Dollar remains the firmer one today, in quiet markets, as traders are awaiting Fed’s rate hike, and forward guidance later in the week. Yen’s trading tone is so far positive, as risk markets lack buyers. Commodity currencies are weak together with Euro and Sterling. Aussie is the relatively steadier one as markets await tomorrow’s RBA hike. Canadian Dollar and also turning weak, as dragged down by falling oil price. But Kiwi is still the worst performer.

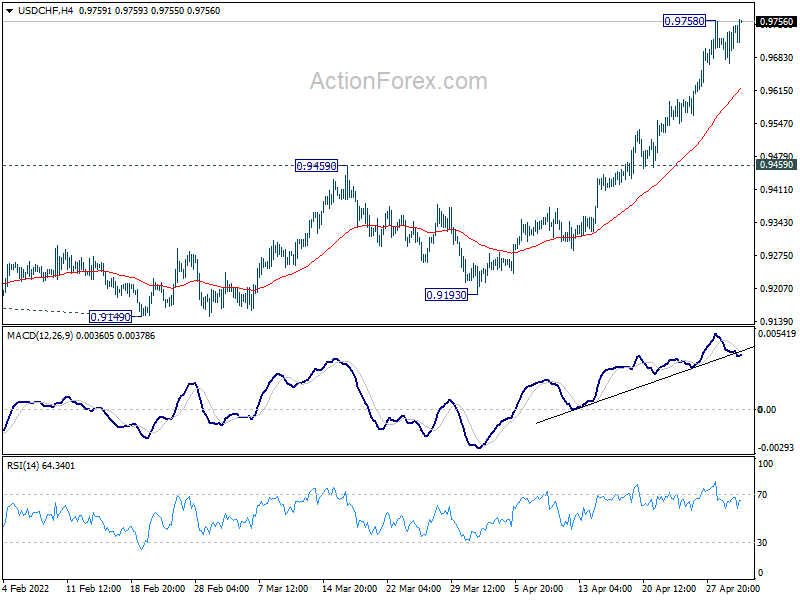

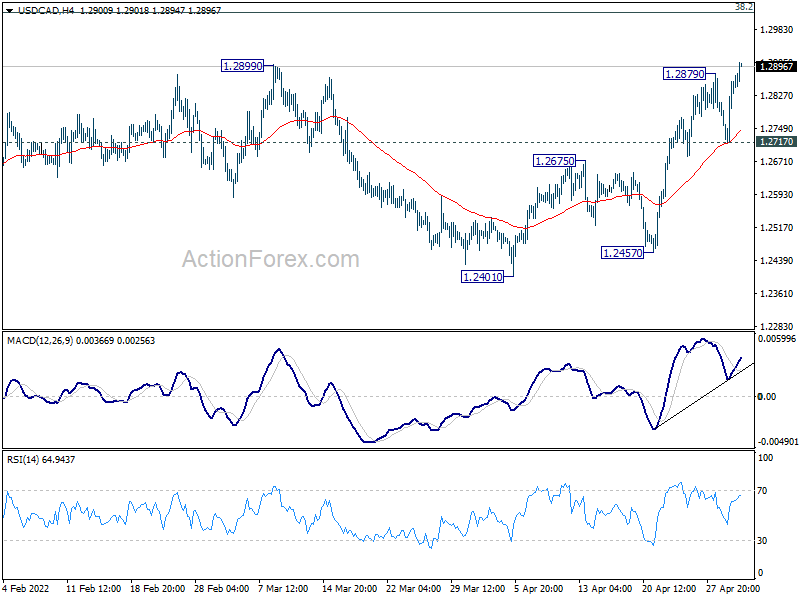

Technically, Dollar’s broad-based rally is making some progress. USD/CAD has taken out 1.2879 temporary top. USD/CHF also takes out 0.9758 temporary top too. Now, focus is on 1.0470 temporary low in EUR/USD and 131.24 temporary top in USD/JPY. Break of these two levels should confirm underlying strength of the greenback.

