Escalating conflict in the Middle East would normally be enough to send the Dollar sharply higher. Instead, markets hesitated. Brent crude climbed above $79 after the weekend’s dramatic expansion of the US-Iran conflict, but stopped short of the $80 threshold that could trigger a broader inflation repricing. Besides, rather than rebuilding aggressive Dollar longs, traders opted to wait for Tuesday’s US June CPI report and Kevin Warsh’s first congressional testimony as Federal Reserve Chair, two events that could prove far more consequential for the policy outlook than the latest geopolitical headlines.

The restrained market reaction suggests investors are not yet convinced that the latest escalation will produce a sustained energy shock. Although Iran widened its retaliation across several Gulf states and the US launched its largest strikes of the conflict, Brent has yet to establish itself decisively above $80. That hesitation indicates traders are still reluctant to restore the full geopolitical risk premium that faded after oil prices retreated in recent weeks. Without a convincing break higher in crude, markets have little reason to materially revise inflation expectations or Fed pricing.

Attention is instead firmly fixed on an unusually important sequence of events in Washington. June CPI will be released at 12:30 GMT on Tuesday, with Warsh appearing before the House Financial Services Committee roughly 90 minutes later in his first congressional testimony since becoming Fed Chair. The Senate Banking Committee hearing follows on Wednesday, allowing lawmakers to respond after markets have had time to digest both the inflation data and Warsh’s initial comments. The timing is exceptional, giving investors an almost immediate indication of how the new Fed Chair interprets a critical inflation report.

Friday’s Monetary Policy Report provides the framework for both the CPI release and Warsh’s testimony. As the semiannual Humphrey-Hawkins report, it effectively serves as the blueprint for his prepared remarks. The report described the US economy as expanding at a solid pace, with Q1 GDP growing at a 2.1% annualized rate, supported by strong high-tech investment and a rebound in government spending, while consumer spending remained only modest and residential investment stayed weak. The labor market was characterized as broadly stable, with unemployment holding at 4.2%, supported by slowing labor-force growth even as private payroll gains strengthened.

Inflation remains the central issue. The report highlighted headline PCE inflation accelerating to 4.1% and core PCE to 3.4%, attributing the increase to three specific forces: tariff-driven import prices, higher energy costs linked to Middle East supply disruptions, and stronger AI-related demand for technology goods. At the same time, housing services inflation has continued to ease, suggesting underlying inflation pressures are becoming less broad-based. That framework means Tuesday’s CPI report will be judged less by the headline figure alone than by whether energy prices and core goods continue to account for most of the inflation strength.

Currency markets reflected that cautious positioning. New Zealand Dollar outperformed after the BusinessNZ Performance of Services Index returned to expansion, reinforcing signs the domestic recovery is regaining momentum. Canadian Dollar also found support from stronger oil prices ahead of Wednesday’s Bank of Canada policy decision, while Euro traded firmer. At the other end of the spectrum, Yen remained under pressure as optimism surrounding Japan’s government pension fund initiative continued to fade, with Swiss Franc and Australian Dollar also lagging. Sterling and Dollar traded closer to the middle of the performance table as investors preferred to await Tuesday’s potentially market-defining events.

Markets Ran Ahead of Tokyo: Yen Weakens as GPIF Expectations Meet Reality

Markets pared expectations of an imminent overhaul of Japan’s GPIF investment strategy after officials clarified there are no immediate plans to revise the pension fund’s benchmark asset allocation. The Yen weakened as investors unwound Friday’s optimism, while stronger New Zealand services data reinforced the country’s economic recovery, helping NZD/JPY extend its rebound toward key resistance at 93.80. Read More.

Brent Oil May Target $85 If US-Iran Escalation Pushes It Through $80

Brent oil surged above $79 after US-Iran conflict widened into a multi-country confrontation across Gulf. Attack on commercial shipping, Iran’s claim that Strait of Hormuz is closed and broader retaliation against US-aligned states have raised risk of prolonged disruption. Technically, firm break above 80.59 could open way toward 85.67, close to 55-day EMA at 85.59. Read More.

