Dollar’s decline extended overnight after Fed left interest rates unchanged as widely expected. The dollar index reaches as low as 99.42 so far is is pressing 99.43 key near term support level. Markets continued to pare back expectation on Fed higher. Fed fund futures are pricing in 17.7% chance of March hike an 69.0% only. Nonetheless, treasury yield was steady with 10 year yield closed up 0.023 to 2.474. Stocks also stabilized with DJIA closed up slightly by 26.85 pts, or 0.14%, at 19890.94. S&P 500 rose 0.68 pts, or 0.03%, to close at 2279.55. In the currency markets, Dollar remains the weakest major currency this week. On the other hand Yen stays the strongest , followed closely by Aussie and Loonie. In other markets, Gold rides on Dollar weakness and surges to as high as 1210.2 so far today, and is set to take on 1220.1 resistance. WTI crude oil stays in familiar range and hovers around 53.5.

FOMC voted unanimously to leave its policy rate within a target range of 0.50-0.75%. The outcome had been widely anticipated as the Fed just adopted rate hike of 25 bps in December. Only minor changes were seen in the accompanying statement. In short, policymakers retained the stance that future interest rate change would be ‘data dependent’. They also reiterated that economic conditions will evolve in a manner that will warrant only gradual increases in the federal fund rate’. Fed’s view on the economic outlook has not changed, with overall growth remaining ‘moderate’ and the balance of risks ‘roughly balanced’. The focus will now turn to Chair Yellen’s Congressional testimony on February 14-15. During the 1.5 week period, we would receive the employment report for January. More in Fed Upbeat About Employment, Next Rate Hike Data Dependent.

BoE "Super Thursday" is the main focus today. The central bank is expected to keep interest rate unchanged at 0.25% and hold asset purchase target at GBP 435b. This key focus in on the quarterly inflation report. It’s widely expected that BoE would raise inflation forecast, and thus, add to the case to stand pat for the rest of the year. However, policymaker’s view on the impact of Brexit to growth is still quite unclear. And the markets would hope to get some more hints on that from the latest projections. Meanwhile, markets are pricing in 50% of rate hike by the end of this year. most economists expected that BoE would be on hold until mid-2019.

On the data front, Japan monetary base rose 22.6% yoy in January. Australia trade surplus widened to AUD 3.51b in December, building approvals dropped -1.2% mom. Japan consumer confidence rose 0.1 pt to 43.2 in January. Swiss will release retail sales in December. Eurozone will release PPI. UK will release construction PMI. US will release Challenger job cuts, non-farm productivity and jobless claims.

