Dollar continues to trade mildly higher into US session as consolidations extend. Upside momentum in the greenback is very weak so far. But such consolidations could now extend for a further while. Aussie and Loonie are the next firmest. Yen is currently the worst performer, followed by Kiwi and Euro, and Sterling is mixed. Still, most major pairs and crosses are bounded inside Friday’s range. With an empty economic calendar in the US and Canada, traders might need to wait until the coming Asian session before seeing any meaningful moves.

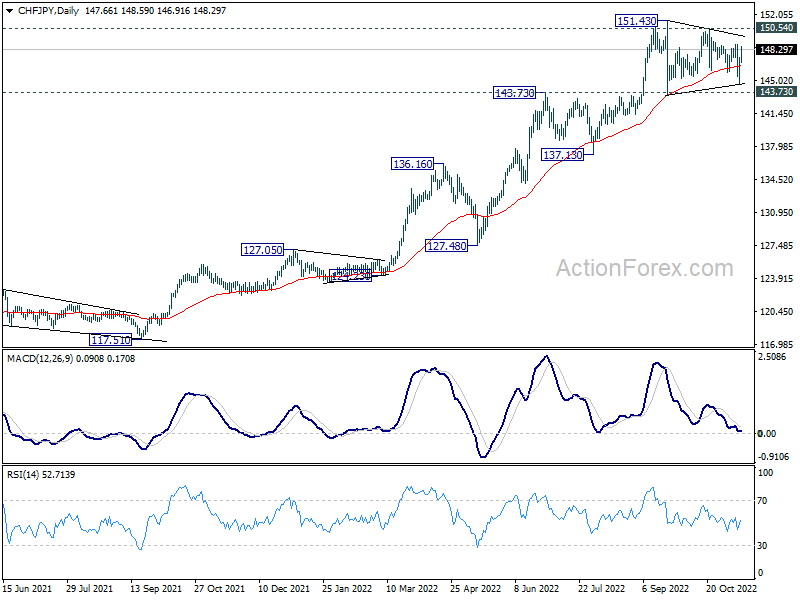

Technically, CHF/JPY’s strong rebound today suggests that 143.73 resistance turned support is safe for now. The development keeps near term outlook bullish for up trend resumption at later stage. Break of 150.54 resistance will suggest that upside momentum is building up through 151.43 high. If that happens, EUR/JPY and GBP/JPY would likely approach 148.38 and 172.11 highs respectively.

In Europe, at the time of writing, DAX is up 0.40%. CAC is up 0.34%. CAC is up 0.35%. Germany 10-year yield is down -0.036 at 2.122. Earlier in Asia, Nikkei dropped -1.06%. Hong Kong HSI rose 1.70%. China Shanghai SSE dropped -0.13%. Singapore Strait Times rose 1.01%. Japan 10-year JGB yield rose 0.0114 to 0.243.

ECB Panetta: Aggressive tightening is not advisable now

ECB Executive Board member Fabio Panetta said in a speech, “after the progress we have already done in adjusting our policy stance, an aggressive tightening is not advisable, for two main reasons.”

First, “current macroeconomic policies should be designed to avoid unnecessarily heightening the risk that the increasingly likely contraction in coming months becomes a severe and protracted one, which would scar the economy… it also requires that monetary policy does not ignore the risks of overtightening,” he said”.

Second, “even in the face of lasting consequences of supply shocks on potential output, the implications for the output gap, inflation dynamics and optimal policy calibration can only be derived over time. And this reinforces the case that, for as long as inflation expectations remain anchored, monetary policy should adjust but not overreact”.

Eurozone industrial production rose 0.9% mom, EU up 0.9% mom

Eurozone industrial production rose 0.9% mom in September, well above expectation of 0.1% mom. Production of non-durable consumer goods rose by 3.6% and capital goods by 1.5%, while production of intermediate goods as well as durable consumer goods fell by -0.9% and energy by -1.1%.

