Funds appear to be flowing out of Euro and Swiss Franc, in relatively quiet trading today. Some focuses are on the Euro-denominated bonds issued by Credit Suisse, which dropped to record lows. Investors are concerned about the Swiss bank’s restructuring program, due to be announced later in the month. Euro and Franc are the worst performers, followed by Yen, while Dollar is mixed. Sterling is trying to rebound after UK Finance Minister Kwasi Kwarteng confirmed to abandons plan to scrap 45p top rate of income tax. But Aussie and Kiwi are stronger ahead of rate hikes by RBA (Tue) and RBNZ (Wed).

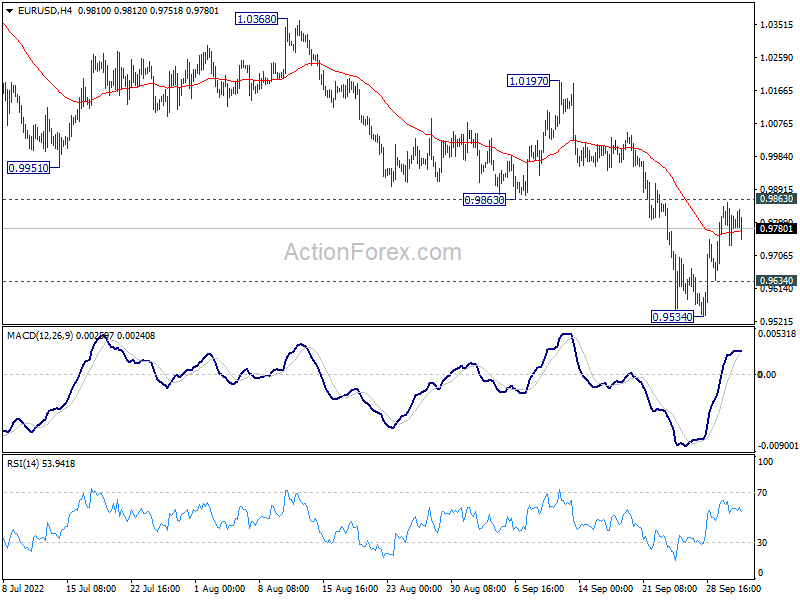

Technically, EUR/GBP is breaking through 0.8720 resistance turned support to indicate near term bearish reversal. But the question is whether it’s translated into more upside in GBP/USD, downside in EUR/USD, or both. For now, outlook in EUR/USD isn’t bullish as long as 0.9863 support turned resistance holds. Break of 0.9634 minor support will bring retest of 0.9534 low.

In Europe, at the time of writing, FTSE is down -0.34%. DAX is down -0.07%. CAC is down -0.27%. Germany 10-year yield is down -0.134 at 1.977. Earlier in Asia, Nikkei rose 1.07%. Hong Kong HSI dropped -0.83%. China was on holiday. Singapore Strait Times dropped -0.74%. Japan 10-year JGB yield dropped -0.0079 to 0.244.

UK PMI manufacturing finalized at 48.4, goods producing sector a drag on GDP

UK PMI Manufacturing was finalized at 48.4 in September, up from August’s 47.3. S&P Global said output and new orders fell further. New export business declined. Input costs and output price inflation accelerated.

Rob Dobson, Director at S&P Global Market Intelligence, said: “The downturn in UK manufacturing continued at the end of the third quarter, meaning the goods producing sector looks set to have acted as a drag on GDP. Manufacturers have once again cut back production as new order intakes declined for the fourth successive month.

“Factories are reporting tough market conditions both at home and abroad. Disappointingly, exports continue to fall despite the more competitive exchange rate.

“There was also less positive news on the price front, with rates of inflation in input costs and selling prices both picking up in September, linked in part to import costs rising due to the weaker pound.

Eurozone PMI manufacturing finalized at 48.4, ugly combination of recession and inflation

Eurozone PMI Manufacturing was finalized at 48.4 in September, down from August’s 49.6. That’s also a 27-month low. Looking at some member states, France PMI Manufacturing was finalized at 47.7, a 28-month low. Germany was finalized at 47.8, a 27-month low. Greece (49.7), the Netherlands (49.0), Spain (49.0), Austria (48.8) and Italy (48.3) were all in contraction, while Ireland (51.5) was in expansion.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said: “The ugly combination of a manufacturing sector in recession and rising inflationary pressures will add further to concerns about the outlook for the eurozone economy… Excluding the initial pandemic lockdowns, eurozone manufacturers have not seen a collapse of demand and production on this scale since the height of the global financial crisis in early-2009.

