Here are the latest developments in global markets:

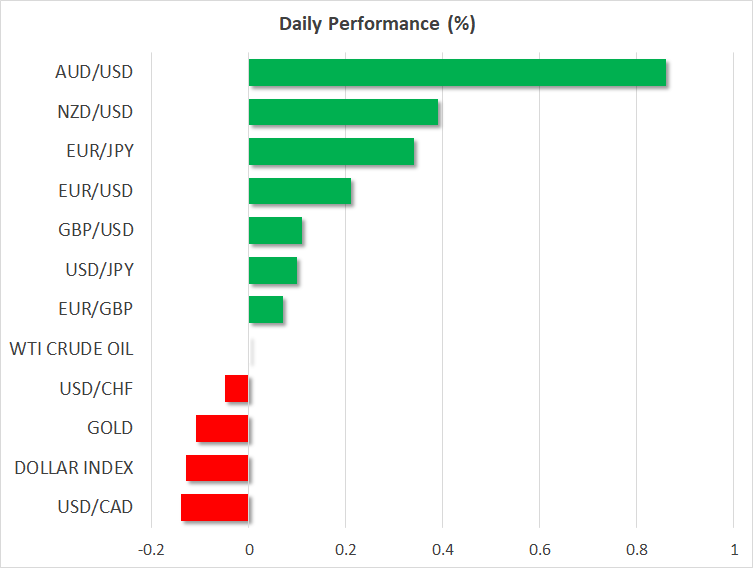

FOREX: The dollar eased a bit versus a basket of currencies on Monday after being boosted on Friday on the back of a largely upbeat US employment report. The aussie was a notable outperformer versus the greenback, being helped by better-than-expected Australian retail sales data.

STOCKS: Wall Street’s major benchmarks closed considerably higher on Friday, with the positive sentiment carrying through to today’s Asian session. The Japanese Nikkei 225 and Topix indices finished higher by 1.4% and 1.5%, while Hong Kong’s Hang Seng was up by 1.5%. Futures markets pointed to a higher open for major European indices, with contracts on the Dow, S&P 500 and Nasdaq 100 also being in the green. Apple, the world’s largest company by market-cap, will be in focus today as its Worldwide Developers Conference in San Jose, California, kicks off; new product offerings are anticipated to be unveiled by the corporation.

COMMODITIES: WTI was flat at $65.84/barrel, while Brent crude traded 0.2% down at $76.66/barrel. Overall, the two oil benchmarks experienced significant declines in recent days on what is perceived by market participants as rising prospects of higher world supplies. Turning to gold, it was 0.1% down at around $1,291/ounce, building on Friday’s losses which came on the back of a stronger dollar.

Major movers: Dollar higher versus the yen, though trade risks loom; aussie jumps

At 0659 GMT, the dollar index was trading 0.15% lower, while dollar/yen was 0.1% up at 109.65, after adding 0.6% on Friday. The robustness of Friday’s jobs report out of the US almost completely eliminated any uncertainty regarding the delivery of a 25bps interest rate hike by the Fed when it meets later in June and increased the odds for four interest rate increases in total during 2018.

Trade uncertainty as the US get more confrontational with China, but also other traditional allies such as the EU and Canada, will be monitored in the days to come as it has the capacity to divert funds out of the dollar and into safe havens, including the yen.

Euro/dollar was 0.2% up and not far below the 1.17 handle. The situation has cleared in Spain – which either way was not really perceived as a major risk – while a first line of uncertainty was removed in Italy as well; the latter acted as the catalyst for some notable euro-gains last week. Now, it remains to be seen what type of policies the anti-establishment parties which have come to power in Italy will follow. Will they play by the “rules of the game”, something which is expected to be perceived as euro-friendly by markets, or will they attempt to shake things up?

Sterling, which was helped by stronger-than-anticipated manufacturing PMI data on Friday, was 0.1% up, having reached a 10-day high of 1.3377 earlier in the day.