In Europe, at the time of writing, DAX is down -1.07%. CAC is down -1.84%. Germany 10-year yield is down -0.0021 at 0.942. UK is on bank holiday. Earlier in Asia, Nikkei dropped -0.11%. Japan 10-year JGB yield rose 0.011 to 0.230. Singapore Strait Times rose 0.65%. Hong Kong and China were on holiday.

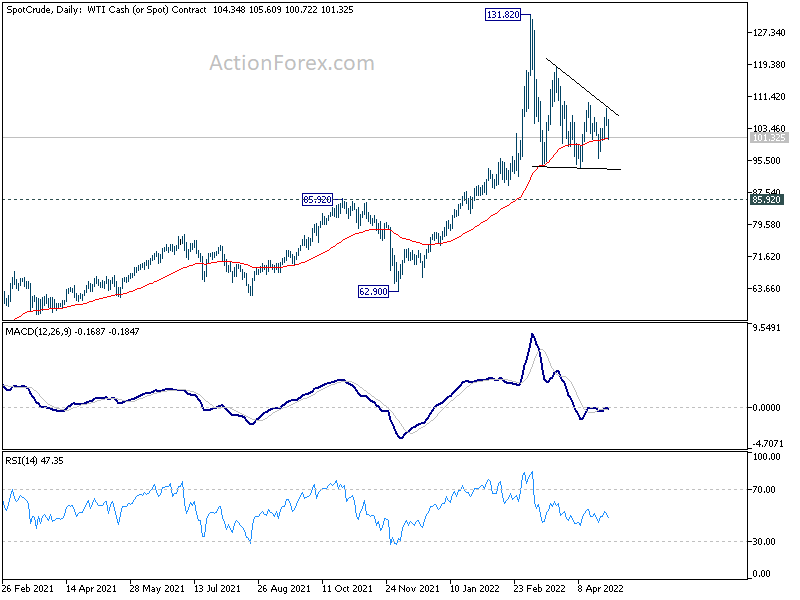

WTI crude oil heading back through 100 on China worries

Oil prices drop notably today on worries over China’s economy. Data released over the weekend showed PMIs hitting the lowest level since February 2020 due to lockdowns. The economy is on the verge of contraction in Q2 as situation is unlikely to improve any time soon. Meanwhile, Libya also temporary resume operation at a terminal, adding to global supply.

WTI should have finished the rebound form 95.87 and it’s now heading back through 100 handle, towards 95.87 support. But overall, it’s seen as developing another falling leg inside the medium term triangle corrective pattern that started back in 131.82. Downside should be contained by 93.47 support. Larger up trend is still expected to resume at a later stage. The bigger question is whether the final rally of the up trend would ended as a failure fifth that couldn’t even pass through 131.82 high.

Eurozone economic sentiment dropped to 105, employment expectation dropped to 112.4

Eurozone Economic Sentiment Indicator dropped from 106.7 to 105.0 in April. Industry confidence dropped from 9.0 to 7.9. Services confidence ticked down from 13.6 to 13.5. Consumer confidence dropped from -21.6 to -22.0. Retail trade confidence dropped from -2.4 to -4.3. Construction confidence rose from 8.9 to 7.1. Employment Expectation Indicator dropped from 113.5 to 112.4.

EU Economic Sentiment dropped from 106.6 to 104.9. Amongst the largest EU economies, the ESI fell markedly in Spain (-4.5) and to a lesser extent in France (-1.4). Confidence remained broadly stable in Germany (-0.1), the Netherlands (-0.1) and Poland (+0.3), while it improved in Italy (+1.3). Employment Expectation Indicator dropped from 112.7 to 111.7.

Eurozone PMI manufacturing finalized at 55.5, output came to a near standstill

Eurozone PMI Manufacturing was finalized at 55.5 in April, a 15-month low, and down from March’s 55.5. Output index was finalized at 50.7, a 22-month low, down from March’s 53.1.

