European majors are trading generally lower today, in quiet markets just ahead of monthly close. On the other hand, Dollar is among the strongest together with Aussie and Kiwi. Despite steep selloff in Asian stocks, European markets recover after initial weakness. Bond markets are steady with major treasury yields rising slightly. Such development should keep Yen weak, in particular USD/JPY.

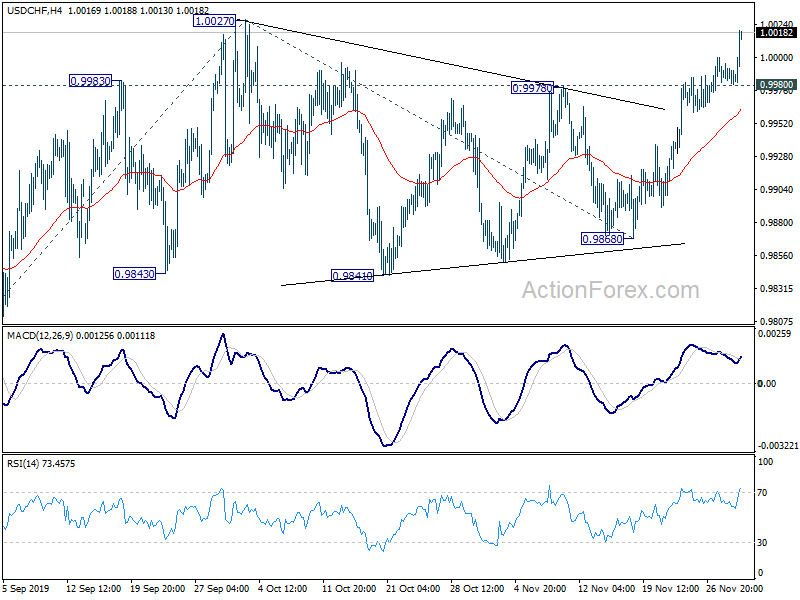

Technically, EUR/USD’s break of 1.0989 support indicates resumption of fall from 1.1175 finally. It’s now heading back to 1.0879 low. USD/CHF will take on 1.0027 resistance very soon. Break will resume whole rise from 0.9659. These are the two pairs to watch just before weekly close.

In Europe, FTSE is currently down -0.32%. DAX is up 0.30%. CAC is up 0.26%. German 10-year yield is up 0.0011 at -0.348. Earlier in Asia, Nikkei dropped -0.49%. Hong Kong HSI dropped -2.03%. China Shanghai SSE dropped -0.61%. Singapore Strait Times dropped -0.21%. Japan 10-year JGB yield rose 0.0072 to -0.082.

Canada GDP grew 0.1% in Sep, 0.3% in Q3

Canada GDP grew 0.1% mom in September, matched expectations. Increase in services (+0.2%) slightly outpacing the increase in goods (+0.1%). Growth was recorded in 13 of 20 industrial sectors.

For Q3, GDP growth slowed to 0.3%, down from Q2’s 0.9%. Expressed at annualized rate GDP grew 1.3%. Business investment rose 2.6% in the third quarter, the fastest pace since the fourth quarter of 2017. Growth in household spending accelerated to 0.4%, after rising 0.1% in the second quarter. These increases were moderated by a 0.4% decline in exports, while imports were flat.

Also from Canada, IPPI rose 0.1% mom in October, above expectation of 0.0% mom. RMPI dropped -1.9% mom, matched expectations.

Eurozone CPI rose to 1.0%, core up to 1.3%

Eurozone CPI accelerated to 1.0% yoy in November, up from 0.7% yoy, beat expectation of 0.8% yoy. CPI core also accelerated to 1.3% yoy, up from 1.1% yoy, beat expectation of 1.2% yoy.

Germany unemployment dropped -16k in November, versus expectation of 5k rise. Unemployment rate was unchanged at 5%, matched expectations. Retail sales, however, dropped -1.9% mom, much worse than expectation of -0.2% mom.

Swiss KOF dropped to 93, economic outlook remains subdued

Swiss KOF Economic Barometer dropped to 93.0 in November, down from 94.8, and missed expectation of 95.0. It’s also the lowest level since 2015. KOF said: “The downward movement, which has been observed since the beginning of the year, continues. The barometer is still well below its long-term average. The outlook for the Swiss economy remains subdued.”

Also, “Several bundles of indicators are equally responsible for the decline. However, negative signals from hotel and catering activities and from the banking and insurance sector stand out slightly. Indicators regarding foreign demand and other services are also declining. On the other hand, indicators for the manufacturing sector remain almost unchanged.”

UK Gfk consumer confidence unchanged at -14, upcoming election an opportunity to move UK out of doldrums.

UK GfK Consumer Confidence was unchanged at -14 in November, matched expectations. General Economic Situation index over the next 12 months improved by 3 pts from -37 to -34, two points lower than -32 a year ago. Joe Staton, Client Strategy Director at GfK, says: “In the face of Brexit and election uncertainty, consumers are clearly in a ‘wait-and-see’ mode…

“The general election is potentially an opportunity to move us out of the doldrums – but for this to happen there must be a clear result. A hung parliament could be very damaging for consumer confidence and would surely deepen the obvious malaise that we see month after month.”

Japan industrial production posted largest contraction in nearly two years

Japan industrial production dropped sharply by -4.2% mom in October, missing expectation of -2.1% mom. That’s also the worst decline in nearly two years since January 2018. Output was seen as negatively impacted by temporary shutdowns of factories due to typhoon. Also slowing productions of big-ticket items following sales tax hike also weighed.

METI also noted that according to the Survey of Production Forecast in Manufacturing, production is expected to decrease in November and increase in December. Finance Minister Taro Aso said the government would consider more funding or cashless support to secure the economy’s recovery trend.

