Markets are somewhat staying in risk on mode with US stock indices making new record highs overnight. But upside momentum in Asia markets is relatively weak. Australian and New Zealand Dollars are mildly firmer today, paring some of this week’s losses. Meanwhile, Yen and Canadian Dollar are the weaker ones. For the week, Sterling is so far the strongest, followed by Dollar, while Yen and Aussie are weakest. Dollar has a chance to overtake the Pound to close as the best performer, depending on non-farm payrolls report from US.

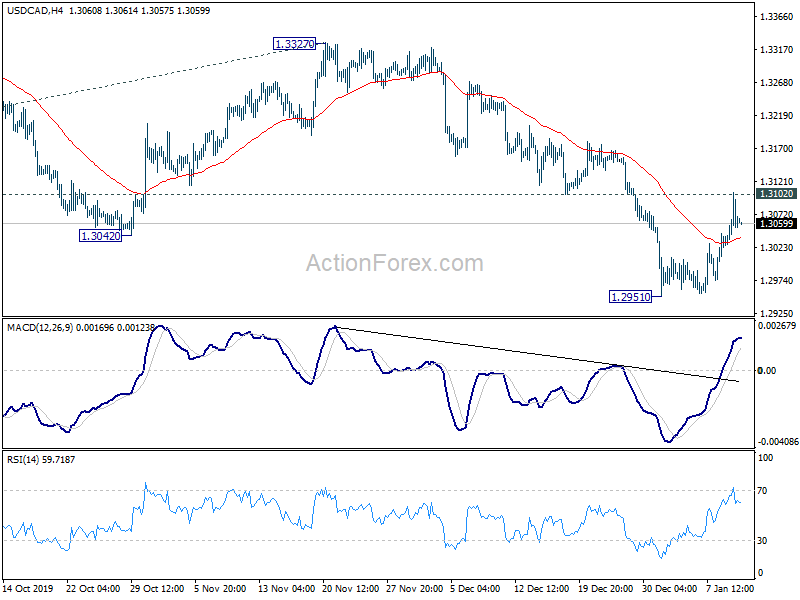

Technically, 109.72 resistance in USD/JPY could be the most important level to watch today. It’s reaction to NFP would decide whether Dollar could extend recent rebound attempt. Break of 109.72 will resume whole rise from 104.45. 1.3102 support turned resistance in USD/CAD is another level to watch. Canadian Dollar turned weaker, together with oil price, as Iran risks subsided. Comparative strength of US and Canadian job data should be the factor to determine the next move in USD/CAD.

In Asia, Nikkei closed up 0.47%. Hong Kong HSI is up 0.17%. China Shanghai SSE is down -0.08%. Singapore Strait Times is up 0.19%. Japan 10-year JGB yield is down -0.0059 at 0.001, staying positive. Overnight, DOW rose 0.74%. S&P 500 rose 0.67%. NASDAQ rose 0.81%. All three indices closed at record highs. 10-year yield dropped -0.016 to 1.858, after hitting 1.9 handle.

Fed Clarida: US economy begins 2020 in a good place

Fed Vice Chair Richard Clarida said the US economy begins 2020 “in a good place”. PCE price inflation is “running somewhat below” the 2% target. But Fed projects that inflation will “rise gradually” back to the 2% symmetric objective. Meanwhile, there is no evidence that a strong labor market is “putting excessive cost-push pressure on price inflation”.

Over the course of 2019, FOMC shifted the monetary stance to “offset some significant global growth headwinds and global disinflationary pressures.” Such shift was “well timed” and has helped keep the outlook on track. ” As long as incoming information about the economy remains broadly consistent with this outlook, the current stance of monetary policy likely will remain appropriate.”

Monetary policy is “not on a preset course”, he added. “if developments emerge that, in the future, trigger a material reassessment of our outlook, we will respond accordingly.

Fed officials are comfortable with rates at current level

Comments from Fed officials yesterday generally suggested that interest rates are currently at the right place. There won’t be further rate cut unless outlook worsens materially.

St. Louis Fed President James Bullard said that the current 2020 baseline outlook suggests reasonable chance of “soft landing”. While growth is expected to slow, US is not facing a “sharper than anticipated” collapse. The three rate cuts in 2019 were “a substantial move”. “Now we should wait and see what the effects are in the first half of 2020 and beyond that,”

Minneapolis Fed President Neel Kashkari said that “trade tensions with China don’t seem to be increasing, so that’s a positive.” That could “translate into more business investment”. He added that Fed’s rate cuts have “taken some of the recession risk off the table.””We think inflation is around the corner and then inflation doesn’t come because we raise rates prematurely,” he said. “Now that we’re in a pause mode I think we’re in a much better position.”

Chicago Fed President Charles Evans said “I see the fundamentals as pretty good.” “If something were to happen that caused the economy to slow down and perhaps do worse than that then that would call for some type of response on the downward fashion. But I’m not expecting that”.

Dallas Fed President Robert Kaplan said federal funds rate at 1.50-1.75% is “a roughly appropriate setting.” GDP is expected to grow about 2% to 2.25% this year, “and if anything my growth outlook has firmed a bit in the last several weeks.” He also backed the view that rates should stay at current level unless there is “material” change in the outlook.

NFP to guide Dollar’s rebound, Gold in medium term correction?