EU industrial production also rose 0.9% mom. Among Member States for which data are available, the highest monthly increases were registered in Ireland (+11.9%), Belgium (+7.1%) as well as in Hungary and the Netherlands (both +1.6%). The largest decreases were observed in Lithuania (-8.2%), Greece (-4.5%) and Estonia (-3.6%).

BoJ Kuroda: Should continue with monetary easing

BoJ Governor Haruhiko Kuroda said in a speech that Japan’s situation “differs” from both the US and the Eurozone. The country is still “on its way to recovery”. Output gap has “remained in negative territory”, but projected to “turn positive” as some point in H2 of this fiscal year. Inflation rate “has not risen from the demand side”. Current rise in inflation was “led by rise in import prices”, and the rate is projected to decline back to below 2% from fiscal 2023.

He reiterated that BoJ “deems that it should continue with monetary easing and thereby firmly support economic activity”. By doing so, “it aims to provide a favorable environment for firms to raise wages and to achieve the price stability target in a sustainable and stable manner, accompanied by wage increases.”

Regarding exchange rates, Kuroda said the “abnormally one-sided, sharp yen weakening appears to have paused, thanks partly to government’s FX intervention.” He emphasized it is “important for forex rates to move stably reflecting economic fundamentals”.

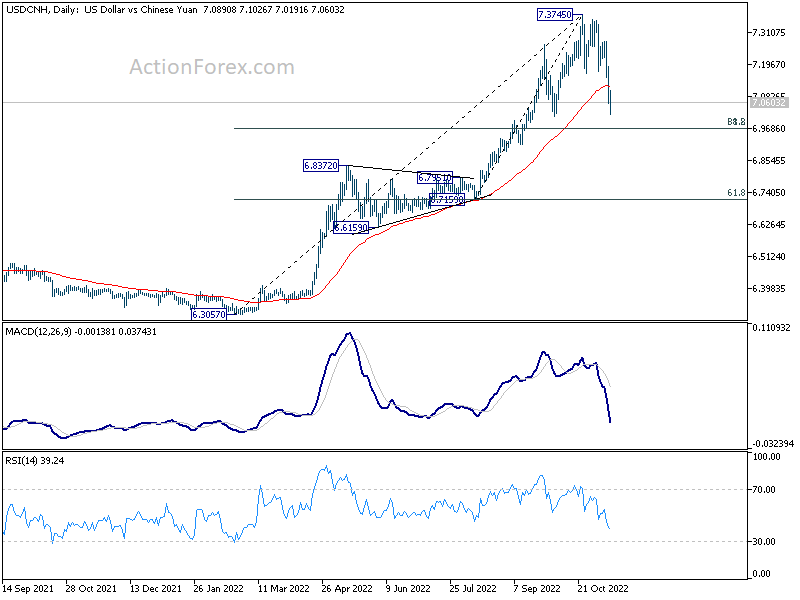

USD/CNH falling towards 7.000, but shouldn’t break there for long

Chinese Yuan surges today and hits the highest level against Dollar since early October. The rally was fueled by growing optimism that China is going to relax is strict zero-COVID policy, even as outbreaks worsen with highest infections in six months. At the same time, of course, decline in USD/CNH happened with global selloff in Dollar, after last week’s lower than expected CPI data solidified the case for Fed to start to slow its tightening pace in December.

Technically speaking, there is room for more pull back in USD/CNH, towards 7.000 psychological level. However, there’s an important cluster support, with 61.8% retracement of 6.7159 to 7.3475 at 6.9675 and 38.2% retracement of 6.3057 to 7.3745 at 6.9662 just nearby. Downside should be contained by this 6.9662/75 support zone to bring rebound, unless there are some fundamental changes, in China, or the US, or their diplomatic relations, or any combinations of these factors.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 137.34; (P) 139.91; (R1) 141.35; More…