New Zealand BNZ PSI: Services Sector Returns to Expansion, but Recovery Still Tentative

New Zealand’s services sector returned to expansion in June as the BusinessNZ PSI rose to 50.6 from 48.0, ending five months of contraction. Strong gains in new orders suggest demand is improving, but employment and activity remained below 50, indicating the recovery is still in its early stages. The data reinforce expectations that economic growth is recovering gradually without materially changing the RBNZ’s cautious policy outlook. Read More.

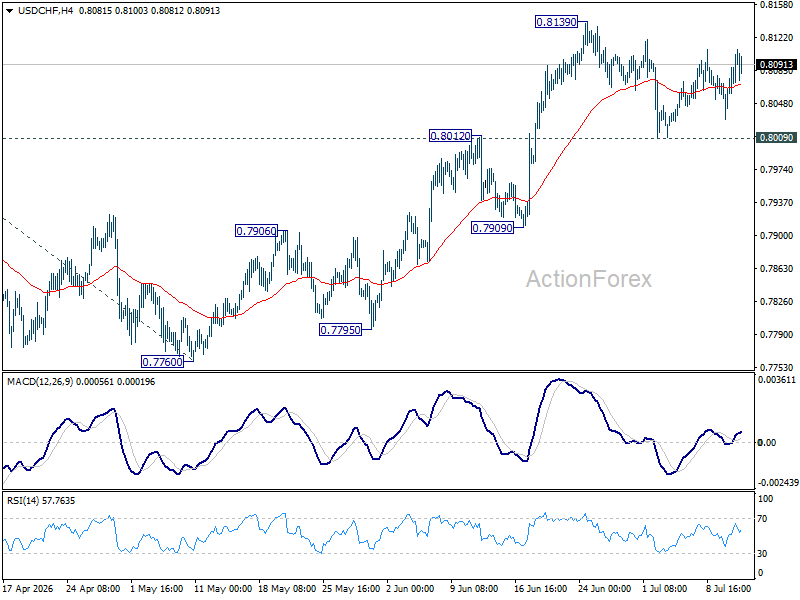

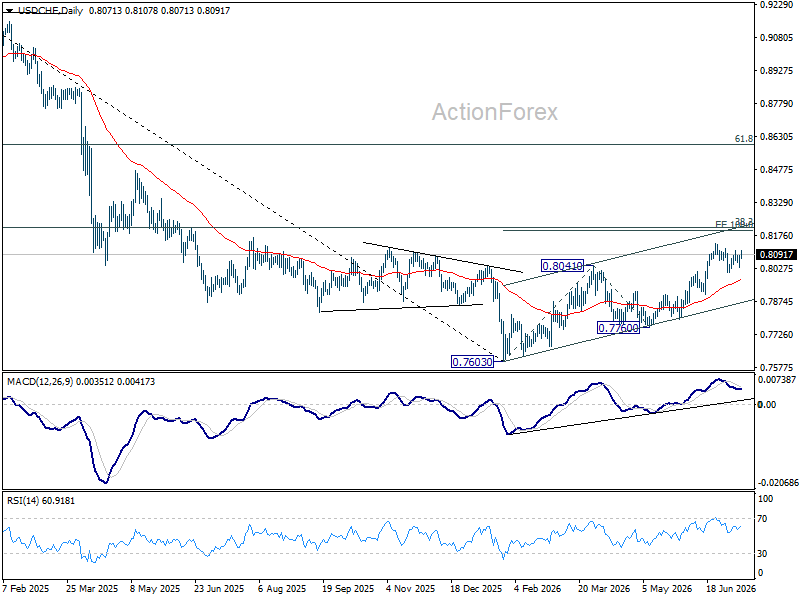

USD/CHF Daily Outlook

Range trading continues in USD/CHF and intraday bias stays neutral. With 0.8009 support intact, further rise is expected. On the upside, above 0.8139 will extend the rally from 0.7760 to 100% projection 0.7603 to 0.8041 from 0.7600 at 0.8198 next. However, sustained break of 0.8012 will bring deeper fall to 0.7909 support instead.

In the bigger picture, while a medium term bottom was formed at 0.7603, it’s still early to call for bullish trend reversal. As long as 38.2% retracement of 0.9200 (2025 high) to 0.7603 at 0.8213 holds, the larger down trend could still continue through 0.7603 at a later stage. However, firm break of 0.7603 will argue that the trend has reversed and turn focus to 0.8332 support turned resistance (2023 low) for confirmation.

{kind=link}