{kind=link}

Sterling weakened sharply after the dovish read-through from the BoE’s rate hold. Although Bank Rate remained at 3.75%, the narrow 5–4 vote surprised markets and brought forward expectations for another cut. The close split highlighted a policy committee on a knife edge. With nearly half the MPC already favoring easing, investors quickly began to price a higher probability of a March move.

That perception was reinforced by Governor Andrew Bailey’s press conference. Bailey framed the outlook as “one of good news,” emphasizing that the disinflation process is firmly on track and progressing faster than the Bank anticipated late last year. Bailey said inflation is expected to average around 3% through the first quarter before dropping close to the 2% target in April and staying there. He stressed that this timeline is roughly a year earlier than the Bank expected in November.

Those comments strengthened the view that, barring negative surprises, doves could hold the upper hand at the March meeting. Markets interpreted the message as lowering the bar for additional easing rather than reaffirming caution.

The broader market backdrop also turned less supportive for risk assets. Risk sentiment soured as US equities opened lower, led by renewed losses in the NASDAQ, extending the ongoing tech rout. Adding to the unease, the Challenger, Gray & Christmas report showed job cuts surged by 108k in January—the highest January total since 2009 and the largest monthly reading since October 2025.

Whether this tech-led weakness bleeds into traditional sectors is now the key watchpoint. For now, markets are cautious rather than panicked, but the labor signal has raised eyebrows. Risk-off sentient is giving Yen and Swiss Franc a lift as markets enter into the US session.

Euro also held modest gains following the ECB’s hold. With policy seen as appropriately set and Euro appreciation already factored into the baseline, the ECB signaled no urgency to move.

On the other hand, sterling is the weakest performer after the BoE’s dovish tilt. Aussie and Kiwi also lag on risk-off sentiment. Yen and Swiss Franc outperform with Euro. Dollar and Loonie trade in the middle.

In Europe, at the time of writing, FTSE is down -0.93%. DAX is down -0.92%. CAC is down -0.55%. UK 10-year yield is up 0.007 at 4.564. Germany 10-year yield is up 0.006 at 2.870. Earlier in Asia, Nikkei fell -0.88%. Hong Kong HSI rose 0.14%. China Shanghai SSE fell -0.64%. Singapore Strait Times rose 0.21%. Japan 10-year JGB yield fell -0.023 to 2.228.

BoE holds at 3.75%, 5-4 vote highlights uneasy balance

The BoE left Bank Rate unchanged at 3.75%, in line with expectations, but the decision masked a much tighter internal debate than markets had anticipated. The 5–4 vote highlighted how finely balanced was the policy considerations as inflation cools but uncertainties persist.

Five members, including Governor Andrew Bailey, backed holding rates steady. Within this group, Megan Greene, Clare Lombardelli and Huw Pill argued that a “more prolonged period of restriction” may still be needed to prevent inflation from settling above target. Bailey and Catherine Mann were more confident that easing inflation would mitigate that risk, but judged that the “evidence was yet sufficient” enough to justify a cut.

On the other side, four members—Sarah Breeden, Swati Dhingra, Dave Ramsden and Alan Taylor—voted for an immediate 25bp reduction. They judged that risks of inflation persistence had “receded materially” and placed greater weight on weaker demand, arguing that policy remains overly restrictive.

Despite the hold, the overall message retained a clear easing bias. The statement reiterated that Bank Rate is “likely to be reduced further”, but emphasized that future decisions will be finely judged and data-dependent, leaving the timing and pace of cuts firmly open.

ECB holds at 2.00%, Euro strength already factored in

The ECB left the deposit rate unchanged at 2.00%, in line with expectations. The accompanying statement reaffirmed confidence that inflation should stabilize at the 2% target over the medium term and reiterated a data-dependent, meeting-by-meeting approach to policy decisions.

At the press conference, President Christine Lagarde emphasized that risks are “broadly balanced.” She acknowledged that some risks have increased while others have eased, leaving the Governing Council comfortable with current settings rather than inclined toward near-term action.

Lagarde outlined upside and downside inflation scenarios. On the upside, persistent energy price increases, more fragmented global supply chains, slower moderation in wage growth, and planned boosts in defence and infrastructure spending could lift inflation over the medium term.

On the downside, weaker external demand from tariffs, excess global capacity spilling into euro area imports, tighter financial conditions, and a stronger Euro could all dampen price pressures.

On the exchange rate, Lagarde noted that Euro appreciation could bring inflation down beyond current expectations. However, she added that the Euro’s gains against the dollar since March 2025 are already incorporated into the ECB’s baseline, while stressing that the Bank will continue to monitor pass-through effects closely.

Eurozone retail sales fall -0.5% mom in December as consumer weakness persists

Retail sales across the Eurozone fell -0.5% mom in December, a steeper decline than the expected -0.2% drop.