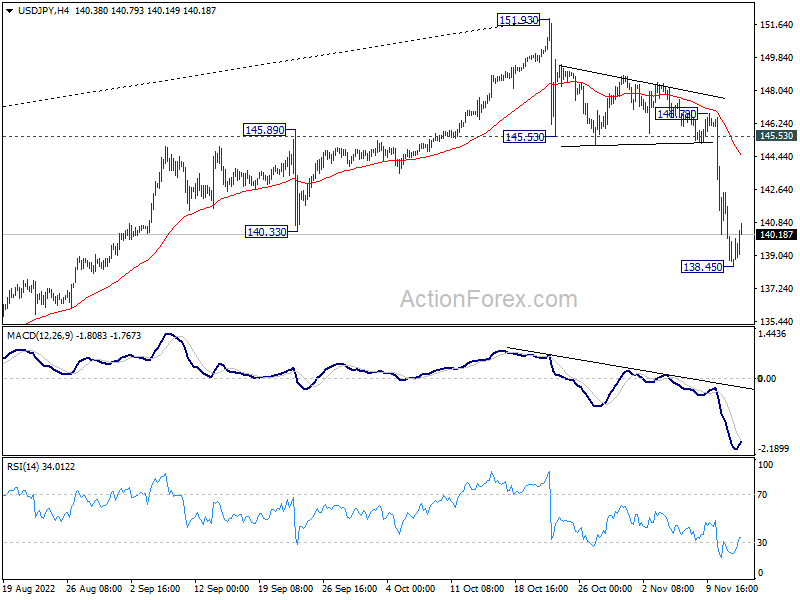

Intraday bias in USD/JPY Is turned neutral with current recovery, and some consolidations could be seen. But upside should be limited below 145.54 support turned resistance and bring another fall. Break of 138.45 will resume the decline from 151.93, as a correction to the larger up trend, towards 133.07 fibonacci level.

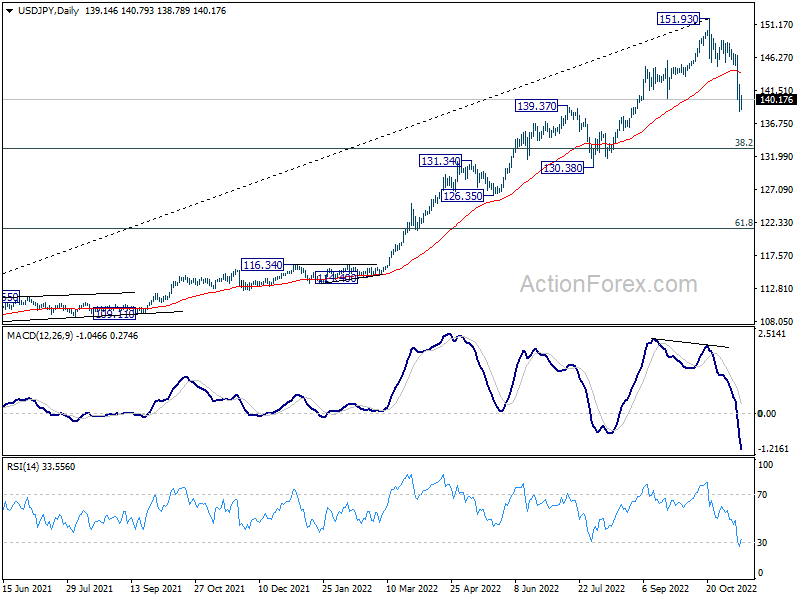

In the bigger picture, a medium term top should be formed at 151.93. Fall from there is correcting larger up trend from 102.58. It’s too early to call for bearish trend reversal. But even as a corrective move, such decline should target 38.2% retracement of 102.58 to 151.93 at 133.07, or further to 55 week EMA (now at 130.58).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 07:30 | CHF | Producer and Import Prices M/M Oct | 0.00% | 0.20% | 0.20% | |

| 07:30 | CHF | Producer and Import Prices Y/Y Oct | 4.90% | 5.40% | ||

| 10:00 | EUR | Eurozone Industrial Production M/M Sep | 0.90% | 0.10% | 1.50% | 2.00% |

{kind=link}