Here are the latest developments in global markets:

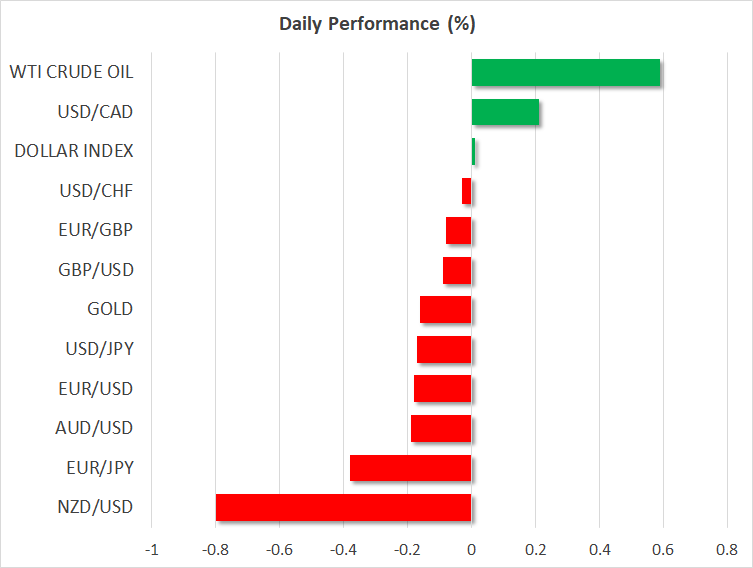

FOREX: Pound/dollar stalled yesterday’s rally, trading at 1.3016 (-0.08%) as the EU’s Brexit negotiator Michel Barnier talked down expectations of a Brexit deal today, saying that the bloc must be prepared for a “disorderly” exit. His comments came a day after he said that the UK could be offered a special partnership “such that has never been with any other country”. Euro/dollar was struggling to overcome the 1.1700 level, last seen at 1.1694 (-0.09%) despite a report by Politico stating that the EU is willing to remove tariffs on US industrial products, including cars, a move that could bring the sides close to a trade deal. In data, the Eurozone Economic Sentiment appeared unexpectedly weaker at 111.6 in August compared to a forecast of 111.9, at the lowest level reached since July 2017. That was the fourth straight month of declining sentiment. Euro/pound slipped to 0.8982 (-0.06%), while euro/yen fell to 130.27 (-0.35%). Dollar/yen fell below 1-month highs reached yesterday to touch 111.48 (-16%) ahead of the release of the core PCE inflation index later today. The dollar index was flat at 94.60. In the antipodean space, aussie/dollar and kiwi/dollar were underperforming, changing hands at 0.7296 (-0.15%) and 0.6661 (-0.80) respectively. Dollar/loonie was the best performer, rising to 1.2923 (+0.21%) a few hours before the Canadian Q2 GDP growth figures come into light.

STOCKS: European stocks followed Asian equities lower on Friday. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were down by 0.50% at 1000 GMT, with all sectors being in the red. The German DAX 30 declined by 0.95%, the French CAC 40 fell by 0.43%, while the Italian FTSE MIB retreated by 0.52%. The UK’s FTSE 100 was also trading in negative territory, losing 0.64%. Futures tracking the S&P 500, Dow Jones and the Nasdaq 100 were pointing to a marginally lower open later today.

COMMODITIES: WTI crude climbed to a 3-week high of $69.92/barrel (+0.60%) and London-based Brent surged to a 1 ½ -month high of $77.60 (+0.60%) on concerns that global supply could fall on the back of US renewed sanctions against Iran and disruptions in oil operations in Venezuela. On Wednesday, the EIA weekly report enhanced these worries, showing a larger decline in US crude inventories than analysts forecasted, while estimations that Iranian crude oil and condensate exports could fall to the lowest since April 2017 added further evidence that global supply is tightening. In precious metals, gold pulled back to $1,204.73/ounce (-0.13%).

Day ahead: US core PCE index & German CPI figures in focus; Canadian Q2 GDP growth under the spotlight too

