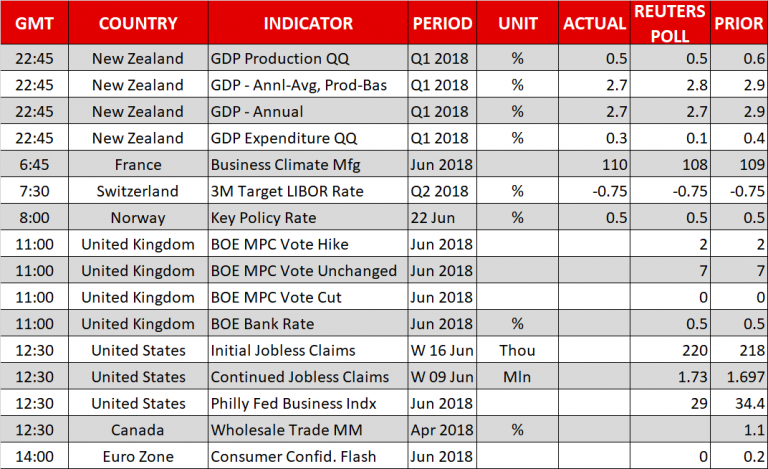

Here are the latest developments in global markets:

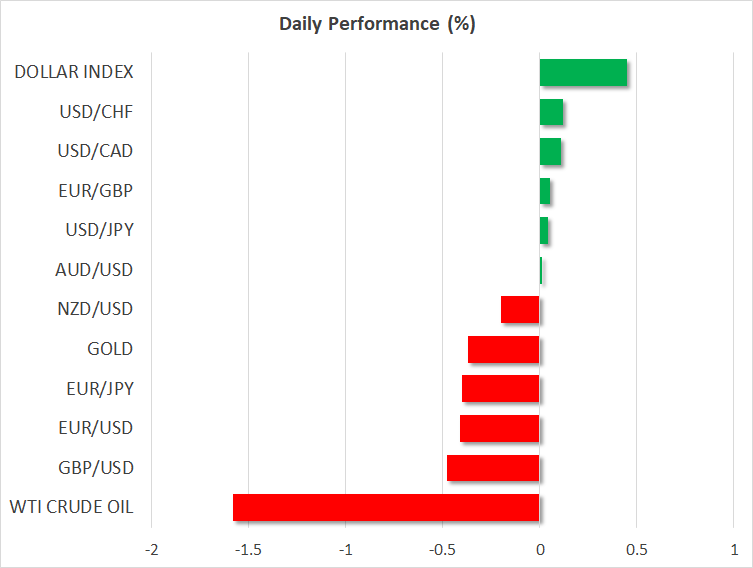

FOREX: Dollar/yen lacked direction for a third day, moving sideways around 110.40 (+0.05%), while the dollar index hit a fresh 11-month high at 95.52 (%?), advancing on the back of a weaker euro and pound. Earlier in the day, US 10-year government bond yields had spiked to a 1-week high of 2.95% but they soon returned to 2.91%. Euro/dollar was in pain as trade uncertainties remained in the air, while in Italy, Eurosceptic Alberto Bagnai, was appointed as the new head of the Senate finance committee, with the pair dropping further to a 3-week low of 1.1507 (-0.40%). Pound/dollar extended its downtrend marginally below 1.31 for the first time since mid-November ahead of the BoE policy decision today. Yesterday, Theresa May’s Brexit bill, was approved by theParliament, easing risks to May’s leadership and bringing a no-deal Brexit deal back on the table in case of no progress in Brexit talks. In antipodean currencies, kiwi/dollar crawled down to a 6-month low of 0.6823 (-0.28%) as economic growth in New Zealand slowed down, as expected, in the face of a weaker consumer spending.Aussie/dollar held steady today at 0.7366. The commodity-linked dollar/loonie reached a new 1-year peak at 1.3329 (+0.09%).

STOCKS: European stocks were mixed at 0830 with the British FTSE 100 being the best performer (+0.32%) and the Italian FTSE MIB being the worst one (-0.80%) as the Italian 10-year bond yields jumped higher. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 inched up by 0.05% and by 0.18% respectively, with consumer non-cyclicals and healthcare sectors leading the gains. The German DAX 30 fell by 0.40% after the German carmaker Daimler signaled that US import tariffs on Chinese products are a threat to its profits. France’s Peugeot and the auto supplier Valeo faced headwinds, as well as trade risks, were looming in the background, sending the French CAC 40 down by 0.19%. In Asia, benchmark stock indices closed in negative territory, while in the US, futures tracking the major indices were flashing red as well, pointing to a negative open.

COMMODITIES: Oil prices were under pressure a day before OPEC members and their allies including Russia meet in Vienna to review the supply cut agreement signed in December 2016. Saudi Arabia and Russia continued to support that a supply hike is necessary, with the Saudi Arabian energy minister saying on Thursday that demand could heighten in the second half of this year and OPEC would negotiate how much to increase output, noting that 1 mb/d is a good target. On the other hand, Iran, remained in the opposite side, arguing that OPEC should reject US proposals to raise supply – though the nation did show some willingness to compromise on a supply increase. Meanwhile, Russia’s Rosneft, one of the world’s biggest oil producers, said that a 1.5 mb/d rise in global production is needed to offset global shortages. WTI crude and the London-based crude were last seen at $64.56/barrel (-1.75%) and at $73.23/barrel (-2.02%) respectively. In precious metals, gold extended losses for the fifth day, retreating to a six-month low of $1,261.36 (-0.38%).

Day Ahead: Bank of England decides on rates; US initial jobless claims pending

The main event of the day is the Bank of England (BOE) interest rate decision at 1100 GMT, where no change in the 0.5% benchmark rate or QE are widely anticipated. Investors will turn their attention to the statement and minutes for guidance, which will be of interest following a run of overall disappointing data so far in Q2 from April and May. Moreover, traders will be watching for any notable changes to the Monetary Policy Committee’s (MPC) members’ in the statement for any clues as to whether a rate hike is possible in August.

Out of the US, weekly jobless claims – initial and continued – due at 1230 GMT will be gathering attention. The number of initial benefits claimants for the week ending June 16 is anticipated to be 220k, little changed from the preceding week’s 218k.

Canadian wholesale trade data for the month of April are scheduled for release at 1230 GMT.

A survey from the European Commission’s Directorate General for Economic and Financial Affairs covering the whole of the euro area will release June’s flash consumer confidence. It is scheduled for release at 1200 GMT and projections are for a dip in consumer confidence to 0.0 from 0.2 before.

In terms of public speeches, the Governor of the Bank of England, Mark Carney will give a speech at the Lord Mayor’s Bankers and Merchants Dinner, at Mansion House, London.

Overnight, Japan will release its CPI figures for May. Expectations are for the inflation rate is to fall to 0.3% in yearly terms, from 0.6% in the preceding month.