Detail shows a clear split between essentials and discretionary items. Food-related sales rose slightly by 0.1% mom, but non-food purchases excluding fuel slumped 1.2%, pointing to continued restraint on big-ticket and discretionary spending. Fuel sales were flat, offering little offset to the broader weakness.

The weakness was broad-based across the European Union, where retail sales also fell 0.5% on the month. Among reporting countries, Portugal (-3.1%), Sweden (-1.9%) and Denmark (-1.6%) recorded the largest declines, while Luxembourg (+7.0%), Slovakia (+3.1%) and Croatia (+1.8%) posted solid gains.

US initial jobless claims surge to 231k vs exp 210k

US initial jobless claims jumped 22k to 231k in the week ending January 31, well above expectation of 210k. Four-week moving average of initial claims rose 6k to 212k.

Continuing claims rose 25k to 1,844k in the week ending January 24. Four-week moving average of continuing claims fell -15k to 1851k, lowest since October 5, 2024.

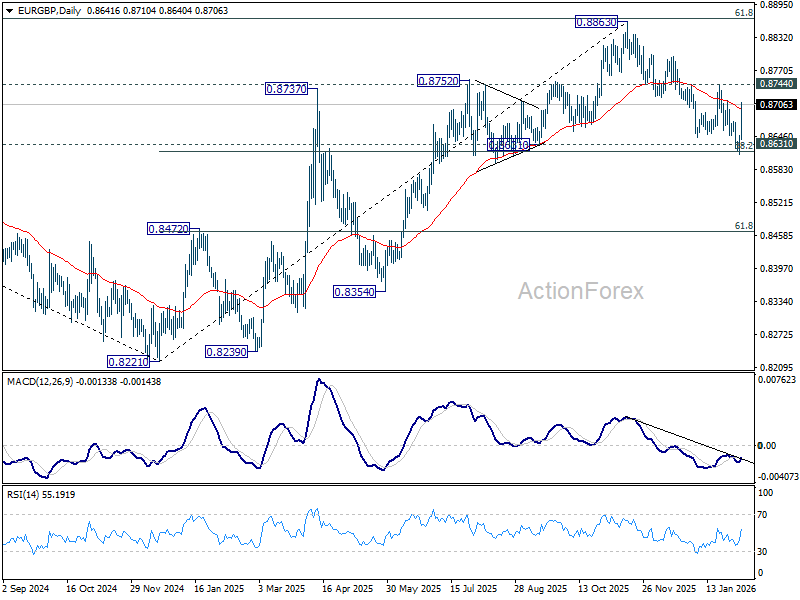

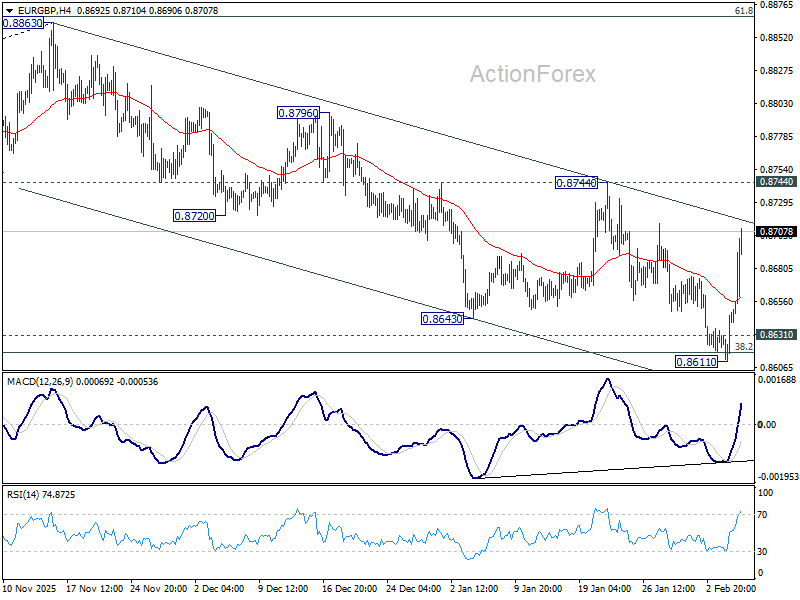

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8623; (P) 0.8636; (R1) 0.8660; More…

EUR/GBP’s rebound from 0.8611 extended higher today but stays below 0.8744 resistance. Intraday bias stays neutral first. On the upside, firm break of 0.8744 will argue that fall from 0.8863 has completed as a correction. Intraday bias will be back to the upside for retesting 0.8863, with prospect of resuming larger up trend. Nevertheless, on the downside, decisive break of 0.8631 cluster support (38.2% retracement of 0.8221 to 0.8663 at 0.8618) will carry larger bearish implications.

In the bigger picture, rise from 0.8221 medium term bottom (2024 low) is seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Sustained trading below 55 W EMA (now at 0.8625) should confirm that this corrective bounce has completed. In this case, deeper fall would be seen back to 0.8201/21 key support zone. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high). That should pave the way back to 0.9267.