{kind=link}

Last week delivered yet another reminder that volatility has become a feature this year, rather than an exception. Sudden repricing episodes continue to emerge, often driven by political and institutional developments rather than changes in economic fundamentals.

The latest bout of turbulence was triggered by market repricing around the nomination of former Fed Governor Kevin Warsh as the next Federal Reserve chair. The move forced a rapid reassessment of risks that had built up over monthly weeks, unleashing violent adjustments in select corners of the market.

The intensity of the reaction, however, was far from uniform. While precious metals experienced dramatic swings, other asset classes showed far more restraint. Equities and Treasuries largely stayed within familiar ranges, hinting that the shock was narrowly concentrated rather than systemic.

That divergence mattered. It suggested that markets were not questioning the broader economic outlook or the Fed’s near-term policy path, but instead recalibrating around perceived shifts in institutional risk and long-term credibility.

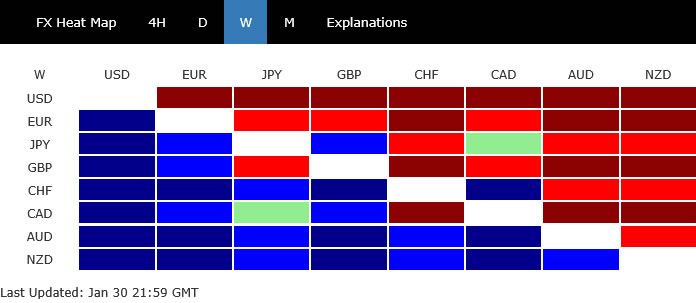

In currency markets, Dollar staged a late-week rebound but still finished as the worst performer overall, followed by Euro and Sterling. At the other end, Kiwi led gains, with Aussie and Swiss Franc close behind. Yen and Loonie ended the week mixed, reflecting cross-currents rather than a clear directional bias.

Gold and Silver Exodus: When the Party Ends

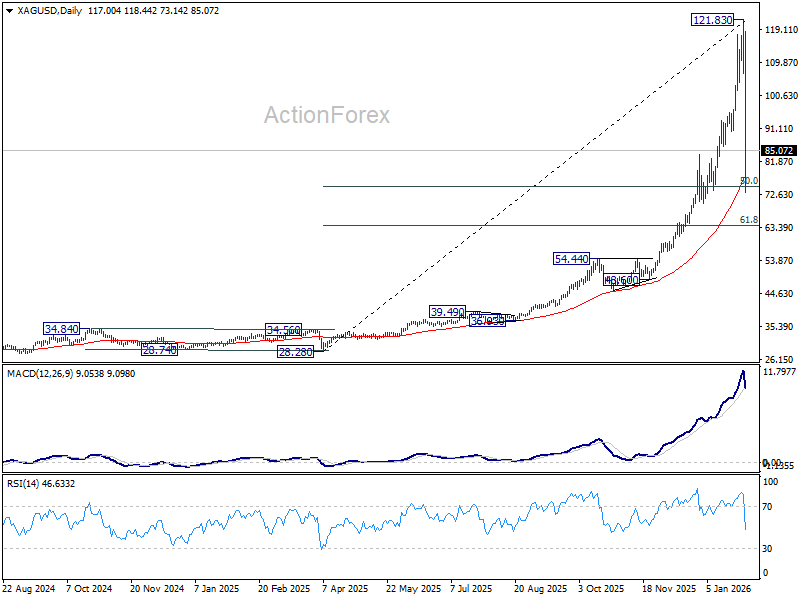

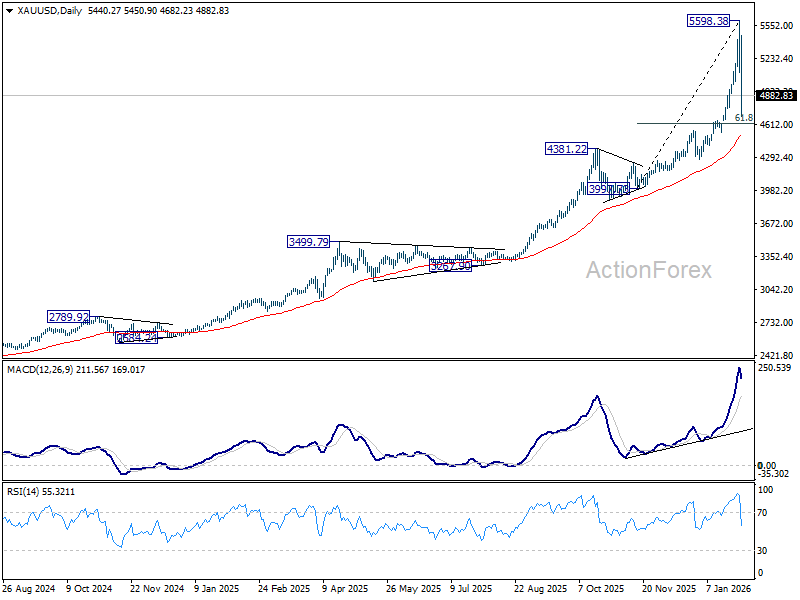

The most dramatic action unfolded in precious metals. Gold and Silver surged to fresh record highs, only to suffer violent reversals that erased weeks of gains in a matter of house. Gold briefly peaked near 5,598 before collapsing to close the week around 4882, a drawdown of more than 13% from the high. Silver’s reversal was even more brutal, plunging from a record 121.81 to 85.07, a decline of roughly 30%. These are classic signs of terminal momentum, not healthy consolidation.

