Global markets are extending a powerful risk-on rally as expectations build that the Iran war may be nearing its end. European equities are posting strong gains, US futures point higher, and Dollar is sharply weaker across the board. The move reflects a clear shift in sentiment, with markets front-running a potential endgame and aggressively repositioning ahead of confirmation from US President Donald Trump’s scheduled address at 9 p.m. ET today.

This risk-on rally has been fueled by Trump’s indication that US forces could withdraw within “two to three weeks.” That guidance has been enough to trigger a repricing of geopolitical risk, but the sustainability of the move is far from assured. This is a rally built on anticipation, not confirmation, and markets are now entering a critical phase.

Conviction hinges on Trump’s address, which is widely seen as the decisive catalyst. Investors are not just looking for reassurance—they are looking for specifics. The difference between confirmation and ambiguity will determine whether the current rally extends or fades.

The first key element to watch is confirmation of a “de facto exit”. Language such as “mission accomplished” or “there’s nothing more to do” would strongly reinforce the endgame narrative. Trump has already downplayed the need for a formal deal, stating that Iran “doesn’t have to make a deal,” which suggests that a unilateral withdrawal is firmly on the table.

However, the biggest risk lies in the April 6 deadline. Any mention of a “final strike” on Iranian energy infrastructure would immediately flip sentiment. Markets view this as the nuclear option, with potential retaliation threatening regional energy facilities. Such a scenario would likely reverse the risk-on rally instantly.

Timing is the second critical factor. Trump’s previous guidance of “maybe two weeks, maybe three” has been enough to trigger positioning, but markets now need precision. A defined withdrawal schedule or phased exit plan would support the rally, while vague language, like “we’ll see what happens”, or delays would reinforce the view that the situation remains fluid.

The third and perhaps most important issue is the Strait of Hormuz. Markets are not just watching whether the US exits, but what happens after. If Trump signals that the US will no longer act as the “policeman” of the Strait, leaving allies to secure shipping lanes, then supply risks remain elevated even in a de-escalation scenario.

This is why oil is the ultimate signal. Brent has dipped notably today but remains above $100, indicating that markets are not fully convinced. A sustained break below $100 following Trump’s address would confirm that the oil shock is unwinding. Or even better, a deeper move below $96 structural support would reinforce a transition toward more normalized “Peace” conditions at around $80. Conversely, if oil holds firm or even rebounds above $110, it would signal lingering concerns about supply disruption and security risks. That would suggest that markets are still pricing uncertainty, even if the geopolitical narrative appears to be improving.

In short, markets are pricing the exit, not confirming it. The current rally reflects optimism around a potential endgame, but execution risk remains high. Whether this risk-on move extends or reverses will depend on whether Trump’s address delivers clarity—or reintroduces uncertainty into an already fragile setup.

In Europe, at the time of writing, FTSE is up 1.66%. DAX is up 2.34%. CAC is up 1.80%. UK 10-year yield is down -0.055 at 4.800. Germany 10-year yield is down -0.018 at 2.988. Earlier in Asia, Nikkei rose 5.24%. Hong Kong HSI rose 2.04%. China Shanghai SSE rose 1.46%. Singapore Strait Times rose 1.85%. Japan 10-year JGB yield fell -0.055 to 2.304.

US Retail Sales Strength Continues, Core Measures Show Broad-Based Gains

US retail sales surprised to the upside in February, rising 0.6% as consumer demand stayed resilient. Core measures also showed steady gains, highlighting broad-based spending strength. Read more.

US ADP Jobs Beat at 62k, Wage Growth Picks Up for Job-Changers

US private hiring came in stronger than expected in March, with ADP jobs rising to 62k. While overall hiring remains steady, the real shift is in wages, with job-changers seeing faster pay growth. The data highlights a labor market that is stable but increasingly uneven beneath the surface. Read more.

UK PMI Manufacturing Finalized at 51.0, Input Costs Surge and Confidence Drops

UK manufacturing growth slowed in March, with PMI slipping to 51.0. But the bigger story is surging input costs and worsening supply delays, with price pressures hitting their highest levels since 1992. As confidence drops and job cuts accelerate, production is being squeezed despite stable demand. Read more.

Eurozone PMI Manufacturing Finalized at 45-Month High But War-Fueled Inflation Clouds Outlook

Eurozone manufacturing PMI rose to 51.6 in March, marking its strongest level in nearly four years. But the Middle East war is already pushing up energy costs and disrupting supply chains, with firms passing higher prices to customers. As inflation pressures build, the recovery is becoming more fragile. Read more.

Japan’s Strong Tankan Signals Support BoJ Normalization Despite External Risks

Japan’s Tankan survey surprised to the upside, with stronger business sentiment and capex plans signaling resilient corporate activity. More importantly, inflation expectations climbed to record levels, reinforcing the case for further BoJ normalization. However, rising energy costs tied to Middle East tensions continue to cloud the outlook. Read more.

