Here are the latest developments in global markets:

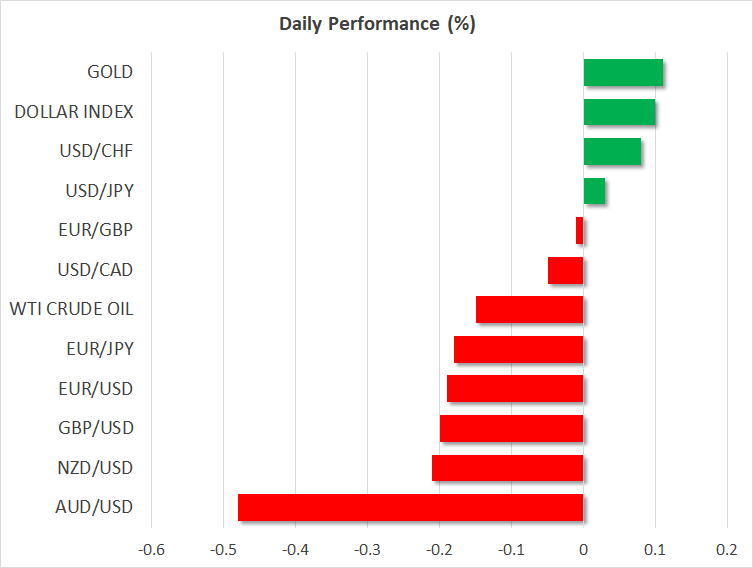

FOREX: The dollar is higher by 0.10% against a basket of six major currencies on Wednesday. Although the currency was on the back foot for most of the trading session on Tuesday, it managed to recover most of its losses following the release of upbeat US consumer confidence data. Elsewhere, the loonie continued to advance amid optimism that a resolution to the NAFTA renegotiations may be inching closer.

STOCKS: Wall Street closed higher yet again on Tuesday, albeit only fractionally so. The S&P 500 and Nasdaq Composite inched up by 0.03% and 0.15% respectively, which was still enough for both of these indices to close at new record highs for a third consecutive session. The Dow Jones, meanwhile, gained 0.06%. Futures tracking the Dow, S&P, and Nasdaq 100 are all pointing to a higher open today as well, though much will likely depend on how the US-Canada trade talks in Washington progress. Turning to Asia, it was a mixed session on Wednesday, with Japan’s Nikkei 225 (+0.15%) and the Topix (+0.46%) advancing, but the Hang Seng in Hong Kong staying marginally in the red (-0.02%). In Europe, all benchmarks except for the French CAC 40 were set to open lower today, according to futures.

COMMODITIES: Oil prices were slightly lower on Wednesday, with WTI and Brent edging down by 0.16% and 0.22% respectively, both extending the losses recorded in the previous session. The losses appear to be owed mostly to an announcement by Venezuela’s state-run oil firm that it has signed a major investment agreement valued at $430 million to increase production by 640,000 barrels per day. That said, given the country’s economic troubles, investors may have taken the news with a grain of salt, as it remains doubtful whether that will actually materialize. In precious metals, dollar-denominated gold is up by a little over 0.1% today at $1,204 an ounce, attempting to recoup some of the losses it posted yesterday as the US dollar rebounded.

Major movers: Dollar pares losses after upbeat data; loonie advances on trade hopes

The greenback was on the retreat during the European session on Tuesday, touching a one-month low against the euro as market participants continued to scale back their safe-haven bets on the dollar, amid optimism that trade tensions may subside soon. That said, the world’s reserve currency staged a comeback during the US trading session, recouping almost all its losses to close the day nearly unchanged, after the US Conference Board consumer confidence index for August was released. The figure surprisingly skyrocketed to reach a near two-decade high, generating hopes that the consumer will likely remain the driving force behind strong US economic growth.

Meanwhile, the loonie continued to advance, touching a fresh three-month high against the dollar as speculation that a NAFTA deal could be hashed out soon remained front and center. Canada’s foreign minister met with the US trade representative yesterday, and said afterwards that Mexico’s concessions to the US have “paved the way for what Canada believes will be a good week”. Separately, Canadian press reported that Ottawa is prepared to make concessions on dairy issues with the US, amplifying hopes that an accord may be inching closer. Overall, there appears to be positive momentum in these talks, and should that be confirmed further by the relevant officials in the coming days, then the loonie could remain under buying interest as the NAFTA risk premium on the currency slowly fades.