AUD/USD Daily Outlook

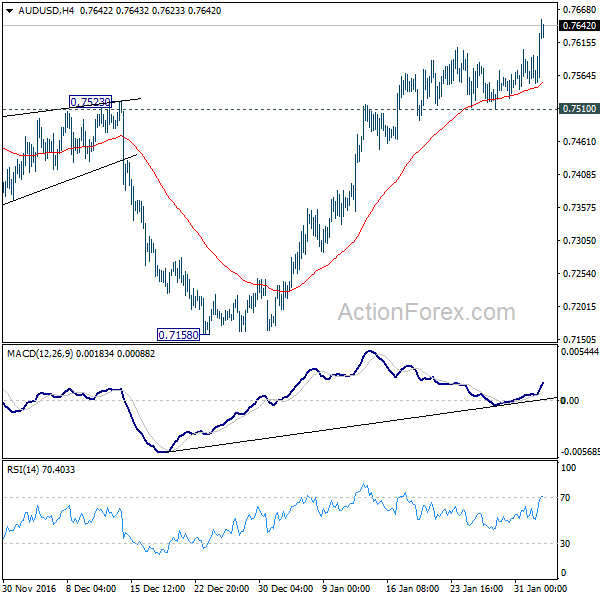

Daily Pivots: (S1) 0.7558; (P) 0.7577; (R1) 0.7603; More…

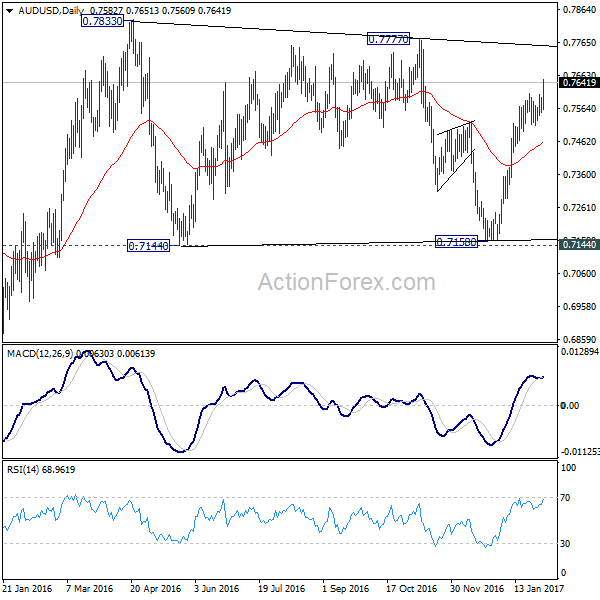

AUD/USD’s rebound from 0.7158 resumed by taking out 0.7608 and reaches as high as 0.7651 so far. Intraday bias is back on the upside for 0.7777 resistance next. At this point, we’d still expect strong resistance from 0.7777/7833 resistance zone to bring near term reversal. On the downside, break of 0.7448 support will indicate that rebound from 0.7510 has completed. That will turn bias to the downside for 0.7144 key support level.

In the bigger picture, AUD/USD is staying inside long term falling channel and it’s likely that the down trend from 1.1079 is still in progress. Break of 0.6826 low will confirm this bearish case. We’ll be looking for bottoming sign again as it approaches 0.6008 key support level. Meanwhile, sustained break of 0.7833 resistance will be a strong sign of medium term reversal.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Consensus | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Monetary Base Y/Y Jan | 22.60% | 24.20% | 23.10% | |

| 0:30 | AUD | Trade Balance (AUD) Dec | 3.51B | 2.00B | 1.24B | 2.04 |

| 0:30 | AUD | Building Approvals M/M Dec | -1.20% | -1.80% | 7.00% | 7.50% |

| 5:00 | JPY | Consumer Confidence Jan | 43.7 | 43.1 | ||

| 8:15 | CHF | Retail Sales (Real) Y/Y Dec | -0.70% | 0.90% | ||

| 9:00 | EUR | ECB Economic Bulletin | ||||

| 9:30 | GBP | Construction PMI Jan | 53.8 | 54.2 | ||

| 10:00 | EUR | Eurozone PPI M/M Dec | 0.50% | 0.30% | ||

| 10:00 | EUR | Eurozone PPI Y/Y Dec | 1.20% | 0.10% | ||

| 12:00 | GBP | BoE Rate Decision | 0.25% | 0.25% | ||

| 12:00 | GBP | BoE Asset Purchase Target | 435B | 435B | ||

| 12:00 | GBP | MPC Official Bank Rate Votes | 0–0–9 | 0–0–9 | ||

| 12:00 | GBP | MPC Asset Purchase Facility Votes | 0–0–9 | 0–0–9 | ||

| 12:00 | GBP | BoE Inflation Report | ||||

| 12:30 | USD | Challenger Job Cuts Y/Y Jan | 42.40% | |||

| 13:30 | USD | Non-Farm Productivity Q4 P | 0.90% | 3.10% | ||

| 13:30 | USD | Unit Labor Costs Q4 P | 1.90% | 0.70% | ||

| 13:30 | USD | Initial Jobless Claims (JAN 28) | 251K | 259k | ||

| 15:30 | USD | Natural Gas Storage | -119B |

Subscribe to our daily and mid-day newsletter to get this report delivered to your mail box

{kind=link}