Live Comments

UK GDP misses at 0.1% mom growth, production and construction drag

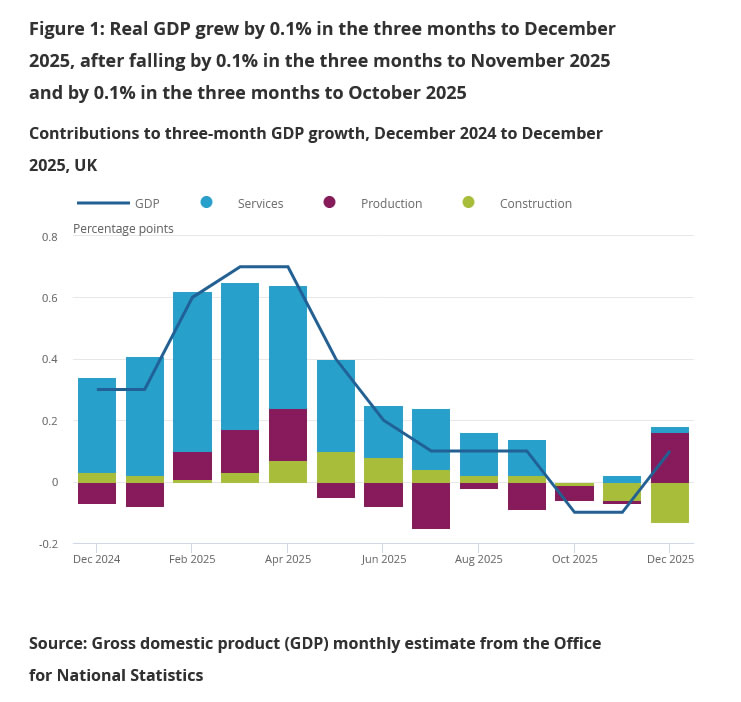

UK GDP rose just 0.1% mom in December, undershooting expectations for a 0.2% gain and pointing to a subdued end to 2025. While services output expanded by 0.3% on the month, weakness in production, which fell -0.9%, and construction, down -0.5%, capped overall growth.

For the fourth quarter as a whole, GDP grew 0.1% quarter-on-quarter compared with Q3. Production output provided the largest positive contribution, rising 1.2%, while services showed no growth and construction contracted sharply by -2.1%.

On a broader basis, GDP expanded 1.0% in the three months to December 2025 compared with a year earlier, with services and production both up 1.0%. Annual GDP growth for 2025 came in at 1.3%, driven primarily by 1.4% growth in services, while production posted its first annual increase since 2021 at 0.2%. Construction grew 1.8%.

Japan PPI eases to 2.3%, but import costs accelerate

Japan’s producer price index slowed slightly to 2.3% year-on-year in January from 2.4%, matching expectations and suggesting pipeline price pressures are stabilizing. The moderation came despite sharp divergences across components.

Fuel prices dropped -12.9% yoy, providing a significant drag on overall wholesale inflation. In contrast, nonferrous metal prices surged 33%, while agricultural goods rose 22.4%. Food and beverage prices also remained elevated, increasing 4.7% from a year earlier, highlighting persistent cost pressures in parts of the supply chain.

Meanwhile, Yen-based import prices climbed 0.5% yoy, up from a 0.2% gain in December. Despite a recent rebound in the currency, Yen’s broader weakness over recent months has raised the cost of imported energy and raw materials.

RBA’s Bullock says inflation above 3% “unacceptable,” keeps door open to more hikes

RBA Governor Michele Bullock reinforced the hawkish stance at a Senate estimates hearing today, making clear that further tightening remains on the table. “If we need to go up further because inflation is entrenched, the board will do so,” she said, stressing that returning inflation to target remains the central bank’s primary mandate.

Bullock said inflation running “with a three in front of it” is unacceptable. She noted that, at present, total demand is judged to be exceeding the economy’s capacity to supply, helping to explain ongoing inflation pressures. At the same time, she struck a more balanced tone on growth, pointing to the labour market as a key "positive". While productivity remains weak and limits how fast the economy can expand, employment conditions are holding up. “We’re in this position because the economy is actually doing okay,” Bullock said,.

The RBA raised the cash rate by 25 bps last week to 3.85%, reversing one of last year’s cuts, after underlying inflation accelerated to 3.4% in the latest quarter. With forecasts pointing to inflation reaching 3.7% this year, markets now price roughly a 75% chance of another hike to 4.10% at the May meeting.