In Europe, the single currency continued its advance yesterday, with euro/sterling coming 1 pip short of touching the 0.9100 handle. Sterling continues to be clouded by political risks, with the latest media reports suggesting that the EU and UK will push back the timing of when they expect to finalize their divorce terms to mid-November, amid continued lack of progress in the talks.

Day ahead: Updated GDP estimates due out of the US; trade still in focus

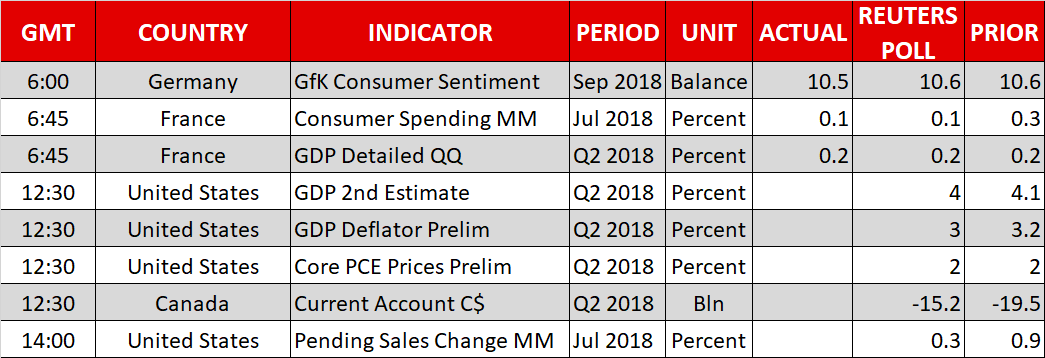

Thursday’s releases include updated growth estimates for the second quarter of the year out of the US. Meanwhile, market participants’ attention remains on trade issues.

Out of the US, the second estimate of GDP for Q2 due out at 1230 GMT is anticipated to revise growth slightly lower to 4.0% on an annualized basis, from the 4.1% in the preliminary reading. If the number comes in as expected, it would still constitute a robust figure, matching the highest pace of growth since Q2 2014. Barring a significant deviation from expectations, the dollar is not likely to react much to the release. The prints for Q2’s GDP deflator and core PCE prices will also be released at the same time, while pending home sales for July out of the world’s largest economy will be made public at 1400 GMT.

Canadian current account data for Q2 are due at 1230 GMT and are projected to show the relevant deficit narrowing to C$15.20 billion from Q1’s C$19.50bn. However, the attention in Canada remains on whether the nation will move towards the direction of entering a North American trade deal with the US and Mexico. The local dollar advanced on a report the country was ready to make concessions to enter such a deal, with dollar/loonie last trading not far above Tuesday’s near two-month low of 1.2883.

Despite the parties making up the NAFTA deal either agreeing or appearing to come closer to a deal, hopes for a breakthrough in Sino-US relationships remain under question.

Elsewhere, Brexit headlines and commentary are likely to move sterling – yesterday PM May said that a no-deal Brexit “is not the end of the world” –, while Italian budget angst may weigh on the euro.

In energy markets, EIA data on US crude stocks for the week ending August 24 are due at 1430 GMT. A drawdown by around 0.7 million barrels is expected after the previously tracked week’s larger-than-anticipated drop of roughly 5.8m barrels that led to an oil price surge.

