Dollar weakens again in early US session after mixed job data, but selling pressure is so far limited. Markets are cautiously awaiting tomorrow’s non-farm payroll report for sure. But more importantly, the development in trade relationship with Canada and China is the focal point. Canadian Foreign Affairs Minister Chrystia Freeland will have another day of meeting with US Trade Representative Robert Lighthizer. Meanwhile, Trump is ready to fire another shot at China once the hearing on the tariffs on USD 200B in Chinese goods ends today.

Euro and commodity currencies are generally weak follow Dollar. Meanwhile, Swiss Franc, Sterling, and Yen are the strongest ones. But the picture could easily be changed should there be any break through in US-Canada trade talks, or any new developments in US-China trade war. And, it should be noted again that Dollar surges almost every time there is an escalation in trade tensions.

In other markets, European stocks stabilized from yesterday’s steep selloff and turned mixed. FTSE is down -0.21% at the time of writing, DAX up 0.12%, CAC up 0.27%. 10 year German bund yield drops -0.008 to 0.337. 10 year Italian yield also dropped -0.087 to 2.862.

Earlier today, Asian markets continued to be the bigger victims in current concerns over emerging market crisis. Nikkei was down -0.41%, Hong Kong HSI was down -0.99%. China Shanghai SSE was down -0.47% at 2691.59, below 2700 handle. Singapore Strait Times dropped -0.27%. Gold rides on Dollar’s weakness and is back at 1205. Focus is on 1209 minor resistance for indicating resumption of rise fro 1160.36.

US initial jobless claims dropped to 203k, another lowest since 1969

US initial jobless claims dropped -10k to 203k in the week ended September 1, well below expectation of 214k. Also, that’s another lowest level since 1969 scored. And it’s indeed just 1k above that 202k in the week of December 6 that year. Four-week moving average of initial claims dropped -2.75k to 209.5k, lowest since December 6 1969 too (204.5k).

Continuing claims dropped -3k to 1.707m in the week ended August 25. Four-week moving average of continuing claims dropped 013.25k to 1.7185m, lowest since December 8 1973.

US ADP employment missed expectation, but job markets remains incredibly dynamic

ADP report showed 163k growth in private sector jobs in August, below expectation of 188k. Ahu Yildirmaz, vice president and co-head of the ADP Research Institute said in the release that “although we saw a small slowdown in job growth the market remains incredibly dynamic”. And, “midsized businesses continue to be the engine of growth, adding nearly 70 percent of all jobs this month, and remain resiliant in the current economic climate.”

Also, Mark Zandi, chief economist of Moody’s Analytics, said, “The job market is hot. Employers are aggressively competing to hold onto their existing workers and to find new ones. Small businesses are struggling the most in this competition, as they increasingly can’t fill open positions.”

Also released, US nonfarm productivity was finalized at 2.9% in Q2, unit labor cost at -1.0%. Canada building permits dropped -0.1% mom in July.

Next phase of US-China trade war ready, as public comments end today

It’s still a bit early, but the next phase of US-China trade war is approaching. The public comment period for the 25% tariffs on USD 200B in Chinese imports will end today. Trump could be ready to start imposition of such tariffs any time. And ahead of that Trump said yesterday that “right now we just can’t make that deal” with China. And, “in the meantime, we’re taking in billions of dollars of taxes coming in from China, with the potential of billions and billions of dollars more taxes coming in.”

On the other hand, Chinese Commerce Ministry Spokesman Gao Feng said in a regular press conference that “if the United States, regardless of opposition, adopts any new tariff measures, China will be forced to roll out necessary retaliatory measures.” Both sides have already slapped tit-for-tat tariffs on $US50 billion of each other’s goods. That came after US steel and aluminium tariffs and China’s own retaliation. For the upcoming ones, China already announced counter measures of tariffs on USD 60B of US goods ranging from liquefied natural gas to certain types of aircraft.

Swiss government raised growth forecast after stronger than expected Q2 GDP

Swiss GDP grew faster than expected by 0.7% qoq in Q2, versus expectation of 0.5% qoq. The government also raised growth forecast for this year. A government economist Ronald Indergand said that “for the year as a whole we could be looking at a growth rate much nearer to the 3 percent rate than 2 percent, which would be above the long-term average.” In the prior forecast, the government projected Swiss GDP to grow 2.4% in 2018, comparing to 1.6% in 2017.

Also released European session, German factory orders dropped sharply by -0.9% mom in July versus expectation of 13.7% mom.

BoJ Kataoka criticizes move to allow wider JGB yield band

BoJ board member Goushi Kataoka criticized the central bank’s recent move to allow 10 year JGB yield to fluctuate in a larger range of -0.1% to 0.1%. He said in a speech that “there’s no need to allow long-term interest rates to move in a wider range at a time when the BOJ is cutting its inflation forecasts.” He added that “allowing long-term rates to rise at a time inflation and inflation expectations aren’t heightening much could delay achievement of the BoJ’s price target.” Also, Kataoka warned “global trade frictions are intensifying and there’s no room for complacency”.

Kataoka is a known dove who dissented the decision to keep policy unchanged in every meeting since joining the board in 2017. Instead, he persistently pushed for more aggressive easing, targeting to keep JGB yields at 0% beyond 10 year maturity.