Non-farm payrolls report from US will be the most important even today, which could determine whether Dollar could extend the current rebound. Markets are expecting 160k jobs added in December. Unemployment rate is expected to be unchanged at 3.50%. Average hourly earnings are expected to grow 0.3% mom.

Looking at other employment data, ISM manufacturing employment dropped from 46.6 to 45.1, staying in deep contraction. But ISM services employment remained firm in expansion, down slightly from 55.5 to 55.2. The relative strength was clearly reflected in private sector jobs too. ADP jobs grew 202k, with 173k in services jobs and 29k in goods-producing jobs. Four-week moving average of initial claims rose slightly to 224k, up from 218k. Overall, services sector is the key to whether NFP would shine.

Gold should have topped out in near term at 1611.37, ahead of 61.8% projection of 1266.26 to 1557.04 from 1445.59 at 1625.29. We’re also seeing the five wave sequence from 1160.17 as being completed. Thus, it should now be in a medium term corrective pattern. Downside target of the correction is 1145.59, which is close to 38.2% retracement of 1160.17 to 1611.37 at 1439.01. But that would very much depends on today’s NFP as well as Dollar’s reaction.

Elsewhere

Australia retail sales rose 0.9% mom in November, seasonally adjusted, above expectation of 0.4% mom. AiG Performance of Services Index dropped sharply to 48.7 in December, down from 53.7. Japan overall household spending dropped -2.0% yoy in November, matched expectations.

Looking ahead, Swiss will release unemployment rate in Europaen session. France and Italy will release industrial output. Later in the day, NFP will catch most attention. But Canada employment is also important.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3019; (P) 1.3062; (R1) 1.3098; More….

USD/CAD’s recovery from 1.2951 extended higher but couldn’t break through 1.3102 resistance so far. Outlook is unchanged and further decline remains in favor. On the downside, break of 1.2951 will target 100% projection of 1.3564 to 1.3016 from 1.3327 at 1.2779 next. However, sustained break of 1.3102 will confirm short term bottoming and target 55 day EMA (now at 1.3152) and above.

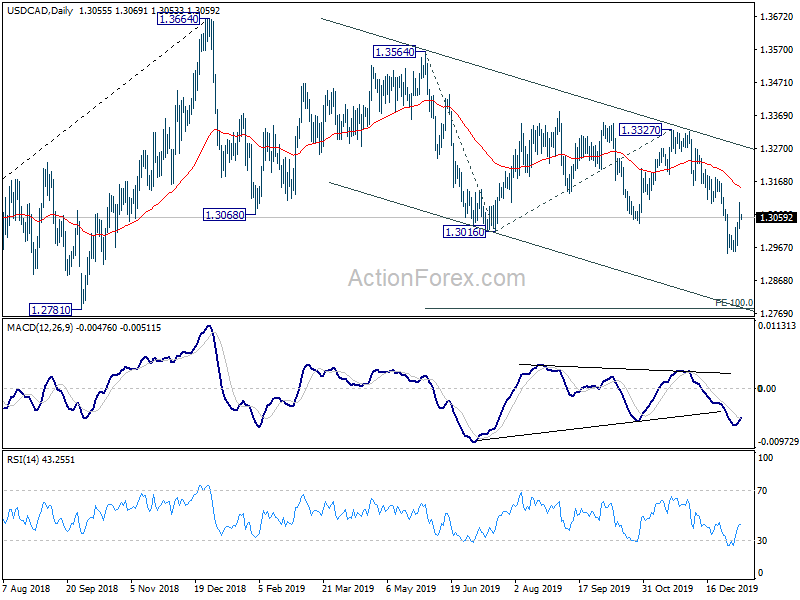

In the bigger picture, rise from 1.2061 (2017 low) could have completed at 1.3664, after failing 61.8% retracement of 1.4689 (2016 high) to 1.2061 at 1.3685. However, structure of price actions from 1.3664 argues that it’s probably just a corrective move. Hence, while further fall is expected, downside should be contained by 61.8% retracement of 1.2061 to 1.364 at 1.2673. Nevertheless, sustained break of 1.2673 will put focus on 1.2061 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Services Index Dec | 48.7 | 53.7 | ||

| 23:30 | JPY | Overall Household Spending Y/Y Nov | -2.00% | -2.00% | -5.10% | |

| 0:30 | AUD | Retail Sales M/M Nov | 0.90% | 0.40% | 0.00% | 0.10% |

| 5:00 | JPY | Leading Economic Index Nov P | 90.6 | 91.6 | ||

| 6:45 | CHF | Unemployment Rate Dec | 2.30% | 2.30% | ||

| 7:45 | EUR | France Industrial Output M/M Nov | 0.10% | 0.40% | ||

| 9:00 | EUR | Italy Industrial Output M/M Nov | 0.00% | -0.30% | ||

| 13:30 | USD | Nonfarm Payrolls Dec | 160K | 266K | ||

| 13:30 | USD | Unemployment Rate Dec | 3.50% | 3.50% | ||

| 13:30 | USD | Average Hourly Earnings M/M Dec | 0.30% | 0.20% | ||

| 13:30 | CAD | Net Change in Employment Dec | 20.0K | -71.2K | ||

| 13:30 | CAD | Unemployment Rate Dec | 5.80% | 5.90% | ||

| 15:00 | USD | Wholesale Inventories Nov | 0.00% | 0.00% |

{kind=link}