New Zealand dollar is the star performer today as markets respond very positively to the appointment of the new RBNZ governor. Strength in the Kiwi also took Aussie generally higher. Meanwhile, Dollar is paring recent gains against all but Sterling and Loonie. Dollar traders are cautiously adjusting their positions ahead of the FOMC rate hike and new forecasts on Wednesday. But it’s Sterling who’s the weakest and impact from Brexit breakthrough faded. More volatility is anticipated ahead with Fed, ECB, BoE and SNB meeting this week, in addition to heavy weight data like US and UK CPI.

Kiwi surges on RBNZ Governor appointment

New Zealand Dollar responds very positively today after Finance Minister Grant Robertson named Superannuation Fund chief Adrian Orr as the next RBNZ Governor, beginning March 27. Orr was also a former RBNZ Deputy Governor and chief economist. Economist are skeptical on the Labour led government’s idea of reforming RBNZ and transit it to Fed-style dual mandate. That is, price stability and full employment would both be the central bank’s targets. And some worried that it would make it much harder for RBNZ to raise interest rates. However, Orr’s employment, with his background, provides some certainty that the reform and transitions will be practical and realistic, rather pure political ideology driven.

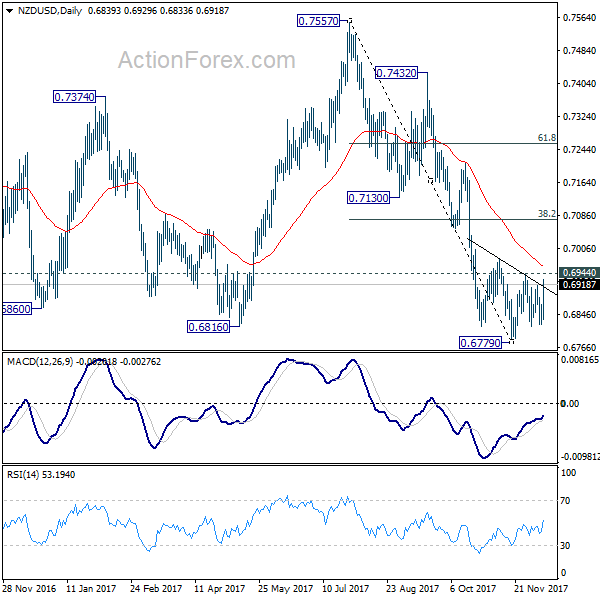

NZD/USD breached 0.6816 key support to 0.6779 back in November but quickly recovered. Current development argues that it could be completing a head and shoulder bottom pattern. With today’s rebound, focus is back on 0.6944 resistance. Break there should at least bring rebound to 38.2% retracement of 0.7557 to 0.6779 at 0.7076.

ECB Nouy: Banks M&A to accelerate

ECB Supervisory head Daniele Nouy said in a newspaper interview that merger and acquisitions in the Eurozone banking sector will acceleration ahead. She said that "with growth returning and with the huge amount of work that is being done in relation to non-performing loans, we are going to see a number of mergers taking place within countries and across borders." Meanwhile, ECB’s plan on bad loans may be delayed after hearing the negative feedback from the industry. But she emphasized that "it doesn’t change much whether it happens on say 1 January, 1 April or 1 June,"

David Davis stirring things up after last week’s Brexit deal

Just two days UK Prime Minister Theresa eased her nerve with the Brexit deal with EU, Brexit Secretary David Davis seemed to be stirring up the issues again. Davis told BBC that UK won’t be paying the divorce bill if there is no trade deal. He said "it is conditional on an outcome. It is conditional on getting an implementation period, it is conditional on a trade outcome." This is the exact opposite of what Chancellor Philip Hammond told a parliamentary committee last week. Hammond did say that "nothing is agreed until everything is agreed in this negotiation." But he also said "I find it inconceivable that we as a nation would be walking away from an obligation that we recognized as an obligation." Hammond also emphasized that "that is not a credible scenario. That is not the kind of country we are. Frankly, it would not make us a credible partner for future international agreements."