Swiss CPI unexpectedly slowed to 3.3% yoy

Swiss CPI dropped -0.2% mom in September, below expectation of 0.1% mom. The decrease of 0.2% compared with the previous month can be explained by several factors including falling prices for fuels, heating oil, hotels and supplementary accommodation. In contrast, prices for clothing and footwear increased.

Comparing with the same month a year ago, CPI slowed to 3.3% yoy, down from 3.5% yoy, below expectation of 3.5% yoy. Core CPI (excluding fresh and seasonal products, energy and fuel) was flat mom, up 2.0% yoy (unchanged from August). Domestic product prices rose 1.8% yoy (unchanged from August). Imported product prices rose 7.8% yoy (down from 8.6% yoy in August).

BoJ: Upside risks of inflation to be examined humbly and without any preconceptions

In the summary of opinions of BoJ’s September 21-22 meeting, it’s noted that risks of “consumer prices deviating significantly upward from the baseline scenario, including the impact of foreign exchange rates, needs to be examined humbly and without any preconceptions.”

But while a “certain degree of upside risk to prices” exists, there is a “long way to go” to achieve 2% inflation target in a “sustainable and stable manner”. Output gap has been “negative”, unemployment rate and active active job openings-to-applicants ratio “have not returned to pre-pandemic levels”. Surge in energy and raw material prices has brought about an “outflow of income” from Japan. It is “appropriate” to continue with the current monetary easing.

Regarding exchange rate, one opinion noted that ” further depreciation of the yen is partly due to differences in the direction of monetary policy between Japan and other economies.. the Bank needs to carefully explain the significance of continuing with the current monetary easing.”

Japan business outlook deteriorated in Q3

Japan Tankan large manufacturing index dropped from 9 to 8, below expectation of 11. That’s the third straight quarter of deterioration. Non-manufacturing index improve slightly from 13 to 14, above expectation of 13, and rise for the second straight quarter.

Large manufacturing outlook dropped from 10 to 9, below expectation of 11. Non-manufacturing outlook also deteriorated from 13 to 11, below expectation of 15.

Nevertheless, large companies are expected to increase capital expenditure by 21.5% in the current fiscal year ending March 2023, above expectation of 18.8%.

Meanwhile, companies expect inflation to hit 2.6% a year from now, and 2.1% three years ahead. Five years ahead inflation is also projected at 2.0%, highest since data became available in 2014.

Japan PMI manufacturing finalized at 50.8, weakness even turned worse

Japan PMI Manufacturing was finalized at 50.8 in September, down from August’s 51.5. S&P Global said high inflation and subdued global market conditions weight on order books. Output fell at sharpest pace in a year, while input buying reduced. Weak yen drove inflationary pressures higher.

Joe Hayes,, Senior Economist at S&P Global Market Intelligence, said: “Weakness in Japan’s manufacturing sector persisted in September and even turned worse. New orders fell at their sharpest rate in two years – high inflation is eroding client purchasing power, while slowing global economic growth is hurting exports. Weakness in the yen is doing little to bolster export demand either and instead is pushing imported inflation up drastically and drove domestic price pressures up even further.”

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1052; (P) 1.1143; (R1) 1.1260; More…

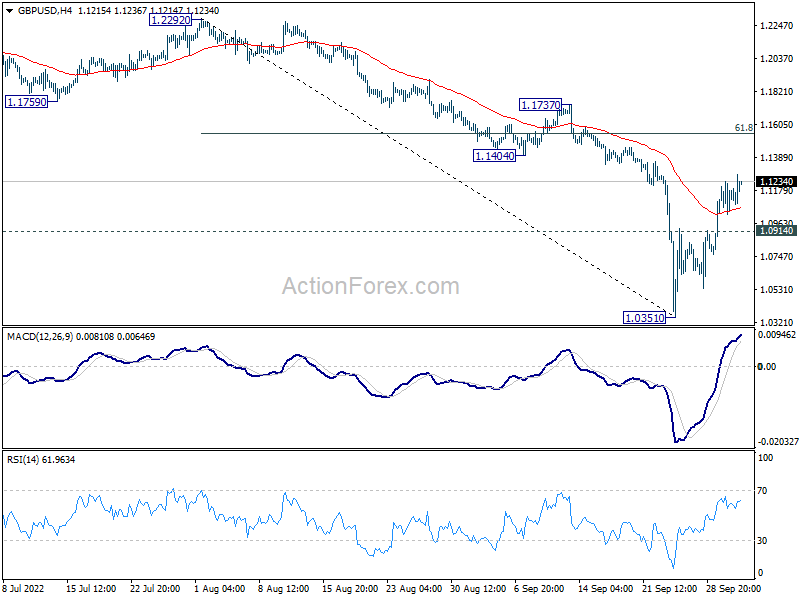

GBP/USD’s rebound from 1.0351 is in progress and intraday bias stays on the upside, Further rally would be seen to 61.8% retracement of 1.2292 to 1.0351 at 1.1551. On the downside, break of 1.0914 minor support will indicate that the rebound is over, and bring retest of 1.0351 low.