Looking at some member states, PMI manufacturing of the Netherlands rose to 2-month high at 59.9. France rose to 2-month high at 55.. Austria dropped to 15-month low at 57.9. Germany dropped to 20-month low at 54.6. Italy dropped to 16-month low at 54.5. Spain dropped to 14-month low at 53.3.

Chris Williamson, Chief Business Economist at S&P Global said: “Manufacturing output came to a near standstill across the eurozone in April, with production merely edging higher at the slowest rate since June 2020. Companies not only reported that ongoing problems with component shortages were aggravated by the Ukraine war and new lockdowns in China, but that rising prices and growing uncertainty about the economic outlook were also hitting demand.”

Germany PMI Manufacturing was finalized at 54.6 in April, a 20-month low, down from March’s 56.9. S&P Global said supply disruption and weaker demand weighed on output. Soaring costs drove unprecedented rise in prices charged. Goods producers remained pessimistic about the outlook.

France PMI Manufacturing was finalized at 55.7 in April, up from March’s 54.7. S&P Global said manufacturing output growth was constrained by war in Ukraine. There were reports of automotive sector weakness, while supply issues persisted. Output price inflation accelerated to series high.

Swiss SECO consumer climate dropped to -27 in Q2, marked weakening of sentiment

Swiss SECO consumer climate dropped sharply from -4 to -27 in Q2, well below expectation of -15. That’s was the biggest decline since the onset of the pandemic, and the reading was below long-term average of -5. Looking at some details, the expected economic development index dropped from 21 to -31. Expected financial situation dropped from -3 to -25. Major purchases index dropped further from -23 to -31.

SECO said: “The survey from April shows a marked weakening of consumer sentiment. In particular, consumers’ outlook for the general economic situation has turned far more pessimistic. Households are feeling the strain as prices continue to rise. Meanwhile, the situation on the labour market is again being viewed as more positive. ”

Japan PMI manufacturing finalized at 53.5, war and China weigh on confidence

Japan PMI Manufacturing was finalized at 53.5 in April, down from March’s 54.1. Au Jibun Bank said growth in output levels was unchanged as new orders expansion slowed. Factory gate charges were in record rise amid accelerating input prices. Business optimism dipped to lowest since July 2020.

Usamah Bhatti, Economist at S&P Global, said: “Domestic demand was a key driver of growth… but the reintroduction of lockdown restrictions in China hindered international demand. These measures coupled with the fallout from war in Ukraine continued to disrupt supply chains across the sector.

“Delivery delays and price rises remained a dampener… Sharply rising cost burdens pushed Japanese manufacturers to raise selling prices to the greatest extent in the survey history.

“Though still optimistic, Japanese goods producers were increasingly wary of the continued impact of price and supply pressures, and also the impact of the war and extended lockdowns in China. As a result, confidence dipped to the weakest since July 2020.”

Japan consumer confidence ticked up to 33.0 in Apr

Japan consumer confidence index rose slightly by 0.2 pts to 33.0 in April, missed expectation of 33.9. Overall livelihood dropped -0.1 to 31.2. Income growth dropped -0.6 to 36.8. Employment rose 1.3 to 36.1. Willingness to buy durable goods dropped -0.1 to 27.7.

93.7% of respondents expect prices to go up a year ahead, up 0.9%. 2.7% expect prices to stay the same, down -0.8%. 2.1% expect prices to go down, up 0.1%.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2765; (P) 1.2813; (R1) 1.2907; More…

USD/CAD’s rally from 1.2401 resumes by breaking through 1.2879 temporary top. Intraday bias is back on the upside for 1.3022 fibonacci level next. Decisive break there will carry larger bullish implications. In any case, outlook will stay cautiously bullish as long as 1.2717 support intact, in case of another retreat.

