GBP/CAD climbed to its highest level in a decade this week, reflecting an increasingly powerful divergence between a Pound supported by fading domestic political risks and a Canadian Dollar facing mounting structural headwinds. Sterling continues to benefit from the unwinding of sizeable speculative short positions built ahead of Prime Minister Keir Starmer’s resignation, while Bank of England Governor Andrew Bailey has effectively ruled out near-term rate cuts. With Bank Rate holding at 3.75% versus the Bank of Canada’s 2.25%, the existing yield advantage remains firmly intact. More recently, however, the rally has found an additional and arguably more durable driver: rising uncertainty over Canada’s trade outlook.

The turning point came on July 1, when the Trump administration declined to extend the USMCA at its mandatory trilateral review. Although the agreement remains in force under an annual review mechanism for up to another decade, the decision marks a meaningful increase in long-term policy uncertainty rather than an immediate disruption to trade. Instead of securing another 16-year extension, businesses now face the prospect of recurring negotiations and periodic reviews. That uncertainty could weigh on investment and growth over coming years, reducing the likelihood that the Bank of Canada will need to tighten policy further.

The BoC has already downplayed the inflationary impact of higher energy prices, arguing there is limited evidence that rising oil costs are feeding into broader price pressures. Together, the trade outlook and the central bank’s cautious stance point to a policy bias that is becoming increasingly less supportive for the Canadian Dollar.

Market positioning reinforces that narrative. Speculative bearish bets against the Canadian Dollar have climbed to their highest level since December, while Canada’s two-year yield trades more than 140 basis points below its US counterpart, the widest gap since last May.

Attention now turns to June employment data from Canada due tomorrow, which could determine whether markets further strengthen expectations ahead of the Bank of Canada’s July 15 meeting. Consensus looks for employment to rise by around 10,000 after May’s outsized 88,000 gain, with the unemployment rate holding at 6.6%.

The risks appear asymmetric. A weaker-than-expected report would reinforce the existing bearish narrative by strengthening expectations that the BoC remains firmly on hold or even shifts toward easing eventually. By contrast, an in-line or even moderately stronger report may offer only temporary relief while the broader uncertainty surrounding USMCA continues to overshadow Canada’s medium-term outlook.

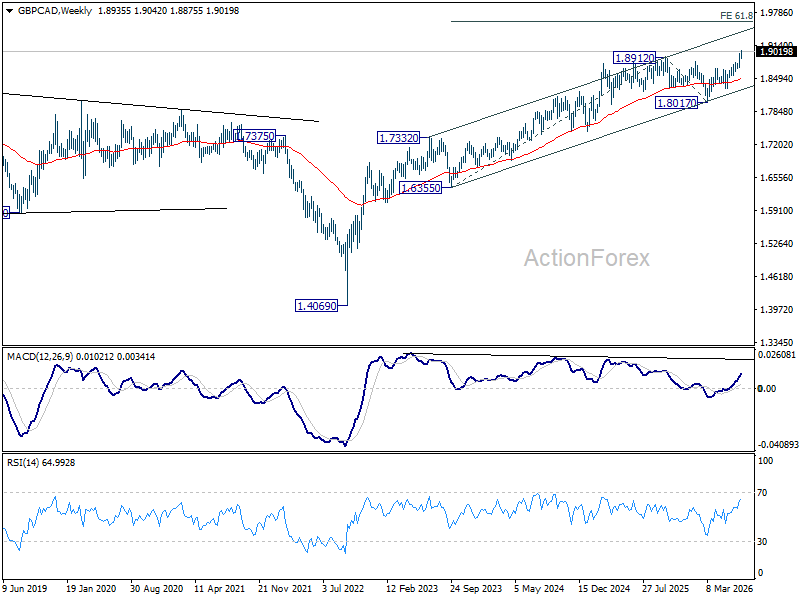

Technically, further rise is expected in GBP/CAD as long as 1.8875 support holds. Immediate focus is on medium term rising channel resistance (now at 1.9049). Decisive break there could prompt upside acceleration to 138.2% projection of 1.8017 to 1.8694 from 1.8299 at 1.9235. Break of 1.8875 will delay the bullish case, and bring consolidations first.

In the bigger picture, GBP/CAD is extending the whole up trend from 1.4069 (2022 low). Next medium term target is 61.8% projection of 1.6355 to 1.8912 from 1.8017 at 1.9597.

{kind=link}