In the antipodean sphere, aussie/dollar was a notable gainer today. Specifically, the pair traded higher by more than 0.8% and not far below a six-week high 0f 0.7631 touched earlier in the day. Strong company profits and a retail sales beat were the reasons behind the aussie’s advance. Meanwhile, the NZD was also boosted, with kiwi/dollar being up by 0.4%, close to Thursday’s four-week high of 0.7023.

Day ahead: Eurozone’s Sentix due; trade developments at the forefront

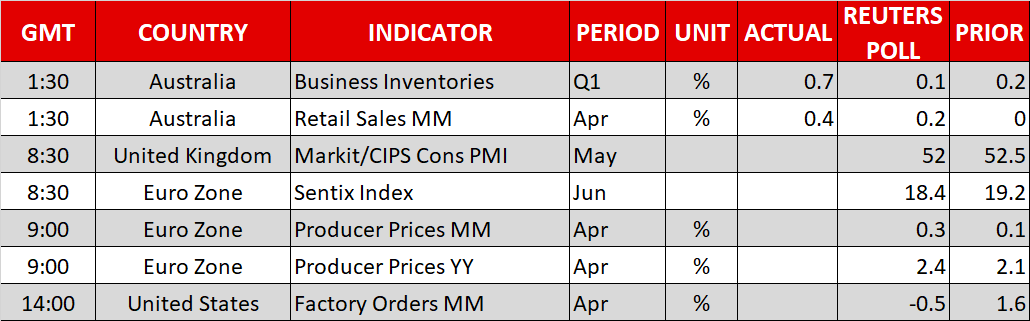

Early in the European session, data out of the eurozone will attract some attention as political risks in Italy have somewhat calmed down after the anti-establishment parties 5-Star Movement and League managed to reach an agreement on forming a coalition government last week.

At 0830 GMT, Eurozone’s Sentix Investor confidence index for the month of May is expected to ease from 19.2 in April to 18.4, hitting the lowest level since February. In contrast, producer prices out of the region due at 0900 GMT are projected to grow faster in April, with analysts seeing an expansion of 2.4% y/y compared to 2.1% in March. Meanwhile, the UK will be on the receiving end of construction PMI data for May at 0830 GMT, one day ahead of the much more important for the UK economy services PMI print.

US factory orders for April are due at 1400 GMT; a month-on-month contraction in orders is expected.

Trade uncertainty is a theme that is expected to dominate market attention in the days to come. Note that on Thursday US President Donald Trump decided to impose tariffs on steel and aluminum imported from the EU, Canada and Mexico. Trump’s move saw immediate countermeasures from Canada and Mexico, the US’s NAFTA partners, while the EU has also threatened to retaliate, with all three countries filing complaints at the World Trade Organization. In the meantime, any updates on the US-China trade spat will also be closely watched by markets. The US export-promoting team led by the Commerce Secretary Wilbur Ross failed to make progress in meetings with Chinese officials over the weekend. Lastly, rising global trade risks are also expected to be discussed on a G7 meeting in Quebec later this week.

As for today’s public appearances, German Chancellor Angela Merkel and Israeli Premier Benjamin Netanyahu will be holding a joint news conference after discussing relations between Israel and Iran (1430 GMT), while at 1700 GMT Bank of England Member of Monetary Policy Committee Silvana Tenreyro will be making comments.

