Here are the latest developments in global markets:

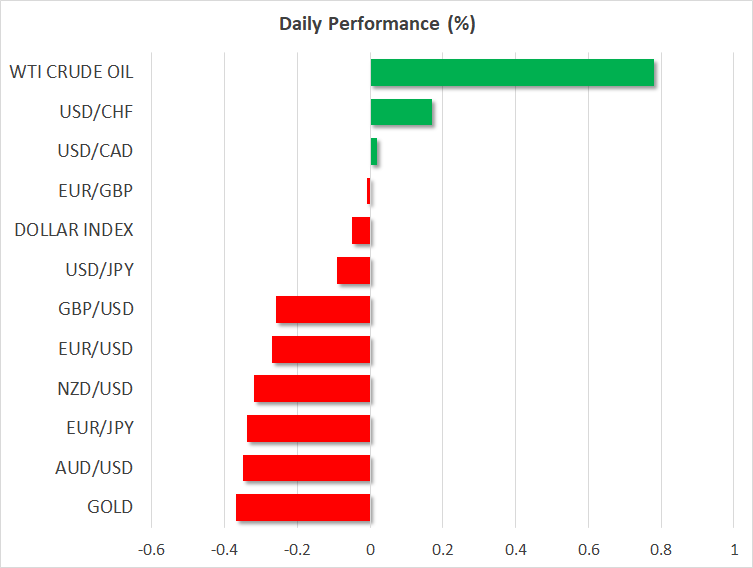

FOREX: The US dollar was nearly flat against a basket of six major currencies on Wednesday (-0.03%), after posting some modest losses in the previous session. Meanwhile, the yen retreated notably on Tuesday, as risk appetite remained firm and investors rotated out of safer assets. In Canada, the loonie staged a significant comeback amid encouraging NAFTA signals from the US President and a surge in oil prices.

STOCKS: US markets closed in the green on Tuesday, buoyed by a recovery in the tech sector. The tech-heavy Nasdaq Composite outperformed (+0.61%), propelled higher by gains in giants like Apple (+2.53%), Microsoft (+1.70%), and Google-parent Alphabet (+1.27%). Meanwhile, the S&P 500 (+0.37%) and the Dow Jones (+0.44%) edged higher as well, drawing some strength from gains in energy stocks amid a surge in oil prices. Futures tracking the S&P, Dow, and Nasdaq 100 are pointing to a more or less flat open today. Asia was a different story though, with nearly every major index being in the red on Wednesday. In Japan, the Nikkei 225 (-0.27%) and the Topix (-0.45%) dropped despite a weaker yen, while in Hong Kong, the Hang Seng was down by 0.58%. In Europe, all the major benchmarks besides the Italian FTSE MIB and Spanish IBEX 35 were set to open higher today, futures suggest.

COMMODITIES: Oil prices were higher on Wednesday, extending the significant gains recorded in the previous session. WTI was up by nearly 0.80% at $69.79 per barrel, while Brent gained a modest 0.27% to trade at $79.24 a barrel. The gains came on the back of a larger-than-expected drawdown in the private API inventory data released overnight, though it should be noted that oil prices were also boosted as Hurricane Florence was threatening to cause disruptions in US east coast gasoline markets. In precious metals, gold prices were down by 0.38%, at $1,193 per ounce on Wednesday. The dollar-denominated yellow metal remains in a narrow range between $1,214 and $1,189, showing limited response to anything besides movements in the greenback.

Major movers: Yen extends losses as risk appetite recovers; loonie rebounds

Risk sentiment remained supported on Tuesday, with funds being rotated out of safe-haven assets such as the Japanese yen and US Treasuries, and into riskier ones like US stocks. The yen retreated across the board, while yields on 2-year US Treasuries reached a fresh 10-year high, indicating a notable selloff in US bonds. At the same time, major US stock indices like the S&P 500 and the Nasdaq advanced for a second session in a row, and oil prices also headed sharply higher alongside energy stocks.

In terms of fundamental catalysts, there were multiple. For starters, reports suggest that Commerzbank and Deutsche Bank – two of Germany’s biggest and most troubled lenders – are considering a merger, alleviating some worries around the health of Europe’s financial sector. Then, US data painted a brighter picture for the nation’s booming economy, with JOLTS job openings reaching a fresh all-time high, and small business optimism as gauged by the NFIB survey also rising to the highest on record. Finally, there was no material escalation in trade frictions. Yes, China did announce it will seek WTO sanctions on the US, but that is a negligible development overall. More importantly, the US hasn’t imposed new tariffs yet – something that investors have been on edge about. The adage “no news is good news” describes this situation perfectly.

