Dollar is lifted mildly in early US session as employment data posted slight upside surprise. But buying in the greenback is not broad based yet. A key factoring limiting Dollar’ rise is sluggish wage growth. But after all, the set of numbers look way better than February’s. Meanwhile, Canadian Dollar is broadly pressured after poor job data. There is prospect of more downside in the Loonie before weekly close.

Elsewhere in the markets, stocks are generally higher globally, but there is no committed buying. No Trump-Xi summit was announced yesterday but just positive words that progress was made. Trump said “we’re getting very close to making a deal”, “within the next four weeks or maybe less, maybe more”. This is rather empty. UK Prime Minister Theresa May formally seeks Article 50 extensions till June 30. But EU will only provide an answer next week.

In Europe, currently, FTSE is up 0.42%. DAX is up 0.08%. CAC is up 0.34%. German 10-year yield is up 0.021 at 0.017, turned positive, with some conviction. Earlier in Asia, Nikkei rose 0.38%. Singapore Strait Times rose 0.19%. China and Hong Kong were on holiday. Japan 10-year JGB yield rose 0.0082 to -0.03.

US NFP rose 196k, Canada employment dropped -7.2k

US Non-farm payroll employment rose 196k in March, above expectation of 175k. Prior month’s figure was revised slightly up from 20k to 33k. Unemployment rate was unchanged at 3.8%, matched expectations. Labor force participation rate, at 63.0%, was little change on net over the past 12 months. However, average hourly earnings growth slowed to 0.1% mom, below expectation of 0.2% mom. Canadian employment contracted -7.2k, slightly better than expectation of -10k. Unemployment rate was unchanged at 5.8%.

Released earlier, Swiss foreign currency reserves rose to CHF 756B in March, up from CHF 739B. German industrial production rose 0.7% mom in February, below expectation of 0.8% mom. Japan leading indicator rose to 97.4 in February, above expectation of 97.2. Overall household spending rose 1.7% yoy in February, versus expectation of 2.0% yoy. Labor cash earnings dropped -0.8% yoy versus expectation of 0.8% yoy rise. Australia AiG performance of construction index rose slightly to 45.6 in March, up from 43.8.

UK PM May writes to EU Tusk to seek Brexit extension till Jun 30

UK Prime Minister Theresa May wrote a formal letter to European Council President Donald Tusk, requesting Article 50 extension till June 20. May said that she’s already started talks with opposition leader to agree on a proposal for the Commons that allow an order Brexit. Invitation for discussion was also extended more broadly to other MPs to achieve a consensus. If no single unified approach is achieved, May’s Government pledges to look to establish a small number of clear options on future relationship to be put the the House.

May said the steps “demonstrate that the Government is determined to bring this process to a resolution quickly”. And, “the government will want to agree a timetable for ratification that allows the United Kingdom to withdraw from the European Union before 23 May 2019 and therefore cancel the European Parliament elections, but will continue to make responsible preparations to hold the elections should this not prove possible”.

EU said to mull Brexit flextension rather than more short extensions

While May is seeking Brexit extension till June 30, it’s reported that Tusk is considering “flextension” instead. An unnamed EU official was quoted saying “the only reasonable way out would be a long but flexible extension. I would call it a ‘flextension’.” That is, “we could give the UK a year-long extension, automatically terminated once the Withdrawal Agreement has been accepted and ratified by the House of Commons”.

One clear advantage is that even if the Commons cannot approve the WA, “UK would still have enough time to rethink its Brexit strategy. A short extension if possible, and a long one if necessary. It seems to be a good scenario for both sides, as it gives the UK all the necessary flexibility, while avoiding the need to meet every few weeks to further discuss Brexit extensions”.