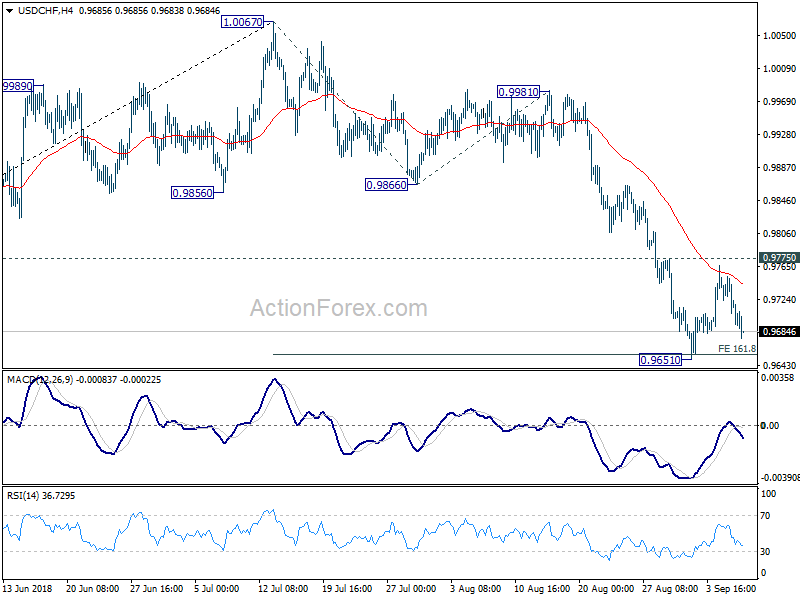

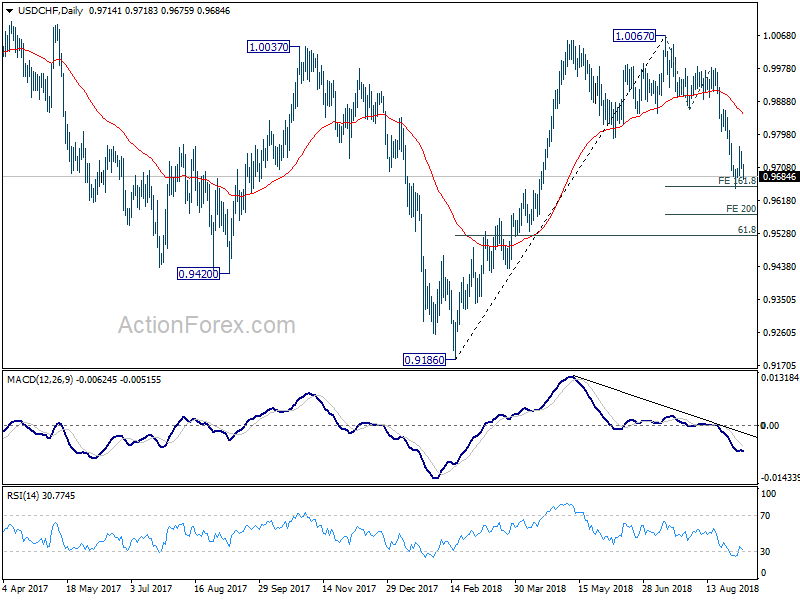

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9699; (P) 0.9727; (R1) 0.9745; More…..

USD/CHF weakens further today after being rejected by 4 hour 55 EMA, but it’s staying in range of 0.9651/9975. Intraday bias stays neutral first. With 0.9775 intact, another decline is mildly in favor. On the downside, break of 0.9651 will target 200% projection of 1.0067 to 0.9866 from 0.9981 at 0.8579 next. However, firm break of 0.9775 will be an early sign of near term reversal. That is, fall from 1.0067 could have completed. In this case, further rally would be seen back to 0.9866 support turned resistance for confirmation.

In the bigger picture, current development suggests that rise from 0.9186 low has completed at 1.0067, after failing to sustain above 1.0037 resistance. Fall from 1.0067 could extend to 61.8% retracement of 0.9816 to 1.0067 at 0.9523 and below. But for now, we don’t expect a break of 0.9186 low. On the upside, firm break of 0.9866 support turned resistance will suggests that fall from 1.0067 has completed and rise from 0.9186 is resuming.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | Trade Balance (AUD) Jul | 1.55B | 1.46B | 1.87B | 1.94B |

| 05:45 | CHF | GDP Q/Q Q2 | 0.70% | 0.50% | 0.60% | 1.00% |

| 06:00 | EUR | German Factory Orders M/M Jul | -0.90% | 1.60% | -4.00% | -3.90% |

| 11:30 | USD | Challenger Job Cuts Y/Y Aug | 13.70% | -4.20% | ||

| 12:15 | USD | ADP Employment Change Aug | 163K | 188K | 219K | 217K |

| 12:30 | CAD | Building Permits M/M Jul | -0.10% | 0.70% | -2.30% | -1.30% |

| 12:30 | USD | Initial Jobless Claims (SEP 1) | 203K | 214K | 213K | |

| 12:30 | USD | Nonfarm Productivity Q2 F | 2.90% | 2.90% | 2.90% | |

| 12:30 | USD | Unit Labor Costs Q2 F | -1.00% | -0.90% | -0.90% | |

| 13:45 | USD | Services PMI Aug F | 55.2 | 55.2 | ||

| 14:00 | USD | ISM Non-Manufacturing/Services Composite Aug | 56.9 | 55.7 | ||

| 14:00 | USD | Factory Orders Jul | -0.10% | 0.70% | ||

| 14:30 | USD | Natural Gas Storage | 70B | |||

| 14:30 | USD | Crude Oil Inventories | -2.6M |

{kind=link}