Also from Japan, unemployment rate was unchanged at 2.4% in October, matched expectations. Housing starts dropped -7.4% yoy versus expectation of -7.6% yoy. Tokyo CPI core edged up to 0.6% yoy in November, matched expectations. Consumer confidence rose to 38.7, up from 36.2.

BoJ Kuroda pushes deregulation and structural reforms

BoJ Governor Haruhiko Kuroda told the parliament today that “a mix of fiscal and monetary policy isn’t enough” to boost the economy. It’s also important to “proceed with deregulation and structural reforms to heighten Japan’s medium- and long-term growth potential.”

Kuroda repeated his view that the ultra-look monetary policy could increase the effect of fiscal stimulus. However, he also emphasized “our monetary easing efforts are aimed at achieving our price target, not at helping fund government spending. There needs to be a clear line drawn on this point,”

Executive Director Eiji Maeda told the parliament that “current ultra-loose monetary environment is stimulating the economy by spurring capital expenditure and housing investment.” That will “push up” household income and asset prices. But policymakers are also “mindful” on the “excessive declines” in super-long yields. He warned that could ‘hurt public sentiment and economic activity by lowering the interest life insurers and pension funds earn from their investment”.

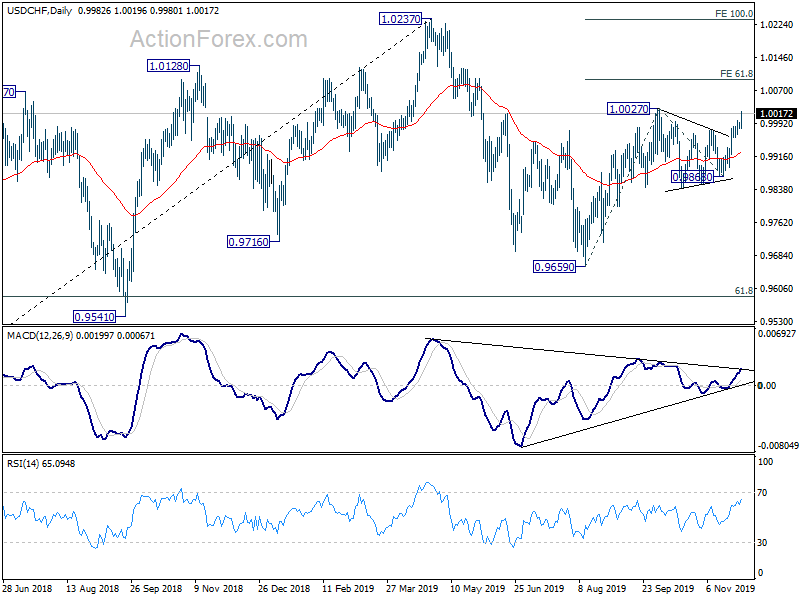

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9977; (P) 0.9989; (R1) 1.0007; More…

USD/CHF rises to as high as 1.0019 so far. Intraday bias stays on the upside for 1.0027 resistance first. Break will resume whole rise from 0.9659. Next upside target will be 61.8% projection of 0.9659 to 1.0027 from 0.9869 at 1.0095. On the downside, below 0.9980 minor support will delay the bullish case and turn intraday bias neutral first.

In the bigger picture, medium term outlook remains neutral as USD/CHF is staying in range of 0.9659/1.0237. In any case, decisive break of 1.0237 is needed to indicate up trend resumption. Otherwise, more sideway trading would be seen with risk of another fall. Meanwhile, break of 0.9695 support will target 0.9541 support instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits M/M Oct | -1.10% | 7.20% | 7.40% | |

| 23:30 | JPY | Tokyo CPI Core Y/Y Nov | 0.60% | 0.60% | 0.50% | |

| 23:30 | JPY | Unemployment Rate Oct | 2.40% | 2.40% | 2.40% | |

| 23:50 | JPY | Industrial Production M/M Oct P | -4.20% | -2.10% | 1.70% | |

| 00:01 | GBP | GfK Consumer Confidence Nov | -14 | -14 | -14 | |

| 00:30 | AUD | Private Sector Credit M/M Oct | 0.10% | 0.30% | 0.20% | |

| 05:00 | JPY | Housing Starts Y/Y Oct | -7.40% | -7.60% | -4.90% | |

| 05:00 | JPY | Consumer Confidence Index Nov | 38.7 | 35.4 | 36.2 | |

| 08:00 | CHF | KOF Leading Indicator Nov | 93 | 95 | 94.7 | |

| 08:55 | EUR | Germany Unemployment Rate Nov | 5% | 5% | 5% | |

| 08:55 | EUR | Germany Unemployment Change Nov | -16K | 5K | 6K | |

| 09:30 | GBP | Mortgage Approvals Oct | 65K | 65K | 66K | |

| 09:30 | GBP | M4 Money Supply M/M Oct | 0.00% | 0.50% | 0.70% | |

| 10:00 | EUR | Eurozone Unemployment Rate Oct | 7.50% | 7.50% | 7.50% | |

| 10:00 | EUR | Eurozone CPI Y/Y Nov P | 1.00% | 0.80% | 0.70% | |

| 10:00 | EUR | Eurozone CPI – Core Y/Y Nov P | 1.30% | 1.20% | 1.10% | |

| 13:30 | CAD | GDP M/M Sep | 0.10% | 0.10% | 0.10% | |

| 13:30 | CAD | Raw Material Price Index Oct | -1.90% | -1.90% | 0.00% | |

| 13:30 | CAD | Industrial Product Price M/M Oct | 0.10% | 0.00% | -0.10% |

{kind=link}