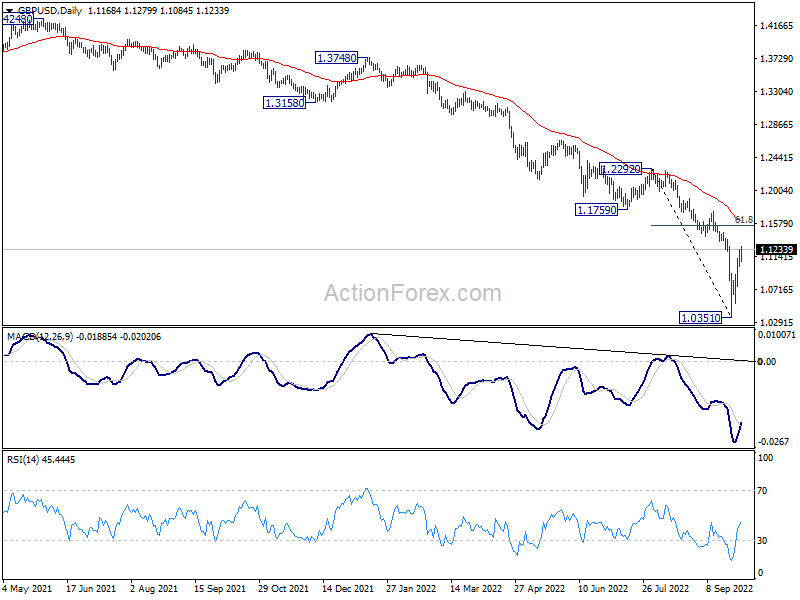

In the bigger picture, fall from 1.4248 (2018 high) is resuming long term down trend from 2.1161 (2007 high). Next target is 100% projection of 2.1161 to 1.3503 from 1.7190 at 0.9532. There is no scope of a medium term rebound as long as 1.1759 support turned resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Tankan Large Manufacturing Index Q3 | 8 | 11 | 9 | |

| 23:50 | JPY | Tankan Non-Manufacturing Index Q3 | 14 | 13 | 13 | |

| 23:50 | JPY | Tankan Large Manufacturing Outlook Q3 | 9 | 11 | 10 | |

| 23:50 | JPY | Tankan Non-Manufacturing Outlook Q3 | 11 | 15 | 13 | |

| 23:50 | JPY | Tankan Large All Industry Capex Q3 | 21.50% | 18.80% | 18.60% | |

| 00:00 | AUD | TD Securities Inflation M/M Sep | 0.50% | -0.50% | ||

| 00:30 | JPY | Manufacturing PMI Sep F | 50.8 | 51 | 51 | |

| 06:30 | CHF | CPI M/M Sep | -0.20% | 0.10% | 0.30% | |

| 06:30 | CHF | CPI Y/Y Sep | 3.30% | 3.50% | 3.50% | |

| 07:30 | CHF | SVME PMI Sep | 57.1 | 54.6 | 56.4 | |

| 07:45 | EUR | Italy Manufacturing PMI Sep | 48.3 | 47.5 | 48 | |

| 07:50 | EUR | France Manufacturing PMI Sep F | 47.7 | 47.8 | 47.8 | |

| 07:55 | EUR | Germany Manufacturing PMI Sep F | 47.8 | 48.3 | 48.3 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Sep F | 48.4 | 48.5 | 48.5 | |

| 08:30 | GBP | Manufacturing PMI Sep | 48.4 | 48.5 | 48.5 | |

| 13:30 | CAD | Manufacturing PMI Sep | 50.6 | 48.7 | ||

| 13:45 | USD | Manufacturing PMI Sep F | 51.8 | 51.8 | ||

| 14:00 | USD | ISM Manufacturing PMI Sep | 52.3 | 52.8 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid Sep | 51.8 | 52.5 | ||

| 14:00 | USD | ISM Manufacturing Employment Index Sep | 54.2 | |||

| 14:00 | USD | Construction Spending M/M Aug | -0.30% | -0.40% |

{kind=link}