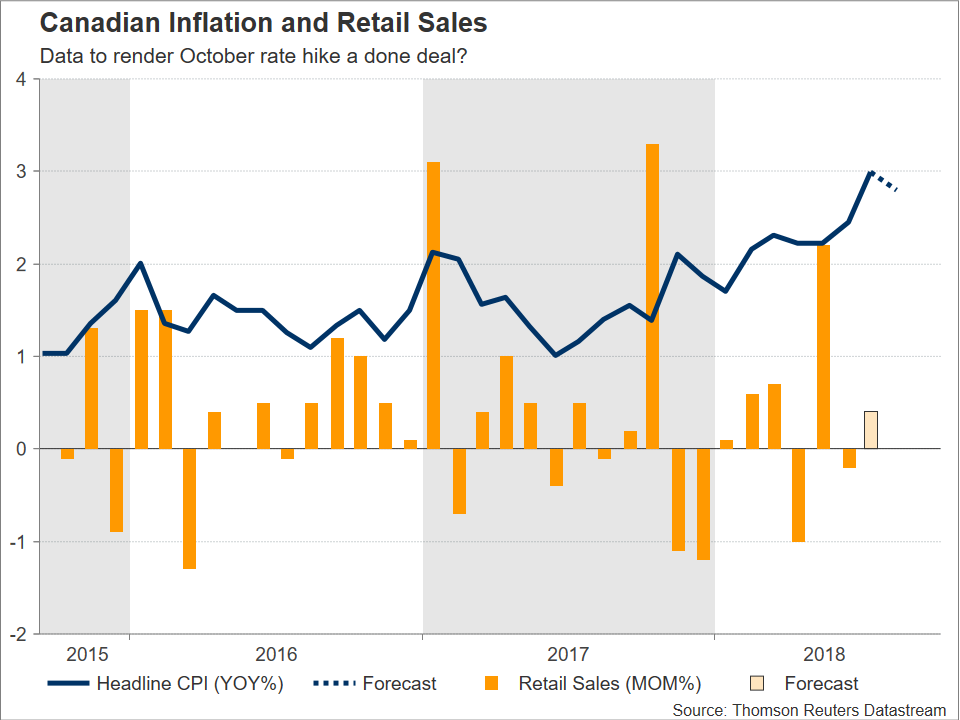

Canadian inflation and retail sales figures for August and July respectively are due on Friday at 1230 GMT. Market participants currently assign a near 80% chance for a rate hike by the nation’s central bank during its late October meeting, with a data beat having the capacity to seal the deal for such a move, consequently supporting the local dollar.

Canada’s inflation as measured by the consumer price index is anticipated to contract by 0.1% m/m in August, after rising by 0.5% in July. This would put the annual pace of growth at 2.8%, below July’s 3.0% which constituted the fastest rate of expansion since September 2011. It is notable though that energy prices contributed the most to July’s rise in inflation. Evidently, core CPI that excludes energy from its calculations grew by 1.6% y/y in July, at its highest since February 2017, but still well below headline inflation; no forecasts are available for Friday’s core inflation release. Additionally, two of the three core measures of inflation monitored by the BoC (CPI common and median) remained unchanged, while the third (CPI trimmed) ticked up to 2.1% y/y from 2.0%.

Overall, a CPI beat, is likely to be seen as more decisively putting on the table a 25bps rate increase by the Bank of Canada when it concludes its upcoming meeting on monetary policy on October 24. This would especially hold true if such an outcome stems from non-energy related price pressures, whose effects might be downplayed by the Canadian central bank; the BoC has a target band for annual inflation that ranges between 1% and 3%. For the record, Canadian overnight index swaps project a 79% probability for a rate hike in October at the moment

In terms of retail sales, those are expected to re-enter a path of positive growth after contracting by 0.2% m/m in June. Specifically, analysts’ projections put sales growth at 0.4% in July. Core retail sales that exclude automobiles, are predicted to expand by 0.6% m/m, which would again mark a rebound relative to June’s -0.1%. Despite last month’s decline in sales, data releases overall continue to suggest that the economy remains robust after clocking in an annualized rate of growth of 2.9% in Q2, this being an encouraging figure for developed country standards.

