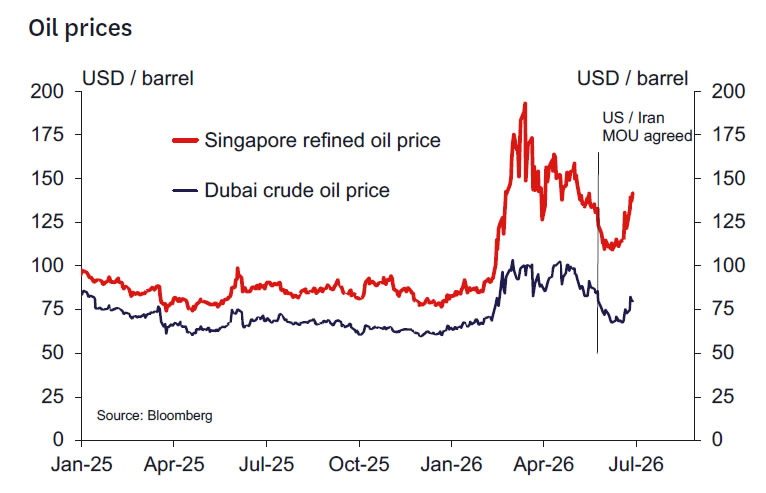

- With the war in the Middle East pushing oil prices sharply, consumer price inflation is set to rise to a two-year high.

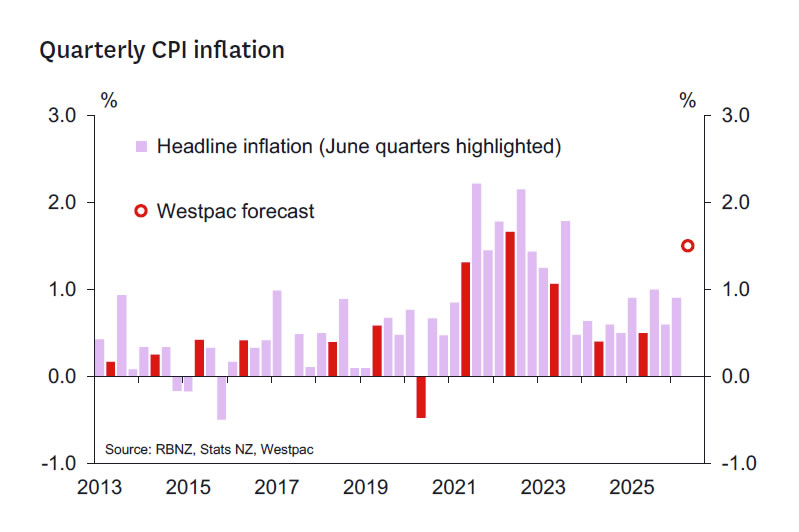

- We estimate that New Zealand consumer prices rose by 1.5% in the June quarter. That’s slightly higher than our previous forecast, consistent with the firmer than expected increases in prices for volatile items like holiday accommodation in Stats NZ’s June update.

