{kind=link}

Commodity currencies are trading generally higher in Asian session, following the rebound in Asian stocks. Meanwhile, weakness is seen in Dollar, Yen and Swiss Franc. But after all, most pairs are confined by Friday’s range. The economic calendar is light today, also with US on holiday. So, trading will likely be subdued. Nonetheless, the week ahead if packed with some important events, including minutes of RBA, Fed and ECB meeting. The forex markets will come back to life for certain.

Japan exports grew 14th straight months

Japan exports grew solidly by 12.2% yoy in January, above expectation of 10.3% yoy. That’s the 14th straight month of growth, led by 30.8% yoy growth in trade with China. Imports grew 7.9% yoy, below expectation of 8.3% yoy. Trade balance came to a deficit of JPY – 0.94T, smaller than expectation of JPY -1T. But that’s still the first trade deficit in eight months. In adjusted terms, trade balance came in at JPY 0.37T surplus.

EU Verhofstadt: Voting down May’s Brexit deal means crisis

European Parliament’s chief Brexit negotiator Guy Verhofstadt said in a BBC interview that EU was "not against a transition period" regarding Brexit. And he added that "it’s normal that in a transition, you simply continue the existing rules and the existing policies." However, it would be unacceptable to violate the freedom of movement of people principle during the transition. And that would be "penalizing citizens" of the EU. Verhofstadt also warned if the UK parliament votes down Prime Minister Theresa May’s Brexit deal, it could be a "crisis in British politics". And that might lead to a re-election, a new government and a new Brexit position. And in that case, there will be risk of Brexit "without any arrangement".

The week ahead: RBA, FOMC and ECB minutes in focus

Three central banks will release monetary policy minutes this week. RBA minutes will likely just echo the neutral stance of its top officials. Governor Philip Lowe is clear with his messages, RBA won’t follow other global central banks in tightening. A key reason for that is RBA didn’t cut interest rate that deep as others like Fed and ECB. Spare capacity in the economy is expected to keep wage growth subdued. The cool down in housing markets also gives the central some more room to wait, with inflation staying on the lower side of the target band.

FOMC minutes will also likely reaffirm the case for a March hike. Fed fund futures are pricing in over 80% chance of that already. Higher than expected inflation reading in January and solid wage growth is keeping the case for three hikes alive. Indeed, markets are already starting to expect as many as four hikes this year. January FOMC minutes are not expected to alter such expectations.

ECB January minutes will be the more interesting one. There are calls from officials for the central bank to alter its communications. The purpose is to send a clear message that the asset purchase program is coming to an end after September. But so far, ECB didn’t change much in its forward guidance yet. And the markets would like to see what discussions were carried out during the meeting regarding the change in communications.

In addition, there are a number of economic data to watch including Eurozone PMIs, German ZEW and Ifo, UK employment extra. Canadian retail sales and CPI would be particularly watched for gauging the chance of another BoC rate hike in near term.

Here are some highlights for the week ahead:

- Monday: Eurozone current account

- Tuesday: New Zealand PPI; RBA minutes; Swiss trade balance; German ZEW, PPI; Eurozone consumer confidence; Canada wholesale sales

- Wednesday: Australia wage price index; Japan PMI manufacturing, all industry index; Eurozone PMIs; UK employment; US PMIs, existing home sales, FOMC minutes

- Thursday: German Ifo; ECB meeting accounts; UK GDP revision; Canada retail sales; US jobless claims

- Friday: New Zealand retail sales; Japan CPI; Eurozone CPI final; Canada CPI

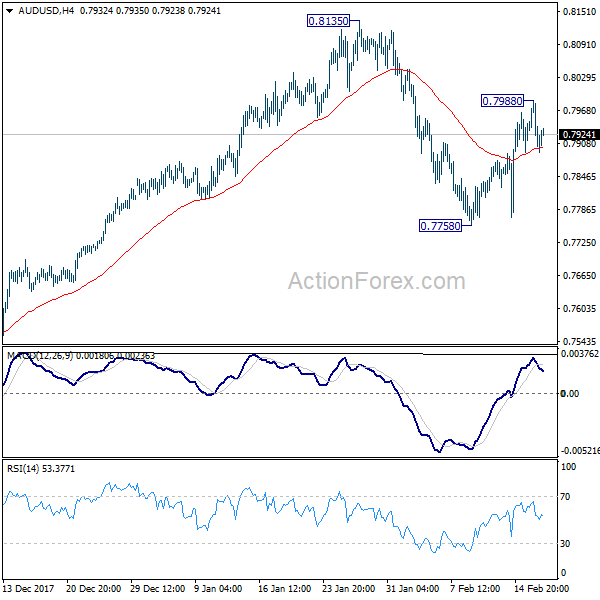

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7902; (P) 0.7934; (R1) 0.7977; More…

AUD/USD recovers mildly today after drawing support from 4 hour 55 EMA. But it’s staying below 0.7988 temporary top. Intraday bias remains neutral at this point. On the upside, above 0.7988 will extend the rebound to retest 0.8135. On the downside, below 0.7758 will resume the fall from 0.8135 and target 0.7500 key near term support. At this point, there is no strong case for a range breakout yet and 0.7500/8135 could hold for a while.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we’d expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Trade Balance Jan | 0.14T | 0.09T | ||

| 00:01 | GBP | Rightmove House Prices M/M Feb | 0.70% | |||

| 09:00 | EUR | Eurozone Current Account (EUR) Dec | 30.5B | 32.5B |