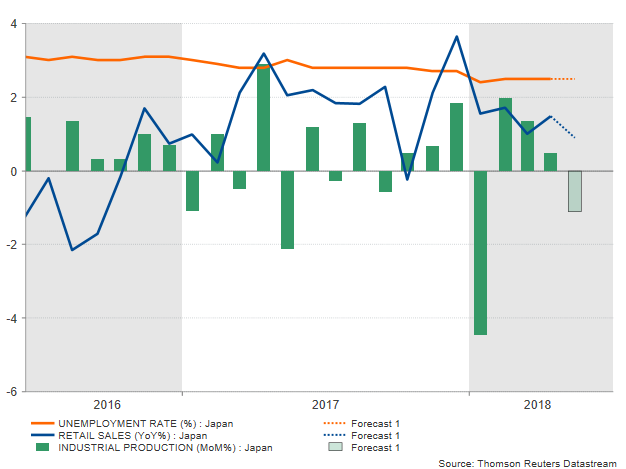

While the safe-haven Japanese yen tends to be less sensitive compared to other currencies when data releases come out of the calendar, updates on economic measures out of Japan can improve or deteriorate investors’ sentiment on the economy. On Thursday, Japan will issue readings on retail sales, while late on Friday employment and industrial production figures will also come under the spotlight. However, the numbers are not expected to show improvement, with labor stats projected to remain unchanged, while retail sales and flash industrial production forecasted to ease.

On Friday (Thursday at 2330 GMT), the Statistics Bureau is expected to say that its labour survey for the month of May was no different to April’s report as analysts believe that the unemployment rate stood flat at 2.5% for the third consecutive month, the lowest in 25 years, while the jobs-to-application ratio held at 1.59, at the highest since 1974. While both figures indicate that the Japanese labor market remained tight despite GDP growth estimates for the first quarter of the year falling to negative territory, recent evidence on wages showed that growth in cash earnings in April narrowed sharply. In fact, payments almost halved, easing from a multi-year high of 2.0% expansion to 0.8% over the year to hint that inflationary pressures are nowhere near to heating up. Household spending supported this view as well when April’s numbers dropped surprisingly by 1.3% y/y, recording the second straight month of losses. Retail sales – a proxy for consumer spending – due on Thursday (Wednesday at 2350 GMT) are anticipated to continue this narrative, showing that sales at the retail level have expanded by 0.9% y/y in May compared to 1.5% in the preceding month.

Meanwhile, on the supply side, production in the industrial sector, where export activities are mostly concentrated, is forecasted to have weakened even further in May according to initial monthly estimates. Particularly, forecasters anticipate the gauge to post a strong pullback of 1.1% m/m after inching up by 0.5% in April. This would be the first decline since the 6.8% sharp downfall in March.

In the meantime, inside the Bank of Japan, policymakers believe that the economy which contracted by 0.6% on an annualized basis in the first quarter of the year, will return to positive territory, attributing the weakness to temporary factors such as the unusually bad weather according to June’s BoJ summary of opinions. Having said that, they still insist that monetary policy should remain accommodative with interest rates remaining below zero, in hopes inflation will continue its broken uptrend towards the BoJ price target of 2.0% despite removing the timeframe for achieving its price goal at April’s policy meeting and downgrading their view on inflation earlier this month. However, with Japanese factories, especially in the growth-driving automobile sectors, facing threats from the US import tariffs on steel (25%) and aluminium (10%) in effect since June 1, the BoJ will likely hold off from winding down its stimulus even if its US and UK counterparts continue to deliver higher rates and its EU peers announcing the termination of their asset purchases program this year. Risks are also stemming from the escalating US-China trade war given that China is Japan’s biggest export destination and any trade restrictions weakening Chinese purchasing power could limit demand for Japanese products. Nevertheless, Japan might face a smaller negative impact than other tariff-affected countries due to their high-quality products which export partners might face difficulty to replace.

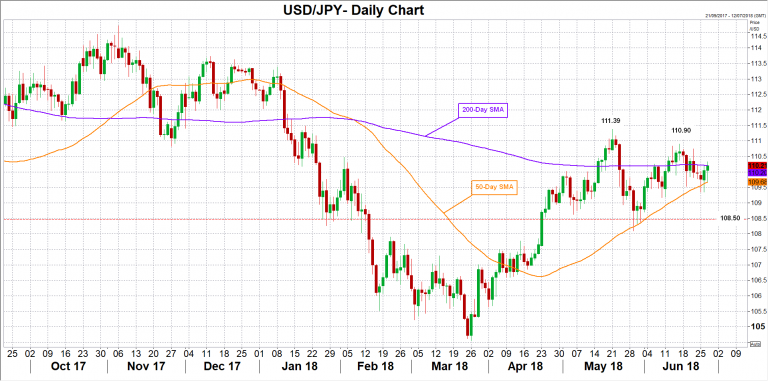

Turning to forex markets, the safe-haven yen, which tends to hardly respond to data releases, has been somewhat gaining on the back of rising tensions in the trade sphere over the past two weeks. In the wake of the above data the yen might not see big changes but a big positive surprise in the numbers – especially in the industrial production front – could increase optimism that economic growth could return to positive territory in the second quarter, increasing buying interest for the yen. In this case, dollar/yen could shift lower towards the 50-day MA at 109.68, which the market was unable to break since mid-April. Even lower, the 109 round-level could come into view, while in case of steeper declines, bears could also eye the area around 108.50, where the market stopped in previous months.

On the other hand, a deterioration in the measures could send dollar/yen towards June 15 peak of 110.90, while any step above this level could open the way towards May 21 high of 111.39.

On Friday (Thursday 2330 GMT) , Tokyo CPI readings for the month of June will attract some attention too as it will be another guide to inflation prospects after the more important to BoJ nationwide core CPI stood flat at 0.7% in May as expected.

{kind=link}