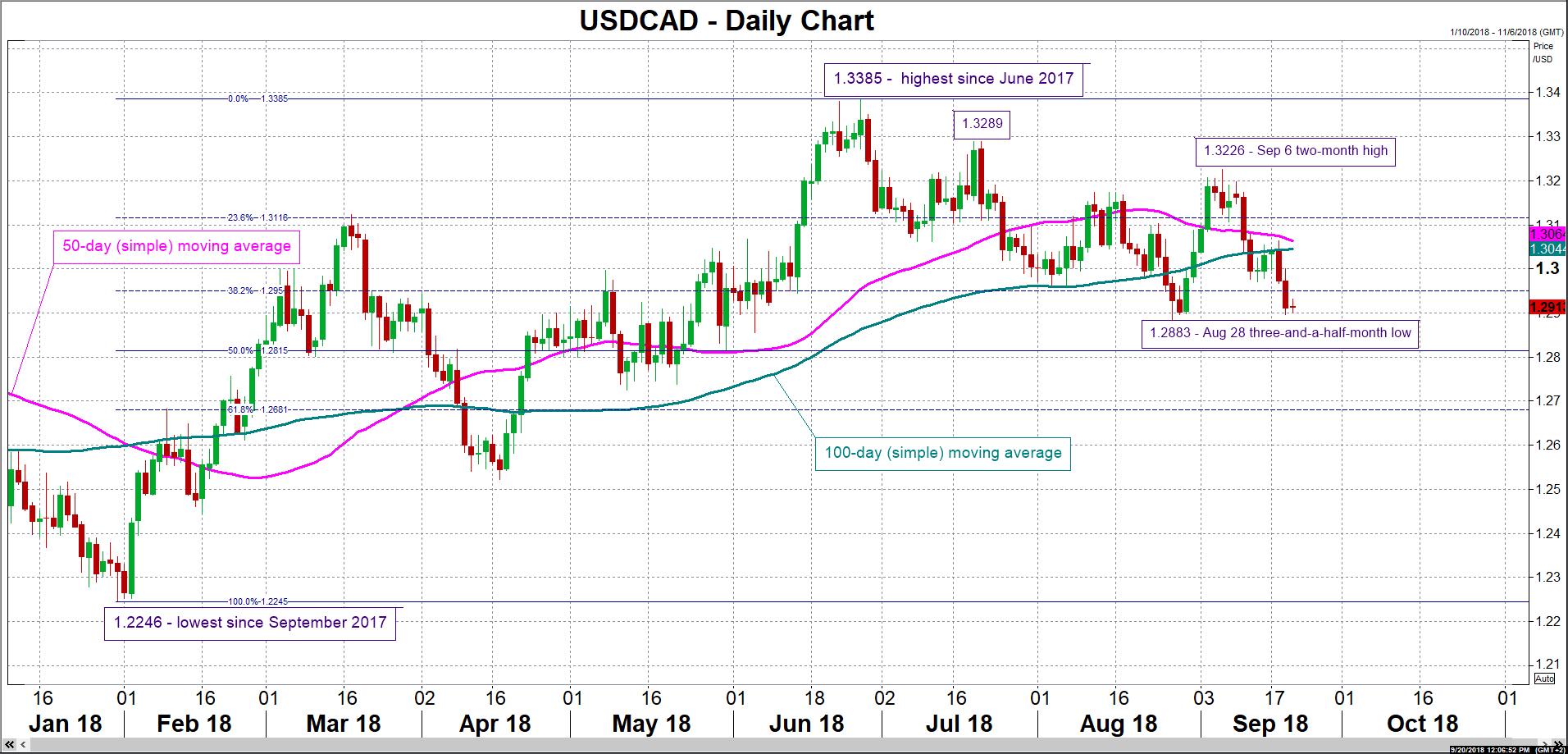

Turning to FX markets, positive Canadian data are likely to boost the loonie. Immediate support to a declining USDCAD may come around late August’s three-and-a-half-month low of 1.2883, with steeper losses eyeing the zones around the 50% and 61.8% Fibonacci retracement levels of the upleg from 1.2246 to 1.3385 at 1.2815 and 1.2681 correspondingly. On the upside and in case of disappointing numbers, resistance could occur around the 38.2% Fibonacci mark at 1.2950. Given that the region around the 1.30 round figure which was congested in previous weeks is violated to the upside as well, the current levels of the 100- and 50-day moving average lines at 1.3044 and 1.3064 respectively would come into focus. Higher still, the attention would shift to the 23.6% Fibonacci point at 1.3116. Notice that negative momentum is in place for the pair which has retreated by more than 300 pips from a two-month peak of 1.3226 hit in early September.

Of course, ongoing negotiations to strike a new North American trade agreement are also important for the direction of the loonie. The knee-jerk reaction in the event of a “deal closed” headline is likely to be a stronger loonie (conversely a “no deal” headline is most probably to be met with selling pressure on the Canadian currency). Once the dust settles though, the currency’s direction will depend on the provisions of the agreed deal. It should be kept in mind that a self-imposed deadline to arrive at an agreement by the end of the week is in place. However, such deadlines seem to be losing their significance as past ones have repeatedly been extended forward; it could be argued that they’re merely game theory type of tactics by the Trump administration to force the other party to give in to US demands. Also relating to this, a report released this week suggested that a deal is unlikely to be struck during the current week.

Lastly, Canada being a major oil exporter renders its currency sensitive to movements in oil prices. In this respect, an OPEC meeting taking place in Algeria this weekend and during which the cartel’s oil output will be discussed, looks set to determine the short-term movement of the precious liquid.

{kind=link}