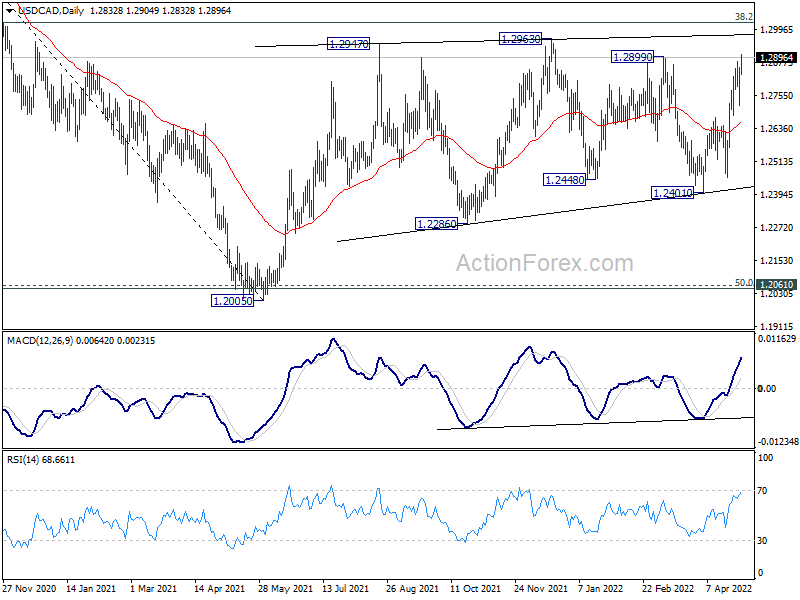

In the bigger picture, focus stays on 38.2% retracement of 1.4667 (2020 high) to 1.2005 (2021 low) at 1.3022. Sustained break there should confirm that the down trend from 1.4667 has completed after defending 1.2061 long term cluster support. Further rise would then be seen towards 61.8% retracement at 1.3650. However, rejection by 1.3022 will maintain medium term bearishness. Break of 1.2005 will resume the down trend from 1.4667 and that carries larger bearish implications too.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Mfg Index Apr | 58.5 | 55.7 | ||

| 00:30 | JPY | Manufacturing PMI Apr F | 53.5 | 53.4 | 53.4 | |

| 05:00 | JPY | Consumer Confidence Index Apr | 33 | 33.9 | 32.8 | |

| 06:00 | EUR | Germany Retail Sales M/M Mar | -0.10% | 0.30% | 0.30% | |

| 07:00 | CHF | SECO Consumer Climate Q2 | -27 | -15 | -4 | |

| 07:30 | CHF | Manufacturing PMI Apr | 62.5 | 60.2 | 64 | |

| 07:45 | EUR | Italy Manufacturing PMI Apr | 54.5 | 55.1 | 55.8 | |

| 07:50 | EUR | France Manufacturing PMI Apr F | 55.7 | 55.4 | 55.4 | |

| 07:55 | EUR | Germany Manufacturing PMI Apr F | 54.6 | 54.1 | 54.1 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Apr F | 55.5 | 55.3 | 55.3 | |

| 09:00 | EUR | Eurozone Economic Sentiment Indicator Apr | 105 | 108 | 108.5 | 106.7 |

| 09:00 | EUR | Eurozone Services Sentiment Apr | 13.5 | 14.2 | 14.4 | 13.6 |

| 09:00 | EUR | Eurozone Industrial Confidence Apr | 7.9 | 9.5 | 10.4 | 9.0 |

| 09:00 | EUR | Eurozone Consumer Confidence Apr F | -22.0 | -16.9 | -16.9 | -21.6 |

| 13:30 | CAD | Manufacturing PMI Apr | 57.9 | 58.9 | ||

| 13:45 | USD | Manufacturing PMI Apr F | 59.7 | 59.7 | ||

| 14:00 | USD | ISM Manufacturing PMI Apr | 57.5 | 57.1 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid Apr | 88.2 | 87.1 | ||

| 14:00 | USD | ISM Manufacturing Employment Index Apr | 56.3 | |||

| 14:00 | USD | Construction Spending M/M Mar | 0.80% | 0.50% |

{kind=link}