Here are the latest developments in global markets:

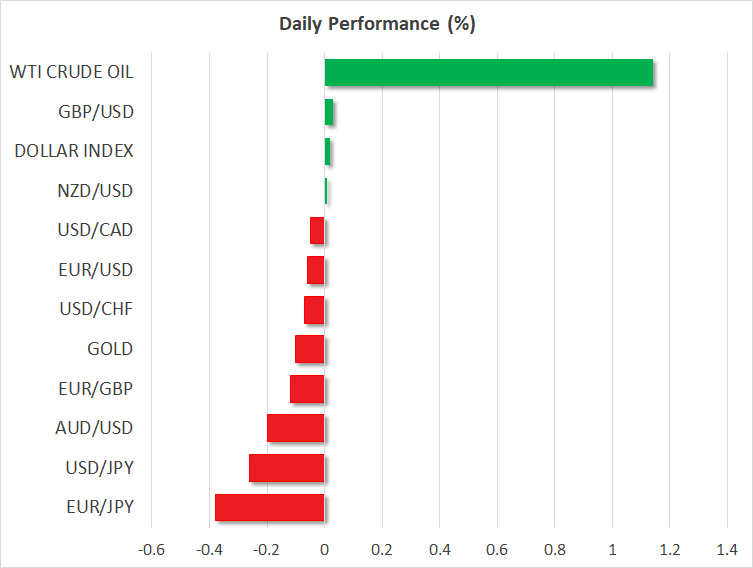

FOREX: The US dollar edged sharply lower over the last three straight days against the Japanese yen as the movements were based on reports the Bank of Japan (BOJ) is discussing changes to its monetary policy, including changes in interest rates and stock buying techniques. The 10-year yield in Japan climbed as much as six basis points to 0.090%, hitting the highest level since February. Dollar/yen continued the bearish move today as well, losing 0.25%. However, the US dollar index advanced by 0.04%, erasing some previous losses. Pound/yen retreated to a 3-week low (-0.24%), while pound/dollar moved up by 0.04%. In Brexit-related news, the new British foreign minister, Jeremy Hunt, said on Monday that there was a real risk of a no-Brexit deal if the EU waited too long for Britain to “blink” Also, euro/yen dipped by 0.36% and euro/dollar fell by 0.08%. In the antipodean sphere, aussie/dollar slipped by 0.19% near 0.7400, while kiwi/dollar stood near its opening level at 0.6806. Meanwhile, dollar/loonie fell marginally by 0.07% after another strong sell-off day on Friday.

STOCKS: European stocks were in the red on Monday. The benchmark European STOXX 600 dived by 0.20% at 1100 GMT as travel companies were the biggest losers after Ryanair posted a 20% decline in first-quarter profit. The blue-chip Euro STOXX 50 was down by 0.33%, while the German DAX 30 fell by 0.30% after two consecutive negative days. The French CAC 40 and the British FTSE 100 were down by 0.55% and 0.37% respectively, while the Spanish IBEX 35 moved lower by 0.28%. In Asia, Japan’s Nikkei 225 closed down by 1.33% after reports said that BOJ is looking to pull back on stimulus. In the US, even though the S&P, Dow Jones, and the Nasdaq all fell slightly on Friday, futures tracking these indices are currently in the red again, pointing to a lower open today.

COMMODITIES: Oil prices surged in the early European session, taking advantage of the weaker greenback amid worries over stronger demand prospects in some of the world’s biggest economies. On Saturday, the Iranian Supreme leader Ayatollah Ali Khamenei echoed President’s Hassan Rouhanis suggestion to block Gulf oil exports if Iran’s exports were restricted, while he characterized talks with the US an “obvious mistake”. WTI and Brent crude were rising, trading not far below $69 and $74 a barrel and adding 1.17% and 1.68% respectively. Gold was down, though not by much (-0.08%), trading around $1230.4 per ounce.

Day ahead: Eurozone flash Consumer Confidence Index in the spotlight; trade developments eyed

On Monday, July’s flash figures on consumer confidence due at 1400 GMT will attract the most attention in the Eurozone as investors are eagerly looking for signs showing that the bloc’s economic slowdown in the first quarter was a temporary blip. The European Commission, however, is expected to say that the measure remained in negative territory for the second month running, with analysts predicting the index to deteriorate to -0.7 from -0.5 in June, a bearish growth evidence that could keep growth prospects for the second quarter pessimistic ahead of the preliminary PMI readings on Tuesday and the ECB monetary policy meeting on Thursday. While the central bank has already announced its decision to terminate its asset purchasing program at the end of this year, a miss in data this week could turn policymakers cautious on future rate hikes as the central bank is planning to shift focus back to rate adjustments after ending its QE program, with markets projecting the first rate rise to come not until the end of 2019. Should today’s data indicate that consumers have lower-than-expected prospects on their future spending, euro/dollar could start erasing Friday’s gains. On the other hand, a surprising improvement in the numbers could help the pair to continue its recovery.

At the same time (1400 GMT) in the US, the calendar is scheduled to deliver stats on existing home sales for the month of June. After contracting by 0.4% month-on-month (m/m) in May and plunging by 2.7% in April, forecasts are now for a growth of 0.5%. The number of existing residential buildings sold in the previous month is anticipated to inch up from 5.43 million to 5.44mn. Still, new potential developments on the trade front could offset any data impact today as the G20 meeting between finance ministers and central bank delegates during the weekend did little to ease tensions. Instead, the US backed its import tariffs and urged its allies to ease their barriers on US products, a few days after the US president said he was ready to impose tariffs on all goods imported from China. European finance ministers were also on the defensive, claiming that no trade deal is possible with the US unless the US removes its duties. On Wednesday, all eyes will turn to Washington, where Trump and the President of the European Commission, Jean-Claude Junker will meet to discuss on security and economic matters such as tariffs on metals and imported cars, with markets being interested to see whether Junker could achieve some progress in the countries’ relations.

Meanwhile in neighboring Canada, May’s wholesale trade figures will gather some attention at 1230 GMT.

On the monetary front, the Bank of Japan will be in the spotlight after reports stated that the central bank is holding preliminary talks regarding changes in interest rates and stock-buying that could remove a layer of stimulus. The headline pushed Japanese bond yields up to levels not seen since February and the yen to 3-week highs, persuading the BoJ to engage in a special bond-buying operation. Moreover, the news came a week before the central bank decides on interest rates, raising speculation that policymakers could signal the start of a stimulus reduction phase. Still, investors worry that a subdued inflation could refrain policymakers from announcing any policy adjustments. Early during the Asian session at 0030 GMT, traders will see the release of Japanese preliminary manufacturing PMIs for the month of July, though the impact on the yen could be minimal as the safe-haven currency tends to react little on data.

US relations with Iran would be also in focus after the Iranian and the US presidents unleashed war of words yesterday with the former warning that “peace with Iran is the mother of all peace, and war with Iran is the mother of all wars” while the latter responded with harsh tone, advising Iran to “never threaten the US”. Recall that Trump recently withdrew the US from the 2015 Iranian nuclear deal, while the US government is set to reimpose sanctions on Tehran.

As for today’s, public appearances, Bank of England’s Deputy Governor Ben Broadbent will give a speech to the Society of Professional Economists in London at 1700 GMT.

In stock markets, earnings releases continue, with Google’s parent Alphabet being among companies to report quarterly reports after the market close. The company is expected to report higher earnings per share year-on-year.

{kind=link}