Dollar fell broadly in early trading after June CPI delivered a much larger-than-expected downside surprise, shifting market attention away from escalating geopolitical risks and back toward a more benign inflation outlook. Headline CPI fell -0.4% on the month while core CPI was unchanged, both undershooting expectations and challenging the aggressive repricing toward additional Federal Reserve tightening that had gathered pace over the past week. The softer inflation data also reduced the immediate significance of Fed Chair Kevin Warsh’s first semiannual congressional testimony, giving policymakers greater flexibility to remain patient despite renewed strength in oil prices.

The inflation report arrived against a dramatically different geopolitical backdrop. Brent crude climbed above $87 after fighting between the United States and Iran intensified again. Iran launched ballistic missiles at a US air base in Jordan, while US forces carried out another extended wave of strikes against Iranian targets as both sides continued battling for control of the Strait of Hormuz. The renewed hostilities have further undermined confidence that last month’s memorandum of understanding guaranteeing shipping through the Strait will evolve into a lasting peace agreement, keeping energy markets on edge and reinforcing concerns that higher oil prices could eventually feed back into global inflation.

Yet markets drew a distinction between today’s inflation and tomorrow’s inflation risks. June’s CPI reflected the earlier decline in energy prices, with the energy component recording its largest monthly fall since April 2020, while shelter inflation slowed to its weakest monthly increase since January 2021. Those developments suggested underlying price pressures continued to moderate before the latest rebound in crude prices. Although the renewed surge in oil still poses an upside risk to future inflation, investors concluded the Fed now has more time to assess whether higher energy costs become embedded in broader price pressures before responding with additional tightening.

That shift substantially lowers the stakes surrounding Warsh’s congressional appearance. Having repeatedly argued against providing explicit forward guidance, the new Fed Chair now has greater room to maintain that communication strategy. Rather than facing pressure to signal an imminent rate increase following Governor Christopher Waller’s hawkish remarks on Monday, Warsh can point to softer inflation while emphasizing that policy will continue to depend on incoming data. Unless lawmakers force a more explicit discussion of future rate moves, the testimony is increasingly likely to produce few meaningful policy surprises.

Currency markets reflected the improved risk backdrop despite escalating tensions in the Middle East. For the week so far, New Zealand Dollar remained the strongest performer after hawkish comments from RBNZ Chief Economist Paul Conway reinforced expectations of additional policy tightening. Canadian Dollar benefited from higher oil prices, while Euro also traded firmly. By contrast, Dollar joined Yen and Swiss Franc among the week’s weakest performers, suggesting investors were responding more to easing Fed expectations than to geopolitical headlines. Sterling and Australian Dollar traded in the middle of the performance rankings as markets balanced softer US inflation against persistent uncertainty over the global energy outlook.

US CPI Misses Forecasts at 3.5%, Core Inflation at 2.6%

US inflation slowed much more than expected in June, with headline CPI falling -0.4% on the month and core CPI unexpectedly flat. The sharp decline was driven by a 5.7% drop in energy prices, the largest monthly fall since April 2020, while shelter inflation also recorded its smallest monthly increase since January 2021. The softer data challenge recent Fed tightening expectations ahead of Fed Chair Kevin Warsh’s congressional testimony. Read More.

AUD/NZD Tests Double Top Breakdown as RBNZ’s Conway Revives Faster Tightening Bets

Paul Conway’s latest speech suggests the RBNZ’s inflation assumptions are already being challenged by the rebound in oil prices. He warned that New Zealand businesses now pass through higher costs more readily and are less likely to cut prices when costs ease, increasing the risk that temporary supply shocks become persistent inflation requiring a firmer monetary policy response. Read More.

Gold Slides as Oil Surges and Fed Hike Bets Build, Leaving $4,000 Increasingly Vulnerable

Gold extended its decline as Brent crude briefly climbed above $85 and markets sharply increased expectations for another Federal Reserve rate hike following hawkish remarks from Governor Christopher Waller. With traders awaiting US CPI and Fed Chair Kevin Warsh’s congressional testimony, the psychologically important $4,000 level is looking increasingly vulnerable. A decisive break would shift focus to 3942.23, with the broader bearish trend targeting 3606.49. Read More.

Australia NAB Business Confidence Rebounds to -5 as Inflation Pressures Ease

Australia’s NAB Business Survey showed business confidence rebounding sharply in June as fears over the Middle East conflict and energy prices eased. At the same time, purchase cost growth, final product price inflation and retail prices all moderated, suggesting the earlier oil shock had a smaller impact on inflation than feared. Read More.

Australia Westpac Consumer Sentiment Rebounds to 83.9, but Pessimism Still Runs Deep

Australia’s Westpac–Melbourne Institute Consumer Sentiment Index rose 4.1% to 83.9 in July after the RBA paused its tightening cycle, easing fears of rapid further rate hikes. However, confidence remains among the weakest in the survey’s 50-year history, while persistent inflation keeps attention firmly on the June quarter CPI report ahead of the RBA’s August meeting. Read More.