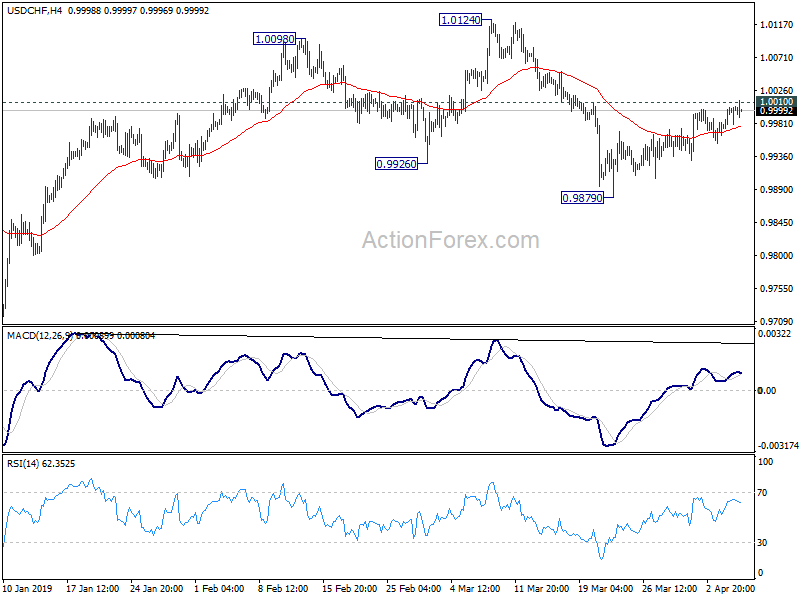

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9977; (P) 0.9991; (R1) 1.0014; More…

USD/CHF’s recovery from 0.9879 extends higher today. 1.0010 minor resistance is breached briefly but not firmly taken out yet. Intraday bias stays neutral first. On the upside, sustained break of 1.0010 will suggest that pull back from 1.0124 has completed. Intraday bias will be turned back to the upside for 1.0124/28 resistance zone. On the downside, break of 0.9879 will resume the fall from 1.0124 to 0.9716 key support.

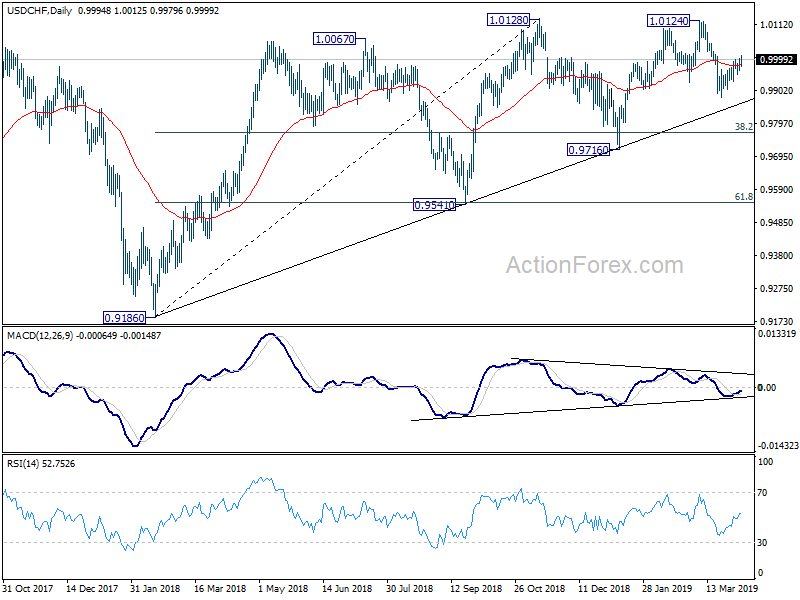

In the bigger picture, focus is back on medium term trend line (now at 0.9849). Decisive break there will argue that whole rise from 0.9186 has completed. Further break of 0.9716 will confirm reversal and target next support level at 0.9541. Nevertheless, there is still a chance that price action from 1.0128 are forming a consolidative pattern with fall from 1.0124 as third leg. If this is the case, stronger support should be seen between 0.9716 and the trend line to contain downside.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Construction Index Mar | 45.6 | 43.8 | ||

| 23:30 | JPY | Overall Household Spending Y/Y Feb | 1.70% | 2.00% | 2.00% | |

| 00:00 | JPY | Labor Cash Earnings Y/Y Feb | -0.80% | 0.80% | 1.20% | -0.60% |

| 05:00 | JPY | Leading Index CI Feb P | 97.4 | 97.2 | 96.5 | |

| 06:00 | EUR | German Industrial Production M/M Feb | 0.70% | 0.80% | -0.80% | |

| 07:00 | CHF | Foreign Currency Reserves (CHF) Mar | 756B | 739B | ||

| 12:30 | CAD | Net Change in Employment Mar | -7.2K | -10.0K | 55.9K | |

| 12:30 | CAD | Unemployment Rate Mar | 5.80% | 5.80% | 5.80% | |

| 12:30 | USD | Change in Non-farm Payrolls Mar | 196K | 175K | 20K | 33K |

| 12:30 | USD | Unemployment Rate Mar | 3.80% | 3.80% | 3.80% | |

| 12:30 | USD | Average Hourly Earnings M/M Mar | 0.10% | 0.20% | 0.40% |

{kind=link}