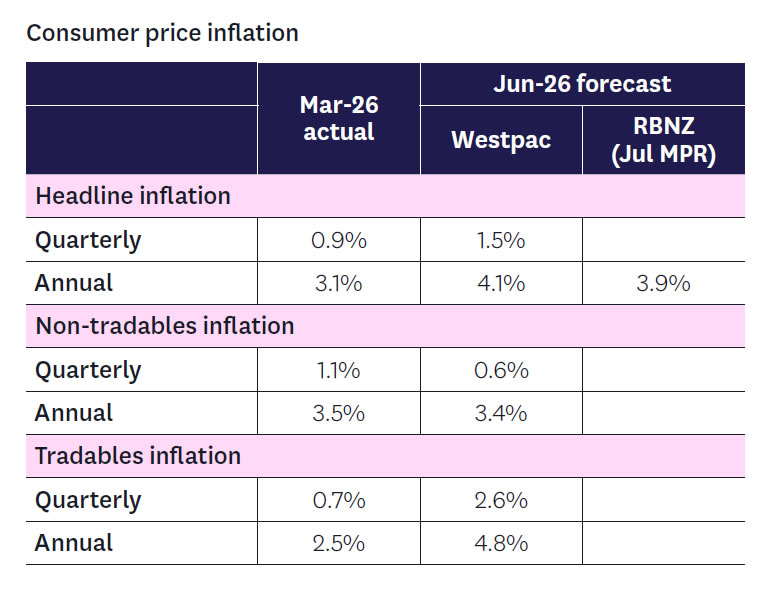

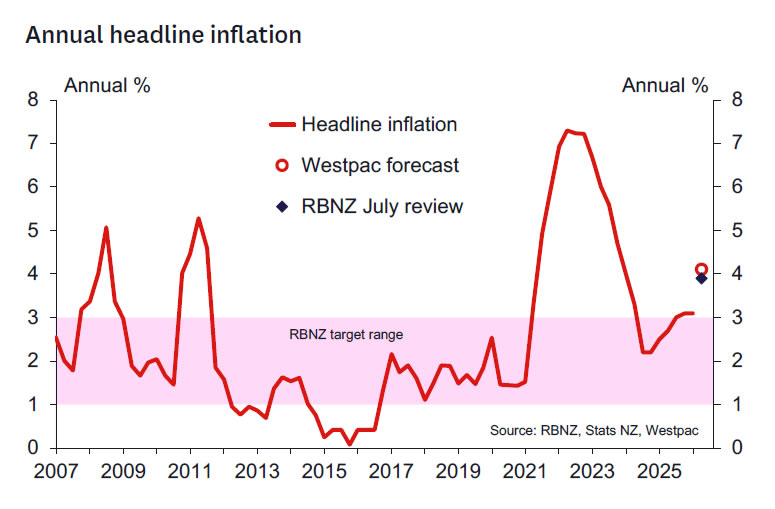

- The annual inflation rate is expected to rise to 4.1% (up from 3.1% previously).

- Core inflation has been softening but remains above the RBNZ’s 2% target midpoint. That’s despite the downturn in economic growth and softness in the labour market.

- Our forecast is close to the RBNZ’s updated forecast for 3.9% annual inflation.

We expect the June quarter inflation report (out on 21 July) will show that New Zealand consumer prices rose 1.5% over the past three months. That would see the annual inflation rate rising to 4.1% – up from 3.1% in the year to March and the highest level in two years.

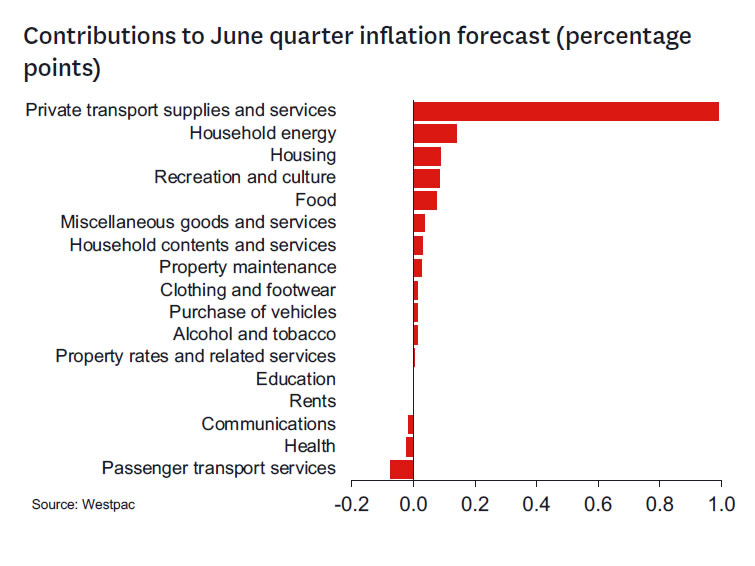

The main driver of June’s spike in consumer prices has been the sharp rise in fuel prices since the start of the Middle East war. While prices have dropped in recent weeks, petrol prices have risen 20% over the June quarter and diesel prices were up an eye-watering 51% (together, those costs account for around 4% of the CPI).

Recent months have also seen further large increases in household energy prices (3% of the CPI). Electricity prices rose 4% over the June quarter and are up 12% over the past year. Similarly, household gas prices rose 2% over the quarter, leaving them up 11% over the past year.

Also adding to inflation has been the 0.4% rise in food prices over the quarter (18% of the CPI).