Elsewhere, positive NAFTA headlines helped the Canadian currency stage a remarkable recovery, with rising oil prices also aiding the move. The US President said that trade talks were “going well”, and that Canada wants to make a deal. The remarks came as Canada’s foreign minister Freeland returned to Washington to restart trade talks. With no major Canadian data releases on the agenda until late next week, NAFTA headlines are likely to remain the dominant force for the loonie. Any remarks suggesting further progress – particularly from US trade representative Lighthizer or Freeland – could spell more good news for the currency as the NAFTA risk premium is phased out.

In Brexit-land, the pound failed to capitalize on stronger-than-expected UK wage growth data, held back by media reports suggesting that UK officials are “misreading” upbeat statements from Brussels, and that the EU will not change its “red lines”. Sterling traded in a very volatile manner to end the day nearly flat against the dollar and euro.

Day ahead: Eurozone industrial production and US PPI due; trade, Brexit and EM closely watched

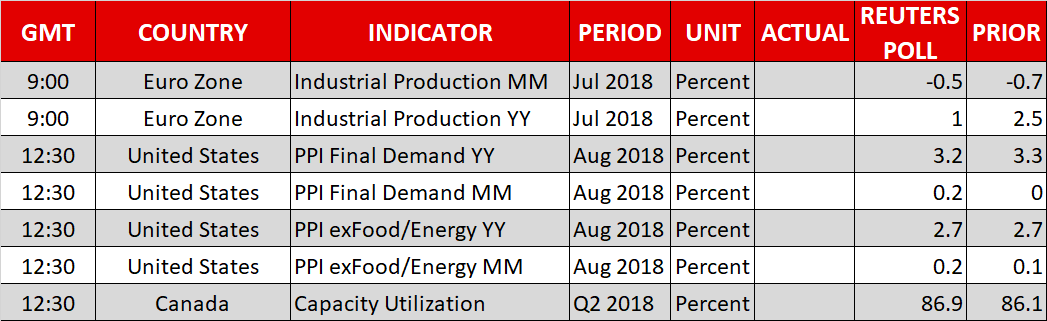

Wednesday’s calendar features eurozone industrial production figures and US producer price data. Beyond these, Brexit updates, EM angst and perhaps more importantly trade developments will be closely watched.

On the trade front, the US appears to be raising its tariff stakes. In the meantime, China will ask the WTO next week for permission to proceed with sanctions on the US for the country’s non-compliance with a ruling in a dispute over dumping duties. In terms of Canada-US talks aiming to forge a new North American trade deal, sources suggest Canada is ready to make a concession by offering the US limited access to the Canadian dairy market; such a move would bring the parties closer to a deal.

On Brexit, a special summit between the UK and the EU taking place in November could be announced soon.

Meanwhile, anxiety over EM markets remains in the background. Argentina’s central bank held rates at the record high of 60%, with the central bank of Turkey deciding on interest rates tomorrow.

In terms of data, July’s industrial production out of the eurozone will be hitting the markets at 0900 GMT. Monthly figures are forecast to reflect a contraction for the second straight month, with the annual rate of growth in industrial output expected to stand at 1.0%, down from June’s 2.5%. It is of note that German data on industrial output released last week unexpectedly showed a large fall in July.

US producer price data for August are due at 1230 GMT. The relevant index (PPI) is predicted to slightly ease in yearly terms, but grow by 0.2% m/m after exhibiting zero growth in July. The core measure of PPI that excludes volatile food and energy items is expected to expand by 2.7% y/y, the same as in July. The readings come one day ahead of prints on consumer prices out of the world’s largest economy and may be seen as giving an indication on tomorrow’s releases. Also out of the US, the Fed’s Beige Book touching on current economic conditions in each of the 12 Federal districts is due at 1800 GMT.

Capacity utilization figures for Q2 will be released out of Canada at 1230 GMT.

The UK’s Treasury Select Committee will be holding pre-appointment hearings for external members of the Prudential Regulation Committee at the Bank of England at 1315 GMT. Additionally, FOMC policymakers Bullard (non-voting FOMC member in 2018) and Brainard (permanent voter) will be talking on the US economy and monetary policy at 1340 GMT 1445 GMT respectively. Also of interest may be European Commission President Jean-Claude Juncker’s annual State of the Union speech.

In energy markets, EIA data on US crude stocks are due at 1430 GMT. A drawdown by roughly 0.81 million barrels is projected for the week ending September 7, following a fall by around 4.3mn during the previously tracked week.

Lastly, Apple will be unveiling new products, including its latest iPhone models, later today.

