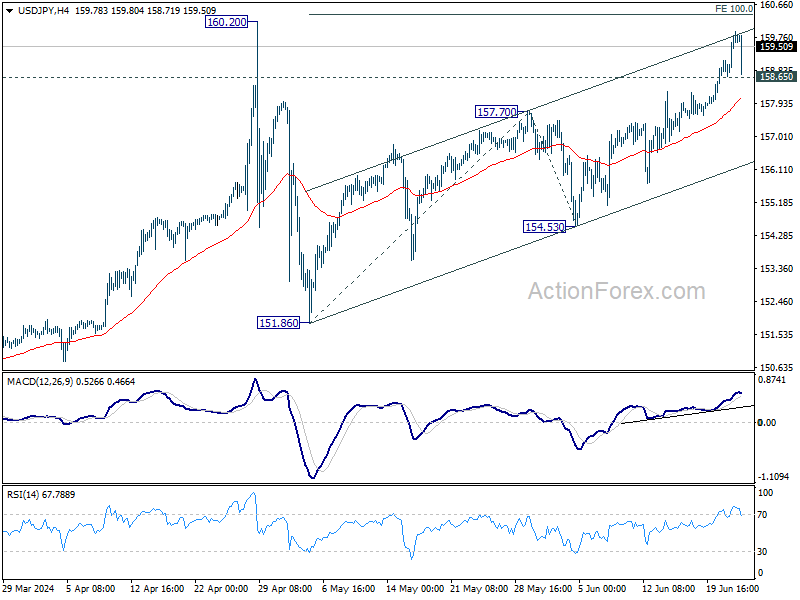

USD/JPY attempt to break through the critical 160 level was unsuccessful for, as Yen recovered during a relatively quiet European session today. Although Yen surged briefly, there was no sustained selloff below the 159 mark against the greenback. The scale of the movement makes it challenging to determine if Japan intervened in the market. This could be due to a cautious probe by the authorities, actions by institutional traders, or simply heightened market nerves. Yen will remain under close scrutiny, especially given the lack of significant economic data from the US until tomorrow’s European session.

Euro is currently the best performer today, with notable bounce against Sterling. However, the rebound in the common currency isn’t strong enough to signal a reversal of the recent downtrend yet. According to the latest Ipsos poll released over the weekend, the far-right National Rally continues to lead the first round of the parliamentary elections with 35.5% of the vote, followed by the left-wing New Popular Front with 29.5%. Should these poll results be reflected in the elections, Euro could face another wave of selling pressure.

Across the broader currency markets, Euro and Yen are the strongest performers today, followed by the Sterling. In contrast, New Zealand Dollar and Australian Dollar are the weakest, alongside Dollar, with Canadian Dollar also lagging. The Swiss Franc is positioned in the middle of the performance spectrum.

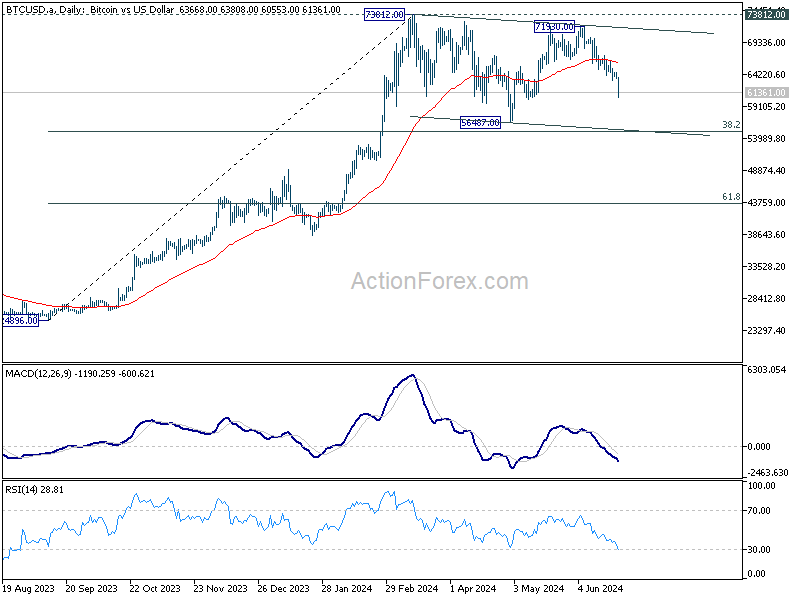

Technically, Bitcoin is now extending the corrective pattern from 73812, with fall from 71930 as the third leg. Deeper decline could be seen in the near term to 56487 support. Strong downside should be contained by 38.2% retracement of 24896 to 73812 at 55126 to bring rebound. Meanwhile, sustained break of 55 D EMA (now at 66019) will suggest that Bitcoin is ready for another test on 73812 again.

In Europe, at the time of writing, FTSE is up 0.43%. DAX is up 0.54%. CAC is up 0.83%. UK 10-year yield is up 0.001 at 4.089. Germany 10-year yield is up 0.015 at 2.427. Earlier in Asia, Nikkei rose 0.54%. Hong Kong HSI fell -0.00%. China Shanghai SSE fell -1.17%. Singapore Strait Times rose 0.25%. Japan 10-year JGB yield rose 0.0138 to 0.991.

German Ifo falls to 88.6, struggling to overcome stagnation

German Ifo Business Climate fell from 89.3 to 88.6 in June, below expectation of 89.7. Current Assessment index was unchanged at 88.3, below expectation of 88.4. Expectations Index fell from 90.3 to 89.0, below expectation of 91.0.