Such price behavior strongly suggests that major tops have been formed. While this does not invalidate the longer-term bullish trend, it does mark the end of the one-way, momentum-driven phase that had defined the previous rallies.

Technically, both metals have now transitioned into a corrective phase. This distinction is critical. Corrections following blow-off tops are rarely clean or directional. Instead, they tend to be prolonged, erratic, and psychologically punishing.

The problem is not just direction—it is structure. At this stage, price action can morph into any number of patterns: flats, zigzags, triangles, or complex combinations. Early in a correction, it is impossible to know which will dominate, making risk-reward unattractive for all but the most tactical traders.

During such phases, short-term speculators take control. Whipsaws become frequent, false breakouts multiply, and both longs and shorts are routinely punished. Trend-following strategies fail, while mean-reversion trades become increasingly unstable.

Fundamentally, corrections also represent a breakdown in narrative clarity. The dominant bullish story—Fed politicization, institutional erosion, currency debasement—has been partially challenged. New information has arrived, but it remains unclear whether it represents a regime shift or temporary noise.

This ambiguity is toxic for positioning. When conviction dissolves, markets no longer reward holding risk. Instead, they reward speed, flexibility, and capital preservation—qualities that most investors do not associate with Gold and Silver exposure.

For professional traders, opportunity may still exist on very short timeframes. But for investors and medium-term participants, the odds are stacked against clean outcomes. Capital can be deployed more efficiently elsewhere while metals reset.

In short, Gold and Silver are not broken, but they are no longer tradable with confidence, not at least in the near term. Until volatility compresses, structures mature, and sentiment stabilizes, the prudent course is to step aside and wait for clarity to return.

Why Warsh Mattered: Experience, Symbolism, and Institutional Lines

The nomination of Kevin Warsh as the next Fed chair was never just about a personnel change. It carried outsized significance because it arrived after weeks of market anxiety over the future independence and credibility of the US central bank.

Warsh is not a newcomer to monetary policy. He served as a Fed governor from 2006 to 2011, spanning the global financial crisis, where he was deeply involved in emergency liquidity measures, bank rescues, and the early phases of unconventional policy. That experience still carries weight in financial circles.

Before joining the Fed, Warsh built his career on Wall Street and in public service, giving him fluency in both market mechanics and policymaking. That dual background has long made him a familiar and generally respected figure among investors, particularly those concerned with institutional continuity.

In the weeks leading up to the decision, markets had focused on Kevin Hassett, the National Economic Council director, as a frontrunner. Hassett’s perceived dovish leanings mattered, but more importantly, his proximity to the White House raised fears of overt political influence over monetary policy.

Those fears had real market consequences. Investors began to price in a more severe erosion of Fed independence, accelerating flows into hard assets and amplifying volatility in Gold and Silver. The assumption was not just easier policy, but a structural shift in how policy decisions would be made.

Against that backdrop, Warsh’s selection was widely interpreted as a line drawn. While he is not immune to political pressure, he is not seen as an extension of the executive branch either. His appointment suggested that there are still boundaries around how far presidential influence over the Fed can stretch.

The symbolism mattered as much as the individual. Rather than installing a close political ally, US President Donald Trump opted for a figure with established Fed credentials and institutional legitimacy. That choice sent a message that continuity, at least in form, still matters.

For markets, this did not mean a reversal of policy direction or an abrupt shift in rate expectations. But it did mean that the most extreme scenarios around politicization were dialed back, helping to stabilize expectations—even if deeper questions about the Fed’s future remain unresolved.

Relief, Not Repricing: What Warsh Did—and Didn’t—Change

Despite the violent reaction in precious metals, the short answer to whether Kevin Warsh’s appointment materially changed the macro outlook is no. Once the initial shock passed, other parts of the market sent a clear signal: expectations around growth, inflation, and monetary policy remain largely intact.

Most tellingly, Fed rate cut pricing barely moved. Futures continue to imply roughly a 60% chance of a 25bp cut by the end of June, little changed from the prior week. If markets believed Warsh marked a meaningful hawkish turn, that pricing would have shifted decisively.

The Federal Open Market Committee’s own behavior reinforced that message. While Stephen Miran and Christopher Waller dissented in favor of a cut at the last meeting, the majority opted to hold rates at 3.50–3.75%, maintaining a cautious, wait-and-see stance. That internal balance remains unchanged.

After delivering three risk-management cuts last year, policymakers appear content to pause and assess incoming data. Inflation has cooled but remains exposed to upside risks, while employment has stabilized rather than weakened decisively. In that environment, urgency to ease further is limited.

