Dollar jumps overnight after hawkish FOMC minutes and remains the strongest one for the week. Nonetheless, the greenback is paring some gains in Asian session. And it’s still limited below key near term resistance against most major currencies, except versus Canadian Dollar. Markets sentiment have shifted much since the start of the year. Back then, most doubted whether Fed would really hike three times this year. After a string of solid data and yesterday’s minutes, traders are now talking whether Fed could hike more than four times. US treasury jumped on such expectations while stocks reversed some of recent rebound. DOW ended the day down -0.67% at 2479.78. For now, it remains to be seen whether Dollar would finally re-couple with yields.

FOMC minutes affirmed more hikes ahead

Minutes of the January 30-31 FOMC meeting affirmed the Fed’s hawkish stance. The key take away is that "a majority of participants noted that a stronger outlook for economic growth raised the likelihood that further gradual policy firming would be appropriate. Growth remained "above trend" while labor market "stayed strong". And there are "upside risks" to growth because of the tax cuts. Meanwhile, "almost all participants" expected inflation to move up to the 2% target over the "medium term".

It should be noted that the meeting was held before January non-farm payroll report and CPI release. NFP showed stronger than expected wage growth at 0.3% mom. CPI jump a strong 0.5% mom while core CPI rose 0.3% mom. The developments could prompt Fed to turn even more hawkish ahead.

Treasury yields extended recent rally after the FOMC minutes. 10 year yield reached as high as 2.943 and hit the highest level since 2014. Recent up trend in TNX is on track for 3.036 key resistance. We’d like to reiterate that the zone between 3.036 and 100% projection of 1.336 to 2.621 from 2.034 at 3.318 is the long term trend redefining area. A solid break above will declare we’ve finally exited the low interest rate era.

BoE Haldane: Wage growth could jump above 3%

BoE Chief Economist Andrew Haldane told Parliament Treasury Committee that wage growth will pick up amid record low unemployment. He said that "the long-awaited — and we have been waiting for a long time — pickup in wages is starting to take root." And, "We get intelligence from our agents that would suggest that wage settlements this year were going to pick up, perhaps to a number with a three in front of it, rather than a two in front of it." Also, risks for the UK economy were "to the upside". Nonetheless, neither Haldane, nor Governor Mark Carney, gave any hint on the timing of the next rate hike.

Looking ahead

ECB minutes will be the main focus of the day. The central bank has hinted at tweaking its forward guidance regarding the asset purchase program. But nonetheless was done so far. The markets would like to know what were being discussed during the meeting regarding this topic, for gauging the chance of ending the APP after September.

In addition, Germany will release Ifo business climate in European session. UK will release Q4 GDP revision, index of services and CBI reported sales.

Later in the day Canadian Dollar will take center stage with retail sales featured. US will release jobless claims and leading index.

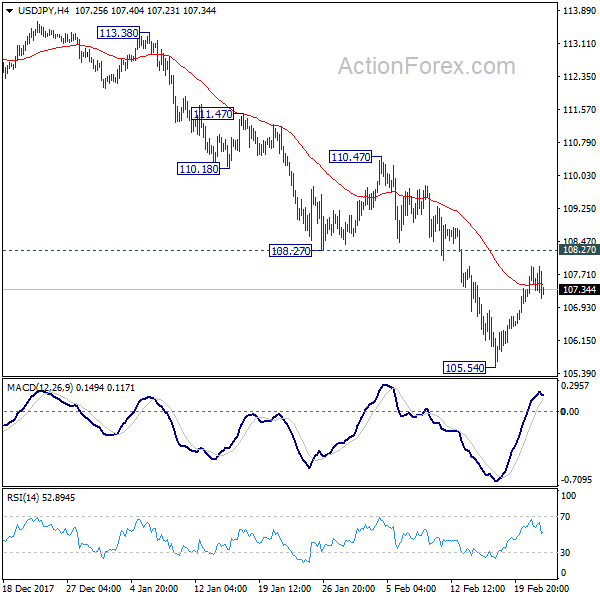

USD/JPY Daily Outlook

Daily Pivots: (S1) 107.39; (P) 107.64; (R1) 108.03; More…

No change in USD/JPY’s outlook. While the rebound from 105.54 is strong, it’s limited below 108.27 support turned resistance. Such rebound is seen as a corrective move. Intraday bias stays neutral and near term outlook remains bearish. Below 105.54 will extend the larger fall from 118.65 and target 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next. However, break of 107.72 will be the first sign of near term reversal and will target 110.47 resistance for confirmation.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48. now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 09:00 | EUR | German IFO Business Climate Feb | 117 | 117.6 | ||

| 09:00 | EUR | German IFO Expectations Feb | 107.9 | 108.4 | ||

| 09:00 | EUR | German IFO Current Assessment Feb | 127 | 127.7 | ||

| 09:30 | GBP | GDP Q/Q Q4 P | 0.50% | 0.50% | ||

| 09:30 | GBP | Index of Services 3M/3M Dec | 0.50% | 0.40% | ||

| 11:00 | GBP | CBI Reported Sales Feb | 14 | 12 | ||

| 12:30 | EUR | ECB Monetary Policy Meeting Accounts | ||||

| 13:30 | USD | Initial Jobless Claims (17 FEB) | 231K | 230K | ||

| 13:30 | CAD | Retail Sales M/M Dec | -0.10% | 0.20% | ||

| 13:30 | CAD | Retail Sales Ex Auto M/M Dec | 0.00% | 1.60% | ||

| 15:00 | USD | Leading Index Jan | 0.70% | 0.60% | ||

| 15:30 | USD | Natural Gas Storage | -194B | |||

| 16:00 | USD | Crude Oil Inventories | 1.8M |