Silver’s recovery lost momentum below the $60 mark this week despite softer-than-expected US inflation, highlighting a macro backdrop that has become less supportive than many investors anticipated. Ordinarily, a downside surprise in CPI would trigger a broader Dollar selloff and provide precious metals with a meaningful tailwind. This time, however, the Dollar’s decline proved relatively shallow and uneven, while buying interest in Silver remained subdued. Together, those factors have kept the metal trapped within its recent trading range and preserved a bearish near-term outlook.

The first headwind has been the Dollar itself. Although the Dollar Index initially fell following June’s weaker CPI report, it recovered a meaningful portion of those losses after Federal Reserve Chair Kevin Warsh reaffirmed the Fed’s commitment to restoring price stability while avoiding any dovish policy signals during his congressional testimony. The Dollar’s weakness was also concentrated in a handful of currencies with their own domestic catalysts, particularly the Canadian Dollar, supported by stronger oil prices and a more hawkish Bank of Canada outlook, and the New Zealand Dollar following hawkish comments from RBNZ Chief Economist Paul Conway. Against the Euro, Sterling, Swiss Franc and Yen, Dollar weakness was comparatively modest. Without a broad-based decline in the US currency, Silver has struggled to attract the sustained buying that typically follows softer US inflation.

Muted demand has reinforced that pressure. While positioning data are not yet available to confirm investor behavior, price action suggests opportunistic buying following the CPI release was considerably weaker than in previous episodes of Dollar weakness. The inability to reclaim the $60 level despite an ostensibly supportive inflation report indicates that buyers remain cautious, leaving the metal vulnerable if the Dollar regains strength or Treasury yields move higher again.

Beyond the immediate macro backdrop, Silver also faces a more structural challenge through industrial demand. The market is currently in its sixth consecutive annual supply deficit, but unlike many commodities, higher prices do not necessarily generate a meaningful increase in supply. Around 70% of global Silver production comes as a by-product of copper, lead and zinc mining, meaning output decisions depend primarily on those metals rather than Silver prices. New mine development also typically requires seven to ten years, leaving demand adjustment as the principal mechanism for balancing the market.

That demand adjustment may already be underway. China’s largest solar manufacturer, Longi Green Energy, has begun commercial production using copper-metallized solar cells, reducing reliance on Silver in one of the metal’s fastest-growing industrial applications. Given that the solar sector accounted for roughly 17% of global Silver demand last year, broader adoption of copper metallization could gradually weaken one of Silver’s most important structural demand drivers. The transition is unlikely to transform the market overnight, but it represents a notable shift in the long-term balance between supply and demand.

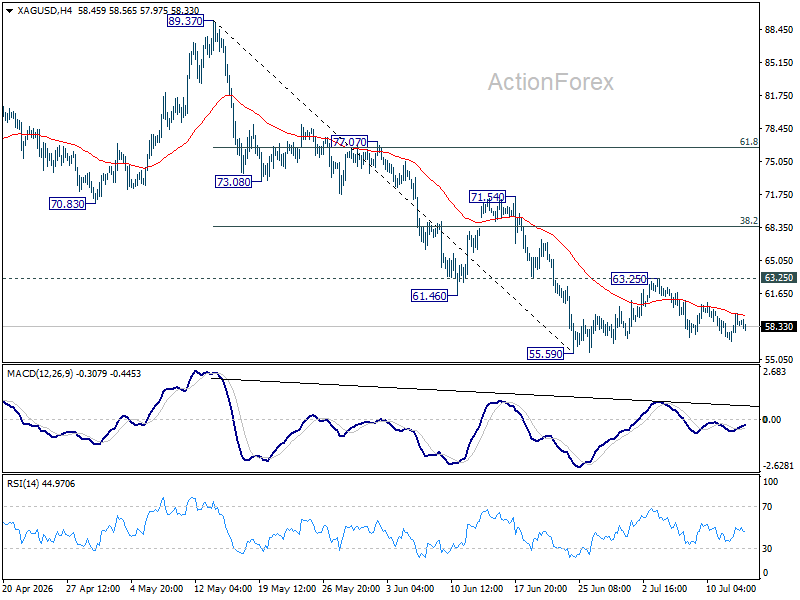

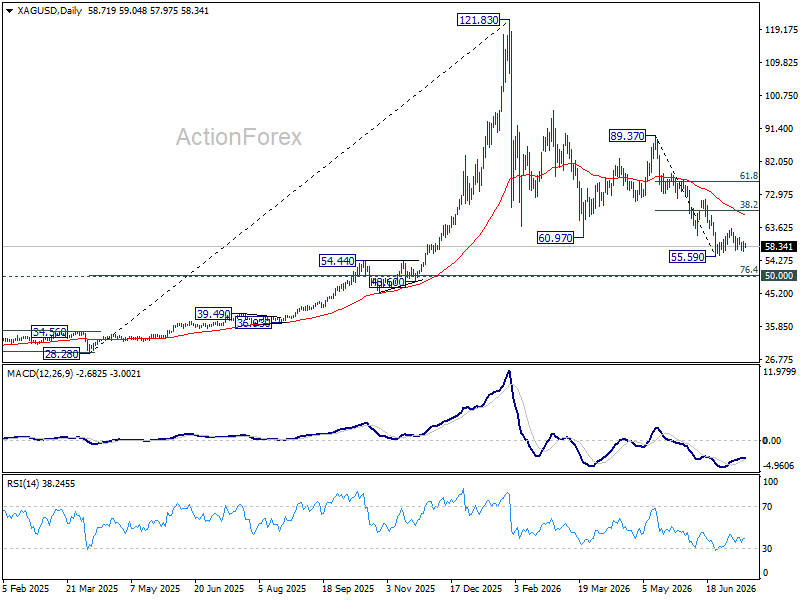

Technically, the outlook remains bearish while resistance at 63.25 caps upside. A break below 55.59 would resume the broader decline from the record high of 121.83 to o 76.4% retracement of 28.28 to 121.83 at 50.35, which is close to 50 psychological level.

Conversely, sustained break above 63.25 would delay the bearish scenario and extend the corrective rebound toward with another rising leg to 38.2% retracement of 89.37 to 55.59 at 68.49 instead.

Until the Dollar weakens more broadly, however, Silver appears increasingly vulnerable to another leg lower.

{kind=link}