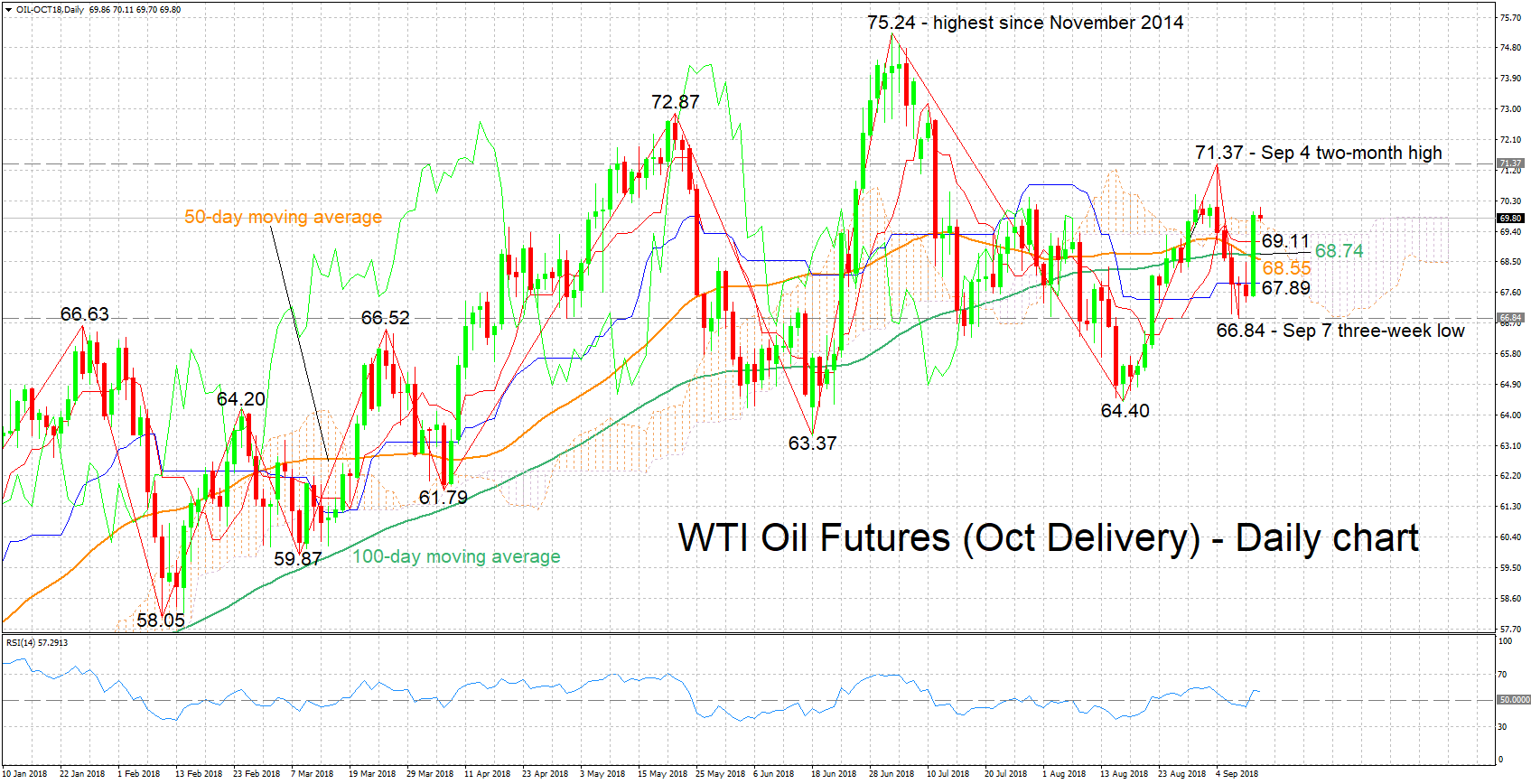

Technical Analysis: WTI oil futures positive momentum eases

WTI oil futures (October delivery) surged on Tuesday, adding 3.5%. The Tenkan- and Kijun-sen lines are positively aligned which is an indication of positive momentum in the short-term. However, the two have flatlined which suggests that the bullish bias has eased. The RSI supports this view as it has halted its advance.

A larger-than-anticipated drawdown out of today’s EIA inventory data could boost prices. Resistance to advances may take place around the two-month high of 71.37 from September 4. Further above, early July’s 75.24, the highest since late 2014, would increasingly come within scope.

Conversely, a smaller drawdown or a buildup in crude stocks may weaken prices. The area around 69.71 and 67.89 encapsulates the Ichimoku cloud top and bottom, the Tenkan- and Kijun-sen lines and the 50- and 100-day moving average lines, and may be of significance, providing support to losses. Further below, September 7’s three-week low of 66.84 would be eyed.

Supply disruptions having to do with Hurricane Florence can also affect prices.