Crucially, the Warsh appointment does not remove the wild cards facing the Fed. Rising oil prices linked to Iran instability, renewed trade tensions with the EU and Canada, and the broader geopolitical backdrop all complicate the inflation outlook in ways that argue for caution rather than haste.

Equity and bond markets reflected this realism. US stocks did not break out of established ranges, and Treasury yields continued to trade sideways. There was no confirmation of a regime shift—just selective repositioning.

This contrast with precious metals is important. Gold and silver reacted violently because they were pricing institutional decay scenarios that were partially unwound. Other asset classes, which had not embraced those extremes, had far less to reverse.

In that sense, Warsh’s appointment reduced tail risk, but it did not rewrite the base case. The Fed remains data-dependent, the policy path remains conditional, and markets are still operating in a world where uncertainty—not clarity—dominates decision-making.

DOW and 10-Year Yield Stay Caged

US equities continued to trade within established ranges. DOW struggled to sustain upside traction below the 50,000 psychological level, with price action reflecting indecision rather than conviction.

Technically, the picture is mixed. On the supportive side, DOW is still holding comfortably within its medium-term rising channel and above the rising 55 D EMA (now at 48,316.64), which continues to offer dynamic support and argues against an immediate trend reversal.

At the same time, warning signs persist. Bearish divergence in D MACD remains unresolved, suggesting upside momentum is fading. This divergence limits confidence in any clean breakout and keeps the risk of a corrective phase alive.

For now, the path of least resistance still points higher, with a break above 50,000 marginally favored. But even in that scenario, upside is unlikely to be smooth. Technical resistance is expected near 78.6% projection of 41,981.14 to 48,431.57 from 45,728.93 at 50,798.97 to limit upside.

On the other hand, Decisive break below 55 D EMA would shift the balance more clearly toward a medium-term correction. That level remains the key fault line between continuation and consolidation, and it has yet to be tested convincingly.

Treasury markets told a similar story of restraint. US 10-year yield continued to oscillate in a tight range above 4.200, after briefly spiking to 4.311 earlier in January. There was no sustained follow-through in either direction.

For now, outlook is unchanged that rise from 3.947 is reversing whole fall from 4.629. Further rally is expected as long as 55 D EMA (now at 4.168) holds. Another rise should be seen back to 61.8% retracement of 4.629 to 3.947 at 4.368. Firm break there will pave the way back 4.628 resistance.

Dollar’s Problems Run Deeper Than the Fed: Euro Normalization and Yen Asymmetry

Even with the Warsh appointment reducing some tail risks, Dollar remains vulnerable to forces that extend well beyond Fed leadership. Chief among these are developments in the Euro and Yen, both of which continue to exert structural pressure on the greenback.

In Europe, the debate around a stronger Euro has quietly shifted. What once sounded like fringe speculation—EUR/USD pushing decisively above 1.20—is now being discussed more openly by market participants. That change in tone matters. Acceptance often precedes price. Euro’s resilience is not built on rapid growth, but on relative stability. The ECB has little incentive to aggressively lean against currency strength. As long as that remains the case, Euro appreciation becomes a feature rather than a bug.

From a flow perspective, diversification out of US assets continues to favor Euro. Reserve managers, institutional investors, and long-term allocators are reassessing concentration risk after years of Dollar dominance. That process is slow, but persistent—and difficult to reverse with a single personnel change at the Fed.

Japan presents a different, but equally powerful, challenge to Dollar. The upcoming snap election remains a major wild card, even if Prime Minister Sanae Takaichi is still expected to secure a solid result. Markets have learned the hard way that political certainty should never be taken for granted.

Any unfavorable election outcome—or even a weaker-than-expected mandate—could trigger a sharp selloff in Japanese equities. Such a move would likely unwind the crowded “Takaichi trade,” forcing capital back into Yen at speed.

That matters because Yen strength tends to feed on itself. Equity weakness, falling foreign asset exposure, and hedging demand can combine to produce outsized currency moves that are difficult for authorities to counter quickly.

In that context, Dollar faces a pincer movement. Euro appreciation reflects gradual, structural diversification, while Yen strength would arrive through sudden, risk-driven adjustments. Neither dynamic is easily neutralized by modest shifts in US rate expectations.

Technically, Dollar Index reflects this pressure. The break below 96.21 to 95.55 last week signaled renewed downside momentum. As long as 97.74 resistance holds, the long term down trend is seen as resuming.

The key level is 38.2% projection of 110.17 to 96.37 from 100.39 at 95.11. Decisive break there would prompt downside acceleration through 61.8% projection at 91.86. Nevertheless, firm break of 97.74 will tremendously ease immediate downside risk and bring stronger rebound back towards 100.39.

And more importantly, as mentioned many times before, another fall with downside acceleration would push Dollar Index through the multi-decade channel floor decisively. That, if happen, would confirm that Dollar Index is reversing whole uptrend from 70.69 (2008 low). That should open up further down trend to 90 psychological level and below.