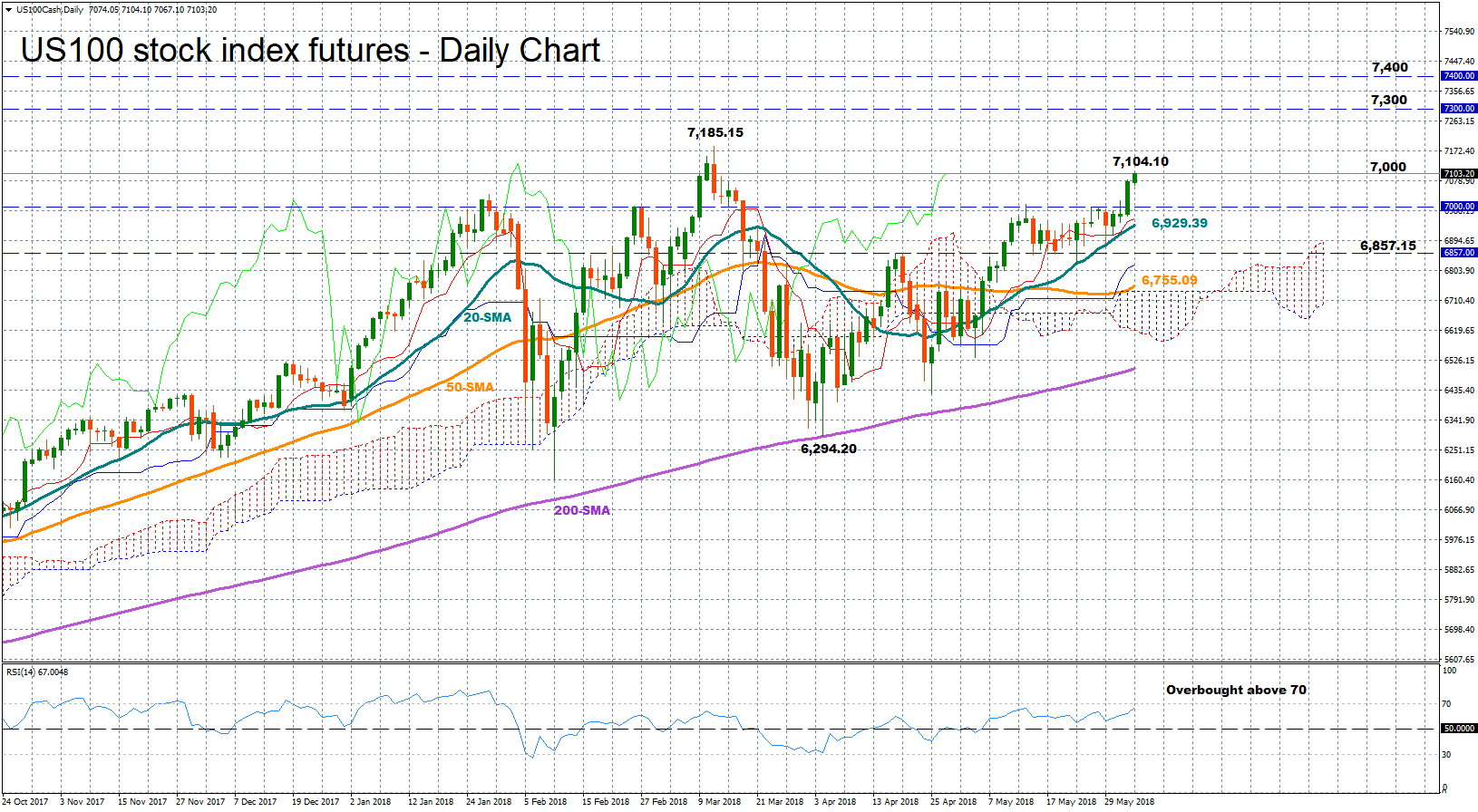

Technical Analysis: US 100 stock index bullish at 2½-month highs

The US 100 stock index (NASDAQ 100) has been running bullish after it found support at the 200-day simple moving average (SMA), unlocking a fresh 2½-month high of 7,104.10 during pre-US market trading. Price action above its SMAs and with the red Tenkan-sen line holding above the blue Kijun-sen line, the uptrend off April’s trough of 6,294.20 could stay in place in the short-term.

The market could also retain positive momentum in the near-term as long as the RSI is positively sloped above its neutral threshold of 50. Yet, downside corrections cannot be excluded as the indicator is edging closer to overbought territory, above 70.

Should the price extend higher, traders could look for resistance around the record high of 7,185.15, while a significant break above that level could open the way towards the 7,300 key-level and at the same time turn the medium-term outlook into a more conclusively bullish one.

Conversely, a move lower could meet support between the 7,000 key-mark and the 20-day SMA currently at 6,929.39; this was a previously congested area. Even lower, the attention could turn to April’s peak of 6,857.15, before the focus shifts to the area around the 50-day SMA at 6,755.09.

{kind=link}