{kind=link}

Dollar is trying to recover in Asian session today after the steep new year selloff. Nonetheless, the greenback remains the second weakest one for the week, just next to Kiwi. S&P 500 and NASDAQ closed at records high at 26951.81 and 7006.90 overnight. DOW also gained 104.79 pts or 0.42% to 24824.01. 10 year yield staged a strong rebound by gaining 0.06 to 2.465 but that was mainly driven by surge in European yields, including Germany and UK. In other markets, gold breached 1320 handle before retreating mildly today. WTI crude oil is also holding above 60 handle.

ECB Nowotny: QE may end in 2018

ECB Governing Council member Ewald Nowotny said in a newspaper interview that the central bank could end the asset purchase program this year and there is continuous improvements in growth in Eurozone. Inflation is still expected to miss the 2% target ahead. But Nowotny said that "we should not see that too dogmatically." Instead, "if the economy continues to do so well, we could let the program run out in 2018". Meanwhile, he also warned that funds are "flooding" into European stock markets and warned of risks of bubble.

CDU and SPD still at odds for grand coalition

In Germany, leaders of Chancellor Angela Merkel’s CDU/CSU will meet today to prepare for the exploratory coalition talk with SPD scheduled for January 7 through 12. The chance for the rebirth of grand coalition seems get dimmer as the two largest parties are still at odds over a couple of issues. SPD deputy leader Thorsten Schaefer-Guembel cited in a newspaper interview the differences with CUD/CSU over tax, healthcare, immigration, Europe and work regulations. And he emphasized that "a minority government remains an option, even if Chancellor Angela Merkel doesn’t want to acknowledge that."

And, Wolfgang Steiger, secretary general of CDU’s economic council, said that Germany could face "enormous financial burdens for generations" if SPD manages to push through the spending plans in the grand coalition. And he warned that "a grand coalition will be more expensive in the long term than a minority government."

UK in talks to join TPP

In UK, it’s reported that the government is in talks to join the so called Trans-Pacific Partnership for post-Brexit international trades. British Trade Minister Greg Hands said despite the geographical difference, "nothing is excluded in all of this," and "with these kind of plurilateral relationships, there doesn’t have to be any geographical restriction." The department of international trade also said that "it is early days, but as our trade policy minister has pointed out, we are not excluding future talks on plurilateral relationships."

But the initiative drew criticism from other politicians. Shadow Trade Minister Barry Gardiner complained that "this plan smacks of desperation. These people want us to leave a market on our doorstep and join a different, smaller one on the other side of the world. It’s all pie in the sky thinking."

The TPP is renamed as Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) after the US withdrew last year under the decision of President Donald Trump. There are eleven remaining members including Australia, Brunei, Canada, Chile, Japan, Malaysia, Mexico, New Zealand, Peru, Singapore and Vietnam. A partial agreement was reached last November without US participation.

Looking ahead: FOMC Minutes and PMIs

FOMC minutes for December meeting will be a major focus of the day. Fed raised interest rate by the third time last year in December. The biggest difference that time was that Chicago Fed President Charles Evans joined Minneapolis Fed President Neel Kashkari in dissenting. What both have said during the meeting could be something of interest. Other than that, the minutes shouldn’t reveal anything new given that there was a press conference, with new projections released after the meeting.

On the data front, Swiss will release PMI manufacturing while UK will release construction PMI. Germany will release unemployment. US ISM manufacturing will also be a focus and a strong set of number is needed to give Dollar a life.

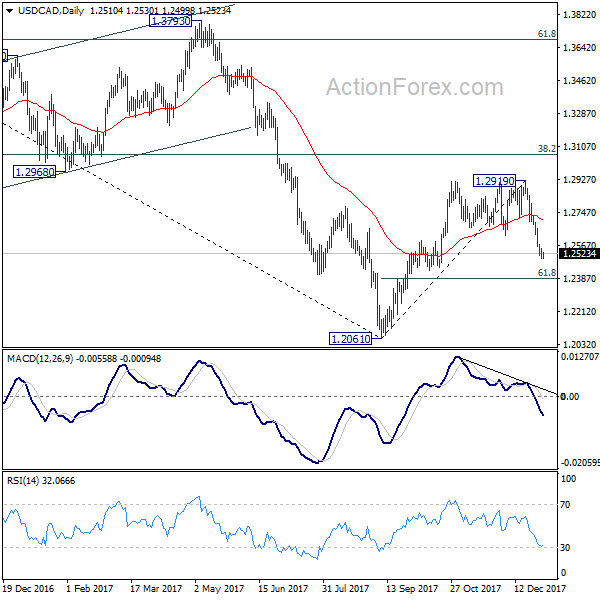

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2482; (P) 1.2528; (R1) 1.2557; More….

USD/CAD drops to as low as 1.2499 so. It’s losing some downside momentum on oversold condition in 4 hour RSI. But intraday bias stays on the downside as long as 1.2566 minor resistance holds. Current fall from 1.2919 would extend to 61.8% retracement of 1.2061 to 1.2919 at 1.2389 or possibly below. On the upside, above 1.2566 will turn intraday bias neutral first.

In the bigger picture, we’re still favoring the case that USD/CAD has defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we’d favor the case that fall from 1.4689 is a correction. With that in mind, fall from 1.2919 is viewed as a correction. Hence, we’re not anticipating a break of 1.2061 low. In the long run, USD/CAD should have another medium term rise to take on 38.2% retracement of 1.4689 to 1.2061 at 1.3065.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 08:30 | CHF | PMI Manufacturing Dec | 64.5 | 65.1 | ||

| 08:55 | EUR | German Unemployment Change Dec | -13k | -18k | ||

| 08:55 | EUR | German Unemployment RateDec | 5.50% | 5.60% | ||

| 09:30 | GBP | Construction PMI Dec | 53.1 | 53.1 | ||

| 15:00 | USD | Construction Spending M/M Nov | 0.50% | 1.40% | ||

| 15:00 | USD | ISM Manufacturing Dec | 58.2 | 58.2 | ||

| 15:00 | USD | ISM Prices Paid Dec | 64.5 | 65.5 |