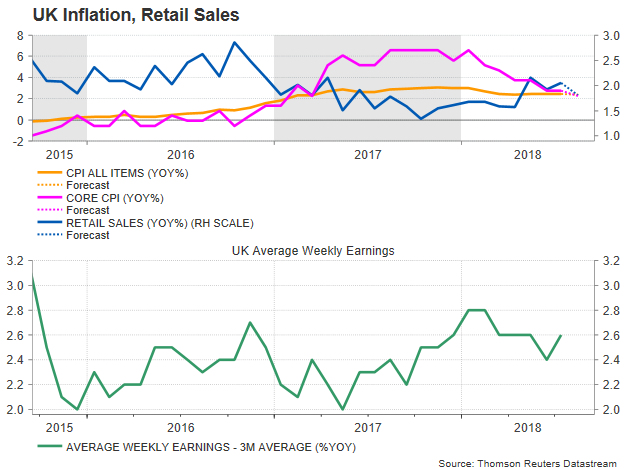

After an upbeat report on wage growth last Tuesday, consumer prices and retail sales out of the UK are the next in line to drive the British pound this week. Surprisingly, average earnings picked up speed in July, outstripping inflation for the fifth consecutive month, a sign that purchasing power could widen in the coming months. Retail sales for the month of August, however, are expected to show that household spending softened instead, even under projections that inflation in the same month has slowed down too.

On Wednesday at 0830 GMT, the Office for National Statistics in the UK is expected to report that the headline CPI rate continued to rise above the Bank of England’s price target of 2.0% in August, though compared to July’s mark of 2.5%, price growth is projected to cool to 2.4% in yearly terms. The core equivalent which excludes food and energy has also lost steam according to forecasts, inching down to 1.8%, from 1.9% in July. Producer prices accompanying the CPI release, another proxy for inflation, are expected to show a similar pattern, with the costs of goods and raw materials purchased by manufacturers easing by 0.8 percentage points to 9.1% y/y, while the costs of products sold by manufacturers is seen at 2.9%, below July’s rate of 3.1%.

On the retail sales front, forecasts are more pessimistic as analysts doubt whether the strong recovery has continued in August. In July, the heatwave in the UK and the World Cup event, fueled consumption, with retail sales surging unexpectedly by 3.5% year-on-year, faster than in June when the gauge marked a growth of 2.9%. In August, though, the weather returned to traditional temperatures and analysts believe that that the gauge declined by 0.2% month-on-month after rising by 0.7% in July, pushing the yearly measure down by 1.2 percentage points to 2.3%. Core retail sales which exclude fuel are also said to decline by 0.2% m/m, registering a slower yearly expansion of 2.5% compared to 3.7% seen before. Recall that readings from the British Retail Consortium, which are a decent gauge of the UK retail performance, identified a weaker trend in retail sales in August as well. Retail sales stats will be available on Thursday at 0830 GMT.

But even if the above data surprise to the upside, backing further monetary tightening in the future, the Bank of England appears to have no intention to elevate interest rates before Britain leaves the European Union on March 29 2019, despite signs of stronger wage and economic growth. The scenario of a no-deal Brexit became more realistic in policymakers’ minds in the past few months, with the BoE chief Mark Carney warning UK ministers behind closed doors last week about the potential negative implications under a disorderly exit from the bloc. Also, sources stated that Carney provided clues on the central bank’s strategy in case the EU and the UK fail to reach an agreement.

Still, hopes for a Brexit solution remain alive, especially after the EU Brexit negotiation, Michel Barnier stated last month that the EU is open to discuss other backstops on the Northern Ireland Border, a key issue in the Brexit talks. Optimism heightened even further this week after reports stated that Barnier is working on plans to limit physical checks at the border, a sign that a deal could be achieved ahead of November’s implicit deadline. Yet, with the UK Cabinet being divided on the Chequer withdrawal plan, the UK Prime Minister will find it hard to get the green light from Parliament even if the EU leaders compromise. Note that on Thursday, May will meet her European counterparts in Salzburg, Austria. Although this is will be an informal gathering, it could still be a stepping stone for October’s regular EU summit.

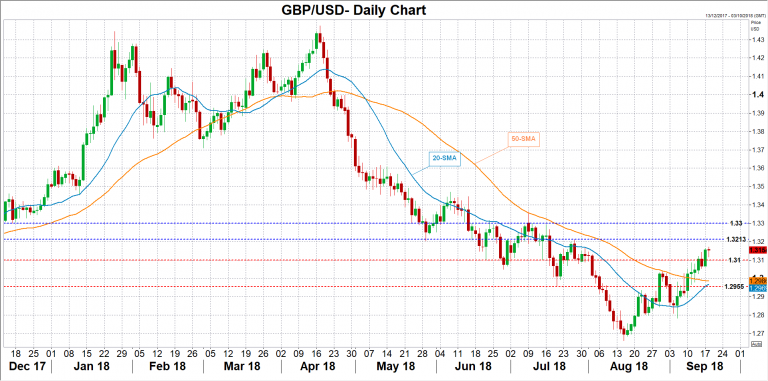

Turning to FX markets, the pound continued to lose against the US dollar in August for the fifth consecutive month, unlocking 1-year lows at 1.2660. In September, though, cable managed to rebound on the back of Brexit optimism, set to fully recover last month’s losses. While a data beat this week might not change the BoE’s “gradual and limited” rate rhetoric, it could positively affect investors outlook on the UK economy and thus push the pound even higher. In this case, traders could look for resistance around 1.3213, the peak on July 26 before eyes turn to the 1.3300 round level. A bigger challenge, however, is expected to come at July’s high of 1.3362 as any decisive close above that point would confirm the start of an uptrend.

Alternatively, if the actual numbers fell short of expectations, then immediate support could be found at 1.3100. Below that mark, bears could retest August peak of 1.3043, while steeper declines could also meet a wall around 1.2955 which acted as a support in July.

{kind=link}