pandemic emergency purchase program (PEPP) “at a significantly higher pace than during the first months of the year”, policymakers in September judged that “favorable financing conditions can be maintained with a moderately lower pace of net asset purchases under the PEPP than in the previous two quarters”. President Christine Lagarde stressed that it “isn’t tapering” and warned that the Eurozone is “not out of the woods”. While the amount of monthly purchases remains uncertain, we expect this to lie around 70B euro, compared to above 80B over the past few months.

On the economic developments, Lagarde reiterated that risks for the economic outlook were “broadly balanced” and “price pressures are building only slowly”. She added that “there remains some way to go before the damage done to the economy by the pandemic is undone”. While retaining the view that recent strong inflation has been driven by temporary factors, the central bank also acknowledged that “underlying inflation pressures have edged up” and that the pressures should “rise over the medium term”. It also anticipated that “price pressures could be more persistent” amidst prolonged supply chain disruption. We believe the ECB has become more concerned about the persistence of inflationary pressure.

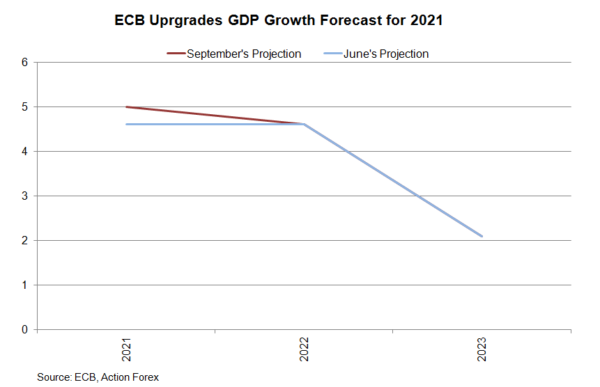

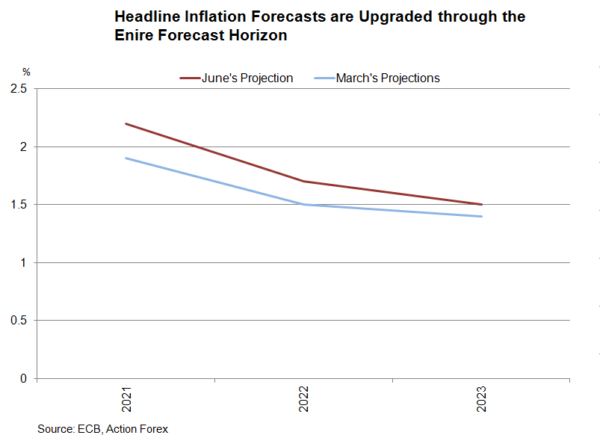

The central bank upgraded GDP growth forecast to +5% y/y from this year, while keeping projections broadly unchanged for 2022 and 2023. Inflation forecasts were upgraded across the forecast horizon.

There are a few implications of the two changes made at today’s meeting. First, the ECB will gradually buy few assets via the PEPP. Yet, this is not the same tapering as adopted by the Fed. The ECB is paving for the way for a transition from the PEPP to APP, as we mentioned in our preview. As such, ECB’s balance sheet could continue to increase after the PEEP is ended. Second, as the ECB has acknowledged that inflationary pressures are more persistent than previously expected, the decision of asset purchase would not only depend on financing conditions but also on the inflation outlook.

There are a few implications of the two changes made at today’s meeting. First, the ECB will gradually buy few assets via the PEPP. Yet, this is not the same tapering as adopted by the Fed. The ECB is paving for the way for a transition from the PEPP to APP, as we mentioned in our preview. As such, ECB’s balance sheet could continue to increase after the PEEP is ended. Second, as the ECB has acknowledged that inflationary pressures are more persistent than previously expected, the decision of asset purchase would not only depend on financing conditions but also on the inflation outlook.

{kind=link}