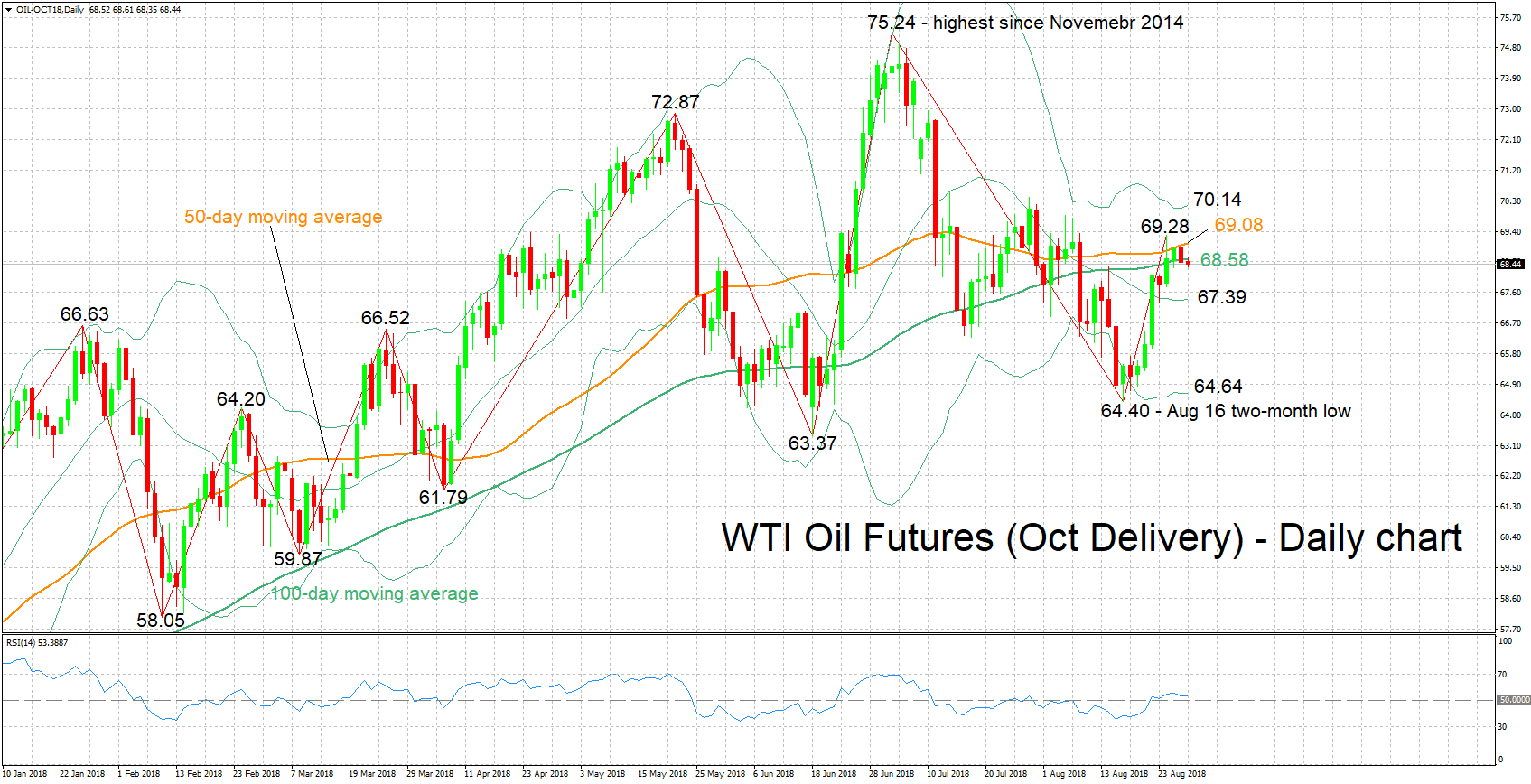

Technical Analysis: WTI oil futures looking mostly neutral in the short-term

WTI oil futures (October delivery) have largely moved sideways after touching a three-week high of 69.28 on Friday. The RSI is also moving sideways, in support of a neutral picture in the short-term.

A larger-than-expected drawdown in crude stocks out of today’s EIA report may boost prices. Immediate resistance to advances may be taking place around the current level of the 100-day moving average at 68.58; the 50-day MA and Friday’s high lie not far above at 69.08 and 69.28 correspondingly. Further above, the attention would turn to the area around the upper Bollinger band at 70.14 that also encapsulates the 70 round figure.

Conversely, a smaller-than-projected drop in crude inventories (or a build) is likely to act as a drag on prices. Support to declines may take place around the middle Bollinger line at 67.39, and further below around the lower Bollinger band at 64.64 – the region around the latter also includes the two-month low of 64.40 recorded on August 16.