Japan PMI Manufacturing Finalized at 51.6, War-Driven Cost Pressures Build

Japan’s manufacturing PMI eased to 51.6 in March, signaling slower growth after February’s 45-month peak. However, the bigger shift came from surging input costs, with firms facing the sharpest price increases in over 18 months due to Middle East tensions. As companies pass on higher costs and turn more cautious, inflation risks are building even as momentum softens. Read more

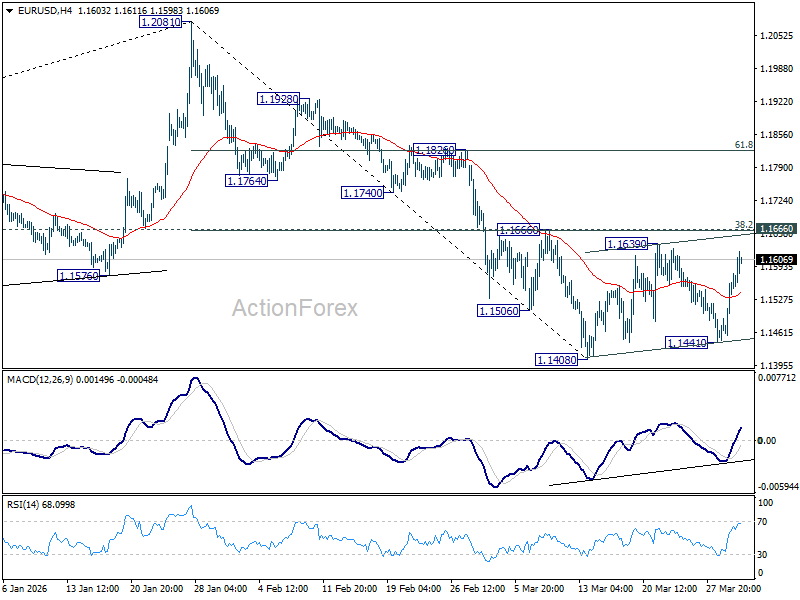

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1479; (P) 1.1521; (R1) 1.1596; More….

EUR/USD’s rebound from 1.1441 extended further, but still it’s capped below 1.1666 cluster resistance (38.2% retracement of 1.2081 to 1.1408 at 1.1665). Price actions from 1.1408 are viewed as a consolidations pattern and further decline is expected. On the downside, firm break of 1.1408 will resume the fall from 1.2081 to 38.2% retracement of 1.0176 to 1.2081 at 1.1353. However, decisive break of 1.1666 will argue that the fall from 1.2081 has completed, and turn bias back to the upside for 61.8% retracement of 1.2081 to 1.1408 at 1.1824.

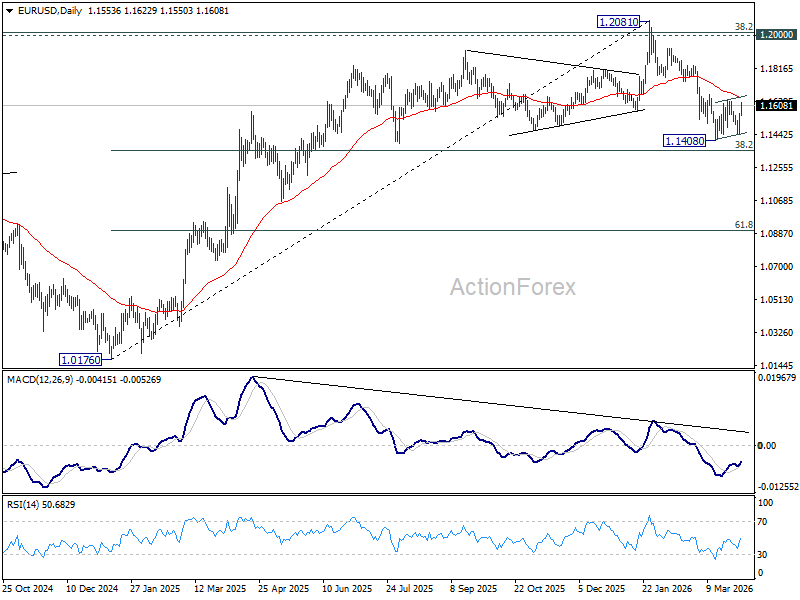

In the bigger picture, prior break of 55 W EMA (now at 1.1497) should confirm rejection by 1.2 key cluster resistance level. The whole up trend from 0.9534 (2022 low) might have completed as a three wave corrective rise too. Deeper fall is expected to long term channel support (now at 1.0535). Meanwhile, risk will stay on the downside as long as 1.2081 holds, even in case of strong rebound.

{kind=link}