Oil Spill(overs)

With a sharp rise in energy prices, many businesses have reported large increases in other operating costs, including transportation and materials. For instance, in the construction sector, the cost of PVC piping and other inputs rose sharply in recent months. Consistent with that, we expect the cost of building new home (which makes up close to 10% of the CPI) to take a step higher this quarter after muted gains over the past year.

But while production costs have been rising, soft demand has been a brake on many businesses’ ability to pass those higher costs through into output prices. That will limit the rise in overall consumer prices but does mean continued pressure on businesses’ margins.

The risk that increased fuel costs spillover into broader inflation pressures is a significant concern for the RBNZ. With that in mind, measures of core inflation will be a key focus. (Note: core inflation measures smooth through the large quarter-to-quarter swings in individual prices and instead track the underlying trend in inflation). In terms of specifics, we expect:

- CPI ex-fuel inflation: +2.8% yr (vs +3.2% previously)

- CPI ex-fuel and food: +2.9% yr (vs +3.0% previously)

- CPI ex-fuel, food and household energy: +2.5% yr (vs +2.6% previously)

- 30% trimmed mean: +2.4% (vs +2.3% previously)

Although the various measures of core inflation have been dropping back, we’re reluctant to describe them as ‘low.’ Despite a sharp slowdown in economic growth and softness in the labour market, the various measures of core inflation have lingered above the 2% midpoint of the RBNZ’s target range for an extended period. And with the recent oil related lift in inflation pressures, recent business surveys point to the risk of at least a temporary broader lift in inflation over the coming months.

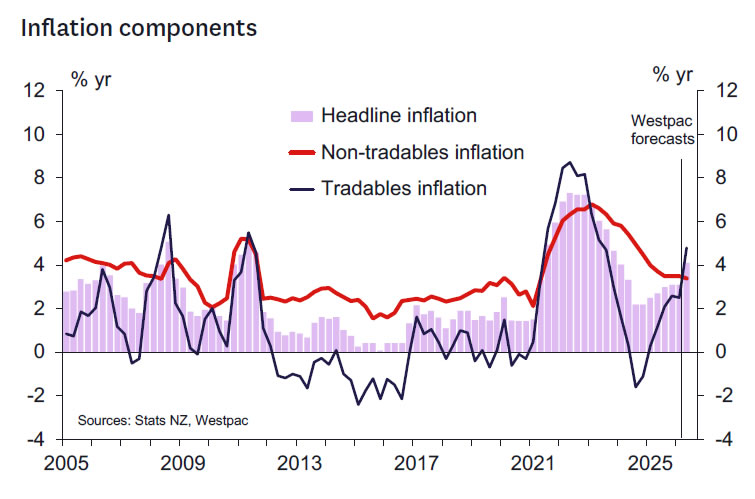

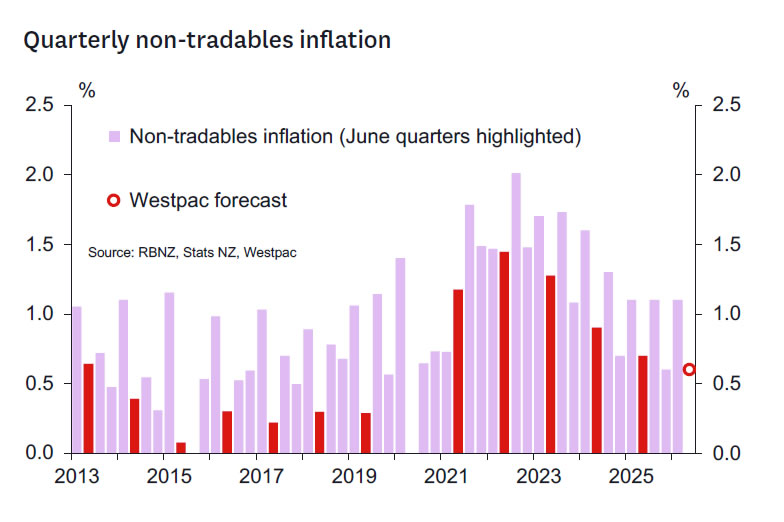

Much of the firmness in core inflation has been due to increases in domestically oriented non-tradables prices. We expect these prices will rise 0.6% over the quarter. That would see annual non-tradables inflation softening to 3.4%, down from 3.5% last quarter but still well above average levels. Much of that strength has been related to continued large increases in administered prices, like council rates and electricity.

