Canadian and Australian Dollar trade generally higher today, following mild strength in Asian stocks. But New Zealand Dollar diverges from them as the country extends lockdown of Auckland until Sunday night. Following Kiwi, Swiss Franc and Yen are the next weakest in risk-on markets. Dollar is mixed and could stay so until Fed Chair Jerome Powell’s Jackson Hole speech later in the week.

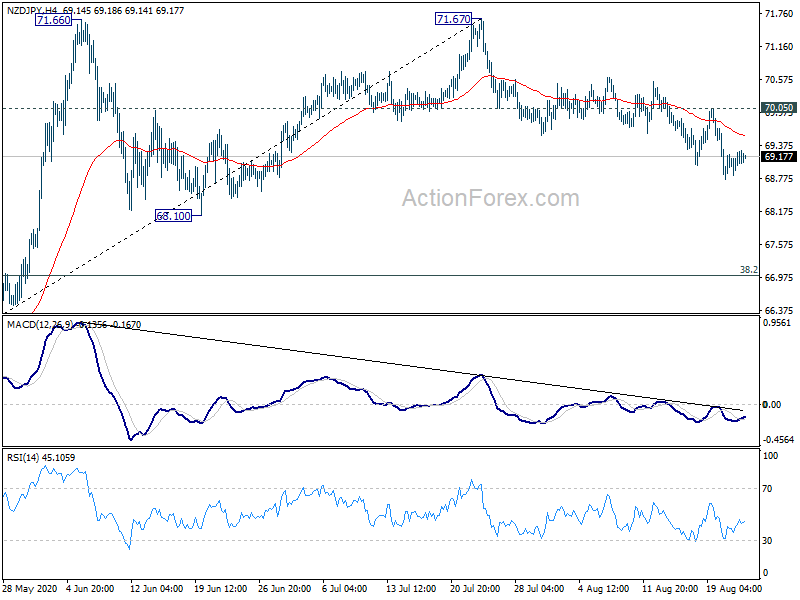

Technically, while Yen turns slightly softer today, there is no clear sign of completing last week’s rebound yet. NZD/JPY’s decline from 71.67 is still in progress for 68.10 support. Eyes will also be on 124.31 support in EUR/JPY and 137.84 support in GBP/JPY. Break there will confirm topping in both crosses and pave the way for deeper correction lower. 1.0739 support in EUR/CHF will also be watched and break will indicate completion of recent rebound from 1.0602, and bring retest of this support.

In Asia, currently, Nikkei is up 0.26%. Hong Kong HSI is up 1.41%. China Shanghai SSE is up 0.18%. Singapore Strait Times is up 0.23%. Japan 10-year JGB yield is down -0.0096 at 0.026.

New Zealand retail sales dropped record -14.6% in Q2, not unexpected

New Zealand retail sales dropped a record -14.6% qoq (ex-inflation) in Q2, better than expectation of -16.3% qoq. “This unprecedented fall in the June quarter was not unexpected, with COVID-19 restrictions significantly limiting retail activity,” StatsNZ retail statistics manager Kathy Hicks said.

12 of the 15 industries had lower sales over the year too. Some had record decline, and the main movements were: Food and beverage services, down -40%; fuel retailing, down -35%; motor vehicle and parts retailing, down -22%; accommodation, down -44%.

Japan Abe in hospital for the second time in a week

Concerns over Japanese Prime Minister Shinzo Abe’s health flared up again today as his visited a Tokyo hospital for the second time in a week. Some said Abe was just receiving the results of a medical check-up from a week ago, when he underwent a 7-hour examination. On the other hand, Nippon TV reported that he’s getting treatment for chronic illness.

Speculations about Abe’s health started earlier this month, with some Cabinet members expressing concerns of his exhaustion on fighting the coronavirus pandemic. There were also detailed reports on Abe’s walking speed. If the longest-serving prime minister couldn’t continue his job on health issue, Deputy Prime Minister Taro Aso would take over temporarily, awaiting the ruling LDP to elect a new leader.

BoK Lee: recovery to remain weak as virus cases resurged

Bank of Korea Governor. Lee Ju-yeol told the National Assembly, “after suffering sharp deterioration, the Korean economy showed some signs of an improvement on eased slumps in exports and consumption.”

But he warned, “as virus cases have recently resurged, the economic recovery is expected to remain weak, and economic uncertainty has further heightened.” “We will also closely monitor changes in financial stability, stemming from growing household debt amid rising home prices and excessive cash inflows to the housing market”.

BOK lowered policy rate to record lower of 0.50% in May. It’s expected to stand pay at the meeting on Thursday. South Korean economy contracted -3.3% qoq in Q2, worst in over two decades.

Fed Powell’s Jackson Hole speech highlights the week

Fed Chair Jerome Powell’s speech at the annual Jackson Hole Symposium is the main highlight of the week. The Fed’s view on the economic and monetary policy responses have been rather clearly communicated in the past few months. Instead, attention will mainly be on information regarding the policy framework review. The annual event, titled “Navigating the Decade Ahead: Implications for Monetary Policy,” should be an ideal occasion to launch the upcoming changes.

