Here are the latest developments in global markets:

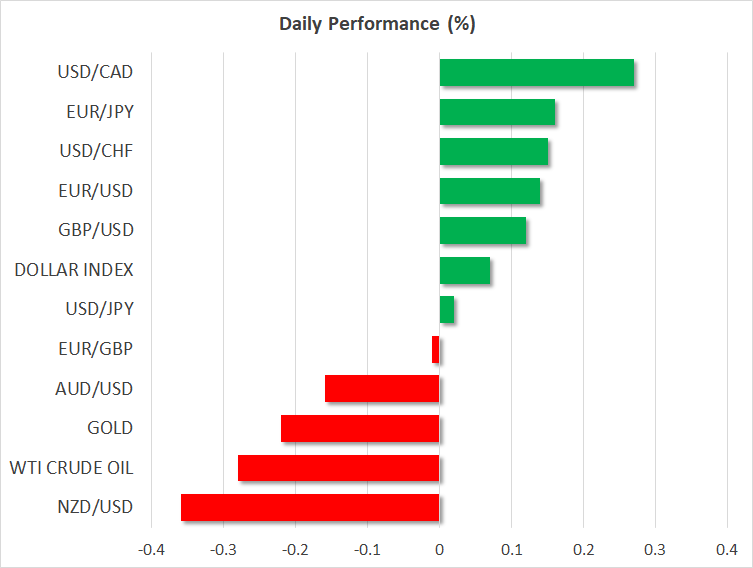

FOREX: The euro edged higher by 0.26% versus the US dollar on Friday but was set to post its biggest weekly loss in 19 months after the European Central Bank (ECB) signaled it will keep rates at record lows until late 2019, pushing euro/dollar down by more than 250 pips at one point on Thursday. Meanwhile, Eurozone’s final CPI readings for May were in lie with preliminary estimates, with ECB member, Ewald Nowotny, saying that the central bank’s inflation target of just below 2.0% is close to be achieved. Sterling started the day in negative territory amid rising Brexit tensions, challenging $1.3210 but managed to move higher later, gaining 0.11% against the greenback. Dollar/yen was flat at 110.65, below the almost one-month high of 110.89 reached earlier after the Bank of Japan (BOJ) kept its policy unchanged but downgraded its assessment on inflation earlier on Friday. Meanwhile, the US dollar index reached a 7-month high of 95.13 before it slid to 94.87 (+0.11%). Trade uncertainties continued to weigh on the greenback as the EU backed a retaliatory plan against US import tariffs on Thursday, while India also joined later on, announcing potential countermeasures on US goods. In the antipodean sphere, aussie/dollar touched a 1-month low of 0.7450 today, falling by 0.20%, while kiwi/dollar dived by 0.43% to 0.6952. Dollar/loonie rose by 0.34% towards a new 1-year high of 1.3153.

STOCKS: European equities were heading downwards on Friday at 1120 GMT, with the French CAC 40 which was up by 0.17% underpinned by gains in the healthcare sector being the exception. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were down by 0.41% and 0.44% respectively, with financials losing the most. The German DAX 30 dropped by 0.31% and the Italian FTSE MIB declined by 1.14%. The British FTSE 100 was in negative territory as well, losing 0.77%, while the Spanish IBEX 35 dived by 1.16%. Futures tracking US stock indices were flashing red, pointing to a negative open.

COMMODITIES: Oil prices retreated on Friday before the OPEC meeting in Vienna on June 22 on rising prospects of increased supply in the market. West Texas Intermediate (WTI) crude oil dipped by 0.27% to $66.71 per barrel, while London-based Brent plummeted by 1.04% to $75.15 per barrel. In precious metals, gold pulled back from a 1-month high of $1,309.30 reached yesterday to $1,299.05/ounce (-0.27%).

Day ahead: Trump to reveal list of Chinese goods that may face tariffs; US industrial production pending

Later on Friday, all eyes will turn to the US, where the White House is expected to announce the final list of Chinese products that could be subject to a 25% tariff, a move that could further deteriorate the trade relations between the world’s two largest economies. Today a Chinese foreign ministry spokesman warned that Beijing will void all US-China trade talks if the US pushes forward with tariffs. Meanwhile on Thursday, the IMF director Christine Laggard expressed her opposition to the US actions on trade as well, saying that the measures “are likely to move the globe further away from an open, fair and rules-based trade system, with adverse effects for both the US economy and for trading partners”.

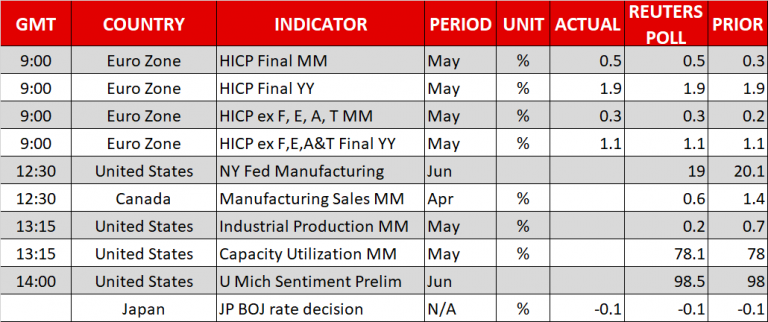

Besides trade headlines, investors will also pay attention to US industrial production trends due at 1315 GMT. The numbers are expected to show a weaker growth of 0.2% m/m in industrial output in April compared to a 0.7% expansion in the previous month; manufacturing output data are also of significance. Earlier at 1230 GMT, the New York Fed is anticipated to indicate a slowdown in its Empire State Manufacturing Index, whereas, at 1400 GMT, June’s preliminary reading for the University of Michigan Consumer Sentiment Index is forecasted to improve by 0.5 points to 98.5.

Elsewhere, manufacturing sales in Canada are projected to post a slower increase for the third consecutive month, with the gauge expected to ease from 1.4% m/m to 0.6%.

In energy markets, the Baker Hughes company will report on US oil drilling activity at 1700 GMT, possibly bringing another wave of volatility to oil prices. Note that the number of active oil drills has been rising since March 29 and another tick to the upside could potentially put the market under pressure once again.

Brexit news will be of greater importance in the UK ahead of the Bank of England’s policy meeting next week. Despite Theresa May’s withdrawal bill getting a winning vote on amendments at the House of Commons on Tuesday, a few days later the chancellor, Philip Hammond, claimed that the amendment published on Thursday was not consistent with what had been promised by May.

As for today’s public appearances, Dallas Fed President Robert Kaplan (non-voting FOMC member in 2018) will be speaking before a business leaders luncheon hosted by the Fort Worth Chamber of Commerce at 1730 GMT.

On Monday, Japanese trade figures will gather some interest during the Asian trading session. Analysts expect Japan’s trade balance has turned negative in May, declining from a surplus of 626 billion yen in April to a deficit of 235bn.