Bucking that trend of general firmness in non-tradeable prices, however, has been notable softness in housing rents (11% of the CPI). With abundant supply and low population growth, average housing rents have shown no growth since late last year, and regions likely Wellington have seen outright falls.

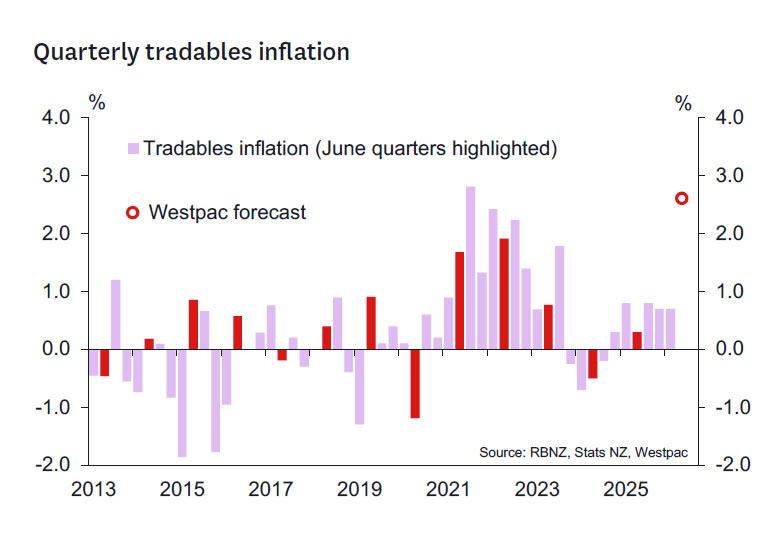

On the imported front, higher fuel costs are expected to see tradables prices rising by a huge 2.6% over the quarter. That would result in annual tradables inflation rising from to 4.8% from 2.5%yr previously. But while higher fuel costs have been a significant driver of the rise in imported inflation, the lower New Zealand dollar is also playing an important role. Excluding food and fuel costs, we estimate that tradables prices were up 3.2% over the past year. The average value of the trade-weighted exchange rate (TWI) in the June quarter was almost 4% lower than a year earlier.

How Do Our Forecasts Compare to the RBNZ’s Assumptions?

Under the direction of new Governor Anna Breman, the RBNZ has made efforts to strengthen it communications. That includes the releases of addition information and forecasts updates at its interim policy reviews (previously, such information was only released when the more detailed quarterly Monetary Policy Statements were released). This has been very welcome move from the RBNZ, especially given the significant and rapid changes in the global economic backdrop in recent weeks.

The RBNZ’s July update show inflation peaking in the year to June at 3.9%. The RBNZ didn’t publish a quarterly inflation track in July, but we estimate that their annual forecast is consistent with a 1.4% quarterly rate in consumer prices.

Our forecast for a 4.1% rise in consumer prices is slightly higher than the RBNZ’s expectations. However, given the rapid changes in the economic outlook over the past few weeks and related uncertainty about the outlook, a result in line with our forecast would not be a major surprise to the RBNZ.

However, even if the overall inflation result is close to forecasts, the underlying detail will be a key interest. The RBNZ will be watching closely for signs that high fuel prices are spilling over into other prices, especially with global oil prices taking another step higher recently. With that in mind, the strength of the various core inflation measures will be a key focus for the RBNZ.

Updates from the June Selected Price Report

Our updated forecast for a 1.5% rise in consumer prices in the June quarter is slightly stronger than our previous forecast for a 1.4% rise. That reflects updated data from Stats NZ’s June Selected Prices report. Of note, June saw a larger than expected increases in the volatile holiday accommodation category. That more than offset a more modest than expected rise in electricity prices.

In the other big categories, food prices were up 0.6% over the month as expected. Housing rental growth remained very muted, rising just 0.1% over the month.

will show that New Zealand consumer prices rose 1.5% over the past three months. That would see the annual inflation rate rising to 4.1% - up from 3.1% in the year to March and the highest level in two years.){kind=link}