Japan business conditions improved

In Japan, the Ministry of Finance’s business survey index (BSI) showed generally improved business conditions. For large corporations, with capital of JPY 1b or above), all industry business conditions improved to 6.2, up from 5.1. Large manufacturing conditions rose to 9.7, up from 9.4. Large non-manufacturing business conditions rose to 4.5, up from 2.9.

China CPI slowed, ease pressure for tightening

In China, CPI slowed to 1.7% yoy in November, down from 1.9% yoy and missed expectation of 1.8% yoy. PPI also dropped to 5.8% yoy, down from 6.9% yoy and met expectations. Slowing inflation is seen as welcomed by both the authority and the markets. The data suggests that China is in no rush to raise interest rate or tighten up monetary policies.

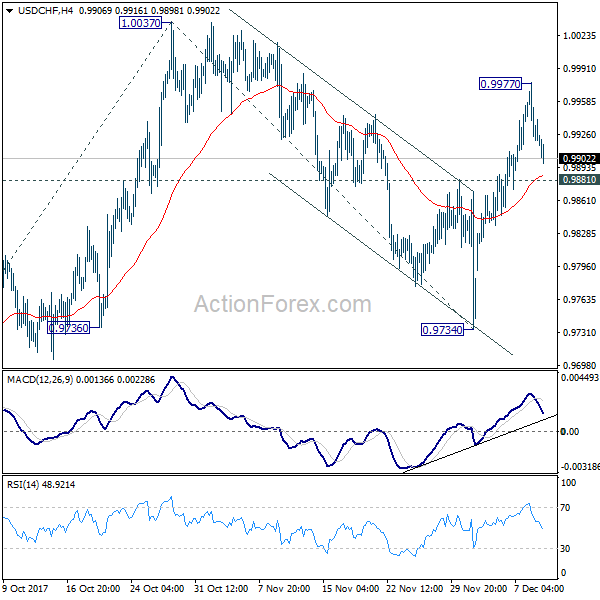

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9901; (P) 0.9939; (R1) 0.9958; More….

USD/CHF’s retreat from 0.9977 temporary top extends lower. But intraday bias remains neutral. We’d holding on to the view that correction from 1.0037 has completed at 0.9734 already. Also, rise from 0.9420 might be resuming. On the upside, above 0.9977 will target 1.0037 high first. Break will extend the rise from 0.9420 to 61.8% projection of 0.9420 to 0.9734 from 1.0047 at 1.0115 next. Nevertheless, firm break of 0.9881 support will dampen this immediate bullish case and turn bias to the downside for 0.9734 instead.

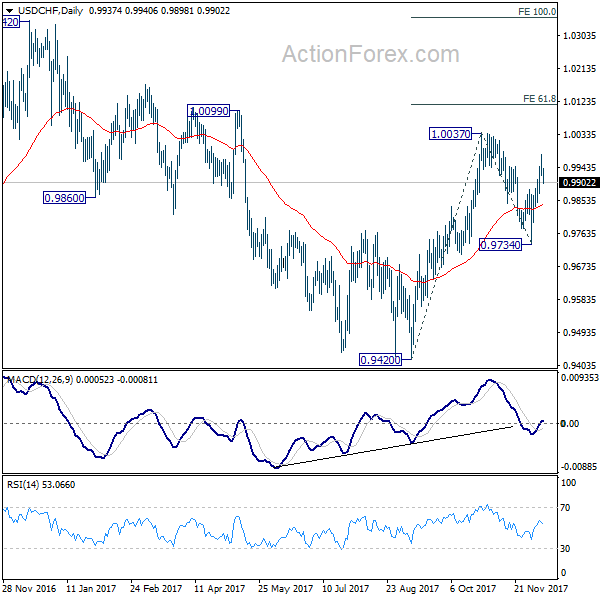

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don’t expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BSI Large All Industry Q/Q Q4 | 6.2 | 5.8 | 5.1 | |

| 23:50 | JPY | BSI Large Manufacturing Q/Q Q4 | 9.7 | 10 | 9.4 | |

| 23:50 | JPY | Japan Money Stock M2+CD Y/Y Nov | 4.00% | 4.10% | 4.10% | |

| 06:00 | JPY | Machine Tool Orders Y/Y Nov P | 46.90% | 49.80% |