Dollar recovers broadly today as the weekend passed without any geopolitical events. But the greenback is slightly out-performed by Canadian Dollar. Meanwhile, Swiss Franc and Yen trade broadly losing, paring some of last week’s risk aversion gains This pattern is also seen in other markets as gold is back pressing 1340 handle after hitting as high as 1362.4 last week. Economic calendar is rather light today and the forex markets will likely engage in some more consolidative trading. Nonetheless, more key events are scheduled for the week ahead including UK inflation, BoE and SNB meeting.

Geopolitical tensions moderated temporarily

Geopolitical tensions showed signs of temporary moderation as North Korea had not launched another missile test on September 9, the founding anniversary of the country. However, the US submitted a draft resolution to the UNSC last Friday proposing to add new sanctions against North Korea. The US is pushing to vote for the notion as UNSC members meet today. The US and Japan have been pushing for harsher sanctions against the hermit kingdom. On the other hand, China and Russia, the two UNSC veto powers besides the US, the UK, and France, are reluctant to impose tougher measures, let alone military intervention. North Korea has warned that the US has to pay the price for strengthening sanctions.

Harvey and Irma could cost USD 190b damage, 1.5% of GDP

In US, hurricane Irma made landfall Sunday as forecasted. According to AccuWeather, the damage from Irma could be at around USD 100b, among the costliest hurricanes of all time. And that is 0.5% of GDP of USD 19T. Damage of hurricane Harvey is estimated to be even worse at USD 190b, at nearly 1% of GDP. Together, the damages could be up to USD 190b, at 1.5% of GDP. Also, this is the first time two Category 4 hurricanes have hit US in the same year.

UK Parliament to vote on Brexit Repeal Bill

In UK, eyes will be on a parliamentary vote of the so called Brexit "Repeal Bill" today. In short, the bill seeks to copy and paste EU laws into UK legislation so that UK will have the same functioning laws and regulatory framework at the time of Brexit. Brexit Secretary David Davis warned that a vote against the bill is "a vote for chaotic exit from the European Union". And he emphasized that "businesses and individuals need reassurance that there will be no unexpected changes to our laws after exit day and that is exactly what the repeal bill provides. Without it, we would be approaching a cliff edge of uncertainty which is not in the interest of anyone." The government will need to secure the votes today to move on to the next phase of the legislation process. Opposition Labour Party has already indicated that they will vote against unless there are concessions.

China cut forex reserve requirement from 20% to 0%.

In China, the PBoC will unwind the rules on forex exchange forward reserve requirements that were implemented back in 2015. Back then the Renminbi exchange rate suffered prolonged depreciation after the devaluation in August 2015. The implementation of 20% reserve requirement was a move to halt the unwanted speculation in the exchanged rate. Effective today, the requirement is cut down to 0%. The move is seen by the markets as the government is adopting a more liberalized approach to Yuan trading. And it’s also an act to soften restriction on capital outflow. Released over the weekend, China CPI accelerated to 1.6% yoy in August, up from 1.4% yoy. PPI slowed to 5.4% yoy, below 5.5% yoy.

Elsewhere in Asia, Japan machine orders rose 8.0% mom in July, M2 rose 4.0% yoy, Tertiary industry index rose 0.1% mom in July. Canadian housing starts is the only featured in the calendar today.

UK CPI, BoE and SNB to highlight the week

Looking ahead, it will be a particular big week for Sterling. UK inflation data to be released on Tuesday will be the first to watch. CPI is expected to climb back to 2.8% yoy in August. Tamer than expected inflation reading has cooled the speculations of an early rate hike by BoE. Indeed, there are talks that inflation would not even touch 3% level. Baring any upside surprise, BoE will likely remains on hold until the Brexit picture becomes clear. And talking about BoE, the monetary policy decision to be delivered on Thursday will be a major focus too. While the central bank is widely expected to keep bank rate and asset purchase target unchanged, attention will be on the vote split. In particular, eyes will be on whether hawks Michael Saunders and Ian McCafferty would change their mind.