Ifo said that the German economy is “having difficulty overcoming stagnation”.

By sector, manufacturing fell from -6.5 to -9.2. Services rose from 1.8 to 4.2. Trade fell from -17. to -23.5. Construction ticked up from -25.6 to -25.0.

BoJ deliberates on rate hikes, Yen depreciation, and JGB purchase adjustments

During Monetary Policy Meeting on June 13-14, BoJ board discussed the need for adjustments in response to rising inflation risks. One key opinion indicated that if April Outlook Report’s economic and inflation forecasts are realized, BoJ will raise the policy interest rate and adjust monetary accommodation.

Another member warned that prices could “deviate upward” from the baseline scenario if recent cost increases are passed on to consumers, suggesting a need for further policy adjustments from a “risk management” perspective. It’s also highlighted the growing “upside risks” to prices, with one member stating these risks have affected consumer sentiment and that the policy interest rate should be raised “not too late” if appropriate.

The impact of Yen’s depreciation was also discussed, with an opinion suggesting an “upward revision” to the inflation outlook, warranting a higher risk-neutral policy interest rate. Some members emphasized the importance of basing monetary policy on the “overall picture of developments in economic activity and prices,” rather than short-term foreign exchange fluctuations. They stressed that policy should be informed by trends in prices and wage developments.

Regarding asset purchases, one opinion recommended reducing the purchase amount of Japanese government bonds to allow long-term interest rates to form more freely in financial markets. This reduction should be “sizeable” and “predictable,” while ensuring flexibility to maintain stability in JGB market.

New Zealand’s goods exports reach record high in may, trade surplus exceeds expectations

New Zealand’s goods exports rose by 2.9% yoy to NZD 7.2B in May, marking the first time that monthly exports have surpassed the NZD 7B mark. Goods imports also saw a slight increase, rising by 0.6% yoy to NZD 7.0B. This resulted in a trade surplus of NZD 204m, exceeding the expected NZD 155m.

Breaking down the top monthly export movements by country, New Zealand saw mixed results. Exports to China fell by -12% yoy, and exports to Australia dropped by -3.8% yoy. In contrast, exports to the US surged by 33% yoy, while exports to the EU and Japan rose by 2.8% yoy and 12% yoy, respectively.

On the import side, imports from China increased by 2.6% yoy, while imports from the EU decreased by -1.8% yoy. Imports from Australia -4.7% yoy, whereas imports from the US and South Korea rose by 1.6% yoy and 5.8% yoy, respectively.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 159.02; (P) 159.44; (R1) 160.22; More…

Despite the deep but brief retreat, intraday bias in USD/JPY stays mildly on the upside with 158.65 minor support intact. Current rally should target 160.20 high, or possibly to 100% projection of 151.86 to 157.70 from 154.53 at 160.37. Upside could be limited there, at least on first attempt. On the downside, below 158.24 minor support will turn intraday bias neutral first. However, decisive break of 160.37 will pave the way to 161.8% projection at 163.97.

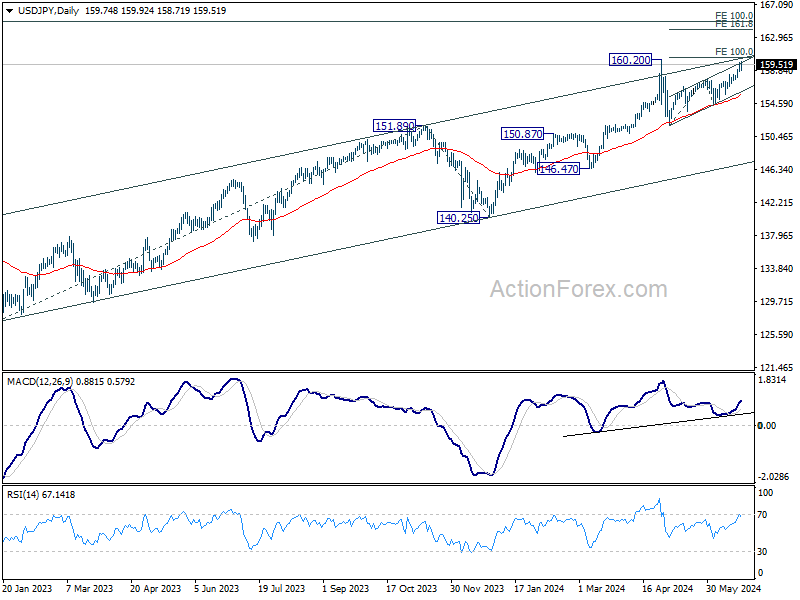

In the bigger picture, there is no sign of long term trend reversal yet. Further rally is expected as long as 150.87 resistance turned support holds. Decisive break of 160.02 will target 100% projection of 127.20 to 151.89 from 140.25 at 164.94.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) May | 204M | 155M | 91M | -3M |

| 23:50 | JPY | BoJ Summary of Opinions | ||||

| 08:00 | EUR | Germany IFO Business Climate Jun | 88.6 | 89.7 | 89.3 | |

| 08:00 | EUR | Germany IFO Current Assessment Jun | 88.3 | 88.4 | 88.3 | |

| 08:00 | EUR | Germany IFO Expectations Jun | 89 | 91 | 90.4 | 90.3 |

{kind=link}