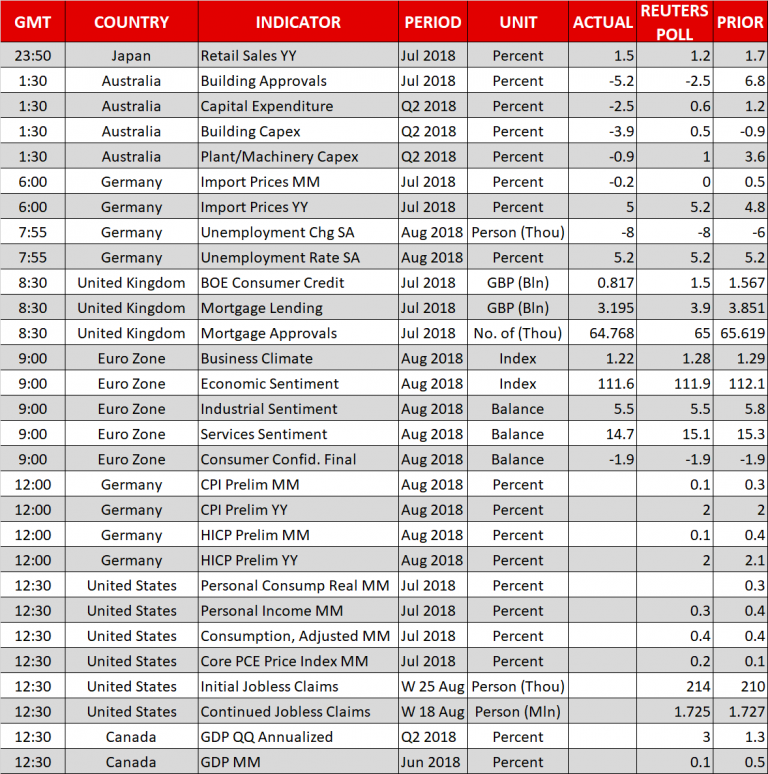

Germany, the biggest economy in the Eurozone, will deliver preliminary inflation figures for the month of August at 1200 GMT and traders may perceive the numbers as a precursor to Eurozone inflation data due on Friday. According to analysts, month-on-month (m/m) German consumer prices grew at a slower pace of 0.1% after rising by 0.3% in July, while in yearly terms the gauge stood flat at 2.0%. The Harmonized Consumer Price Index (HICP) which uses a common methodology across EU countries is expected to show that inflation in Germany softened to 0.1% m/m compared to 0.4% seen previously, while the yearly gauge also eased, edging down by 0.1 points to 2.0%. Should the data miss expectations, the euro could move south in speculation that tomorrow’s inflation data out of the Eurozone could also show some weakness, reducing pressure on ECB policymakers to raise interest rates sooner in time. Note, that German import prices, another proxy for the inflation trend, came in lower than forecasts.

Meanwhile in the US, inflation will also make the headlines as the Bureau of Economic Analysis is scheduled to release the Fed’s preferred inflation gauge, the core Personal Expenditure Index at 1230 GMT. Any upside surprise in the data could stoke market expectations for two more rate hikes by the Fed in 2018 and hence drive the dollar higher. The core PCE index is projected to gain 0.1 percentage points both in monthly and yearly terms in July, inching up to 0.2% m/m and 2.0% y/y. Stats on personal income and consumption accompanying the inflation report will also be of importance as any unexpected improvement on this front may prove that the US economy could afford further rate increases. Forecasts for personal income expect it to slip from 0.4% m/m to 0.3% in July, while consumption growth is said to remain flat at 0.4% m/m.

Initial jobless claims out of the US will come into light at 1230 GMT as well.

In Canada, the focus will shift to GDP growth data for the second quarter due at 1230 GMT. In the three months to June, the Canadian economy is expected to have picked up steam on a yearly basis, with economic activity picking up from 1.3% y/y to 3.0%. However, in monthly terms, GDP growth is estimated to drop from 0.5% to 0.1%. The loonie which has been gaining ground on hopes that a new NAFTA deal could be formed before Friday’s deadline could see a downside if GDP figures disappoint. Still, any positive trade news could provide some support to the currency, limiting the negative impact from the data.

Elsewhere, Japan will see the release of employment figures at 2330 GMT, with the jobs/applications ratio and the unemployment rate projected to remain steady at 1.62 and 2.4% respectively in July. A few minutes later at 2350 GMT, July’s flash reading on industrial production for July will gather interest as well, as analysts believe that after contracting for two months, Japanese industrial output has entered into positive territory again, reaching an expansion of 0.2% m/m. In June, production declined by 1.8%. Tokyo’s core CPI will come under the spotlight at 2330 GMT.

Staying in Asia, early on Friday at 0200 GMT, Chinese manufacturing and non-manufacturing PMIs published by the National Bureau of Statistics will hit the markets, probably bringing some volatility to the Chinese yuan as well as to other currencies depending on the Chinese economy such as the Australian dollar. The Bureau is expected to report that manufacturing activity in China was slightly lower in August, with the index sliding by 0.2 points to 51.

Brexit developments during the day would be closely monitored.

{kind=link}