On the data front, the calendar is relatively light. Here are some highlights for the week:

- Monday: New Zealand Retail sales

- Tuesday: Germany GDP final, ifo business climate: UK CBI realized sales; US house price indices, consumer confidence, new home sales.

- Wednesday: New Zealand trade balance; Australia construction work done; Japan corporate service price; US durable goods orders.

- Thursday: Australia private capital expenditure; Japan all industries activity index; Swiss GDP; Eurozone M3 money supply; Canada current account; US GDP revision, jobless claims, pending home sales.

- Friday: Japan Tokyo CPI; German Gfk consumer sentiment, import prices; France GDP, consumer spending, CPI; Canada GDP; US personal income and spending, goods trade balance, wholesale inventories, Chicago PMI.

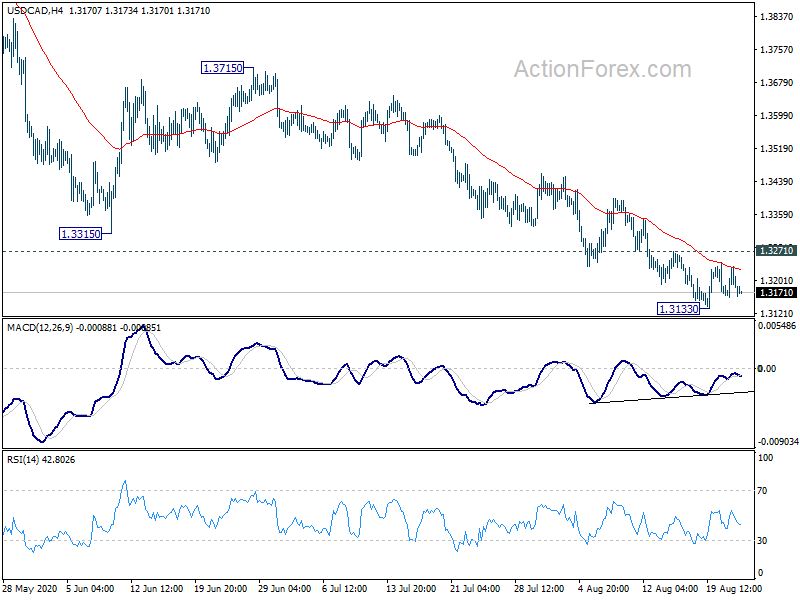

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3154; (P) 1.3194; (R1) 1.3229; More….

Intraday bias in USD/CAD remains neutral for consolidations. Further decline is expected as long as 1.3271 resistance holds. Break of 1.3133 will resume larger fall from 1.4667 to long term fibonacci level at 1.3056. On the upside, considering bullish convergence condition, firm break of 1.3271 should confirm short term bottoming. Intraday bias will be turned back to the upside for rebound to 55 day EMA (now at 1.3439).

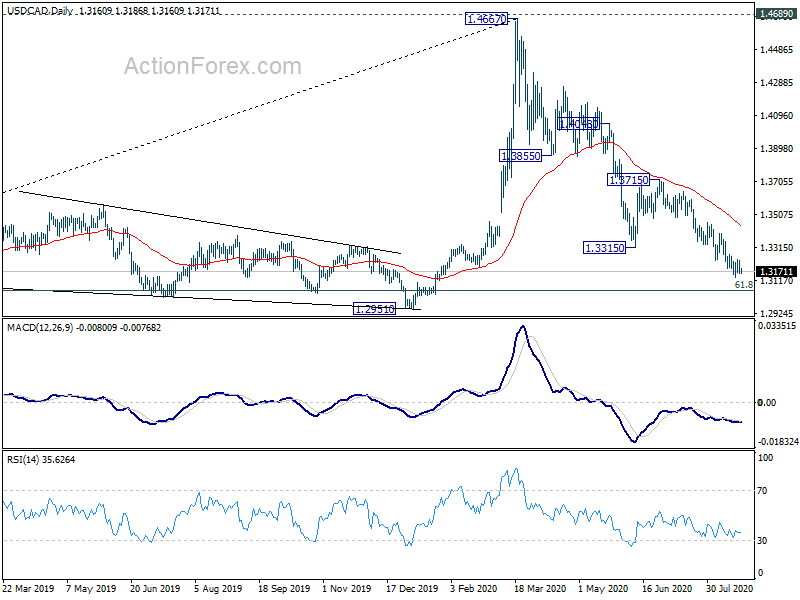

In the bigger picture, the rise from 1.2061 (2017 low) could have completed at 1.4667 after failing 1.4689 (2016 high). Fall from 1.4667 could be the third leg of the corrective pattern from 1.4689. Deeper fall is expected to 61.8% retracement of 1.2061 to 1.4667 at 1.3056 and possibly below. This will now remain the favored case as long as 1.3715 resistance holds. However, sustained break of 1.3715 will turn focus back to 1.4689 key resistance.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Retail Sales Q/Q Q2 | -14.60% | -16.30% | -0.70% | -1.20% |

| 22:45 | NZD | Retail Sales ex Autos Q/Q Q2 | -13.70% | -15.00% | 0.60% | 0.10% |

| EUR | German Buba Monthly Report |

{kind=link}