NZIER QSBO Signals Improving Confidence but Sticky Inflation Risks

New Zealand’s latest NZIER Quarterly Survey of Business Opinion showed confidence improving sharply in the June quarter as fuel prices eased, with a net 12% of firms expecting better economic conditions. However, hiring and investment intentions remained weak, while more than half of businesses reported rising costs and a growing number passed those increases on to customers, highlighting persistent inflation pressures for the RBNZ. Read More.

China Trade Data Crushes Forecasts as Exports and Imports Accelerate in June

China’s trade growth accelerated sharply in June, with exports rising 27.0% and imports climbing 36.0%, both well above expectations. Semiconductor exports more than doubled to USD 38B, while stronger shipments to the US, ASEAN and the EU underscored resilient global demand. The main weak spot was crude oil imports, which fell -41% from a year earlier. Read More.

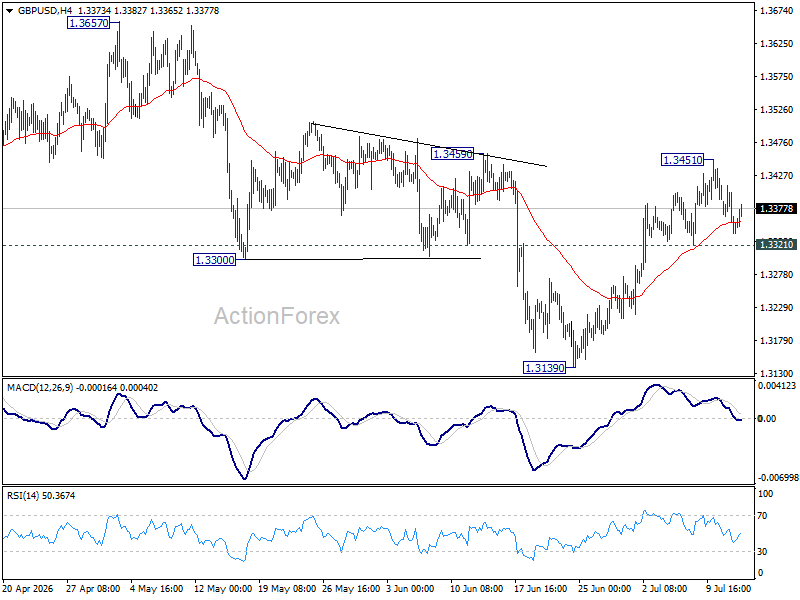

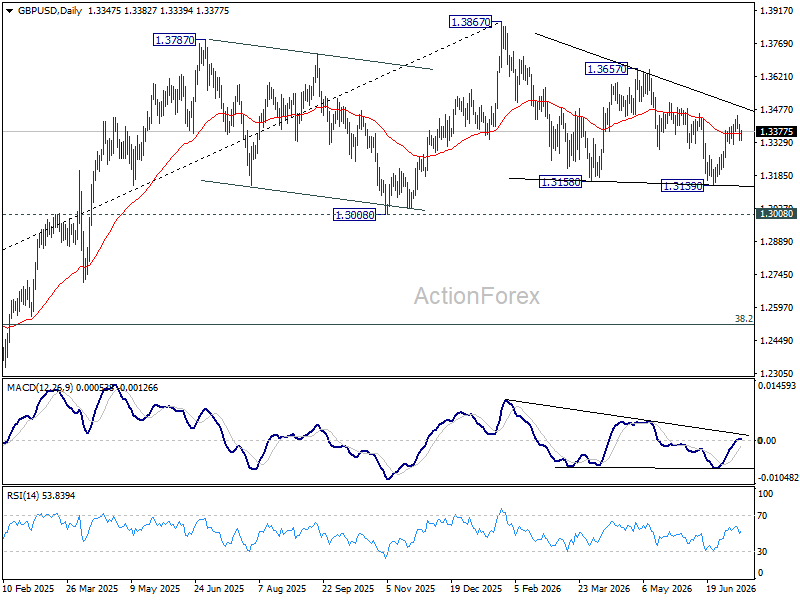

GBP/USD Daily Outlook

Intraday bias in GBP/USD stays neutral for consolidations below 1.3451. On the upside, firm break of 1.3459 will argue that whole correction from 1.3867 has completed, and target 1.3657 resistance for confirmation. On the downside, break of 1.3451 will turn bias back to the downside for 1.3139 support instead.

In the bigger picture, price actions from 1.3867 are a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is in favor for a later stage, towards 1.4248 key resistance (2021 high). However, firm break of 1.3008 will at least bring deeper fall to 38.2% retracement of 1.0351 to 1.3867 at 1.2524, with increased risk of bearish reversal.

{kind=link}