SNB rate decision will be another major focus too. The Swiss franc suffered steep selling back in July but it has then stabilized. Indeed, rising geopolitical tensions have given the Franc a lift recently. SNB chairman Thomas Jordan has also indicated his cautious stance earlier this month. He emphasized that "it doesn’t make any sense to jeopardize the recovery by tightening our monetary policy." And, the selloff and Franc back earlier just reduced the "significant overvaluation. And, situation in the exchange rate "remains fragile". He doubted if " the short-term movements we see in the markets are sustainable."

Elsewhere, US inflation data will be another key focus of the week. Australia employment and a batch of China data on Thursday will also be watched.

Here are some highlights for the week ahead:

- Tuesday: Australia NAB business confidence; UK CPI, RPI, PPI, house price index; US JOLTS job openings

- Wednesday: Australia Westpac consumer confidence; German CPI final; Swiss PPI, UK employment; Eurozone industrial production, employment; US PPI

- Thursday: Australia employment, China retail sales, industrial production, fixed assets investment. SNB rate decision; BoE rate decision; Canada new housing price index; US jobless claims, CPI

- Friday: New Zealand Business NZ manufacturing index; Eurozone trade balance; US empire state manufacturing, retail sales, industrial production, U of Michigan sentiment, business inventories.

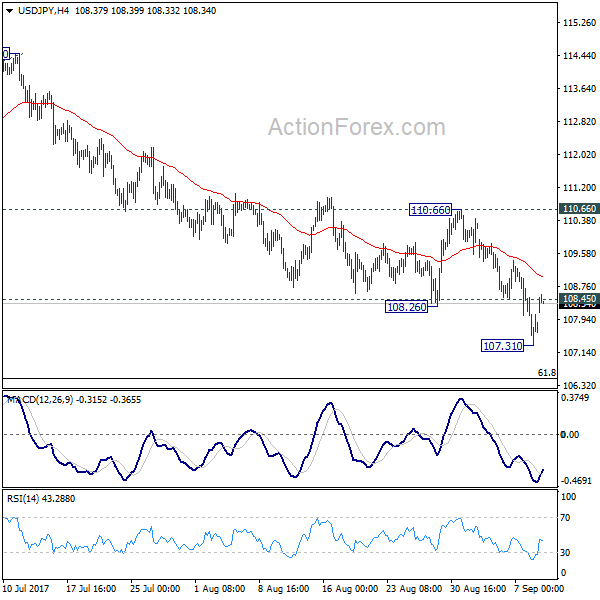

USD/JPY Daily Outlook

Daily Pivots: (S1) 107.27; (P) 107.88; (R1) 108.44; More…

USD/JPY’s strong rebound today suggests temporary bottoming at 107.31. Intraday bias is turned neutral for consolidations first. But outlook will remain bearish as long as 110.66 resistance holds. And, deeper decline is expected. Below 107.31 will extend the whole fall from 118.65 to 61.8% retracement of 98.97 to 118.65 at 106.48 first. We’d look for support from there to bring rebound. But firm break of 106.48 will extend the decline to 100% projection of 118.65 to 108.12 from 114.49 at 103.96 or below.

In the bigger picture, rise from 98.97 (2016 low) is now seen as the second leg of the corrective pattern from 125.85 (2015 high). It’s unclear whether this this second leg has completed at 118.65 or not. But medium term outlook will be mildly bearish as long as 114.49 resistance holds. And, there is prospect of breaking 98.97 ahead. Meanwhile, break of 114.49 will bring retest of 125.85 high. But even in that case, we don’t expect a break there on first attempt.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Machine Orders M/M Jul | 8.00% | 4.10% | -1.90% | |

| 23:50 | JPY | Japan Money Stock M2+CD Y/Y Aug | 4.00% | 4.10% | 4.00% | |

| 4:30 | JPY | Tertiary Industry Index M/M Jul | 0.10% | 0.10% | 0.00% | |

| 6:00 | JPY | Machine Tool Orders Y/Y Aug P | 28.00% | |||

| 12:15 | CAD | Housing Starts Aug | 220.0K | 222.3K |